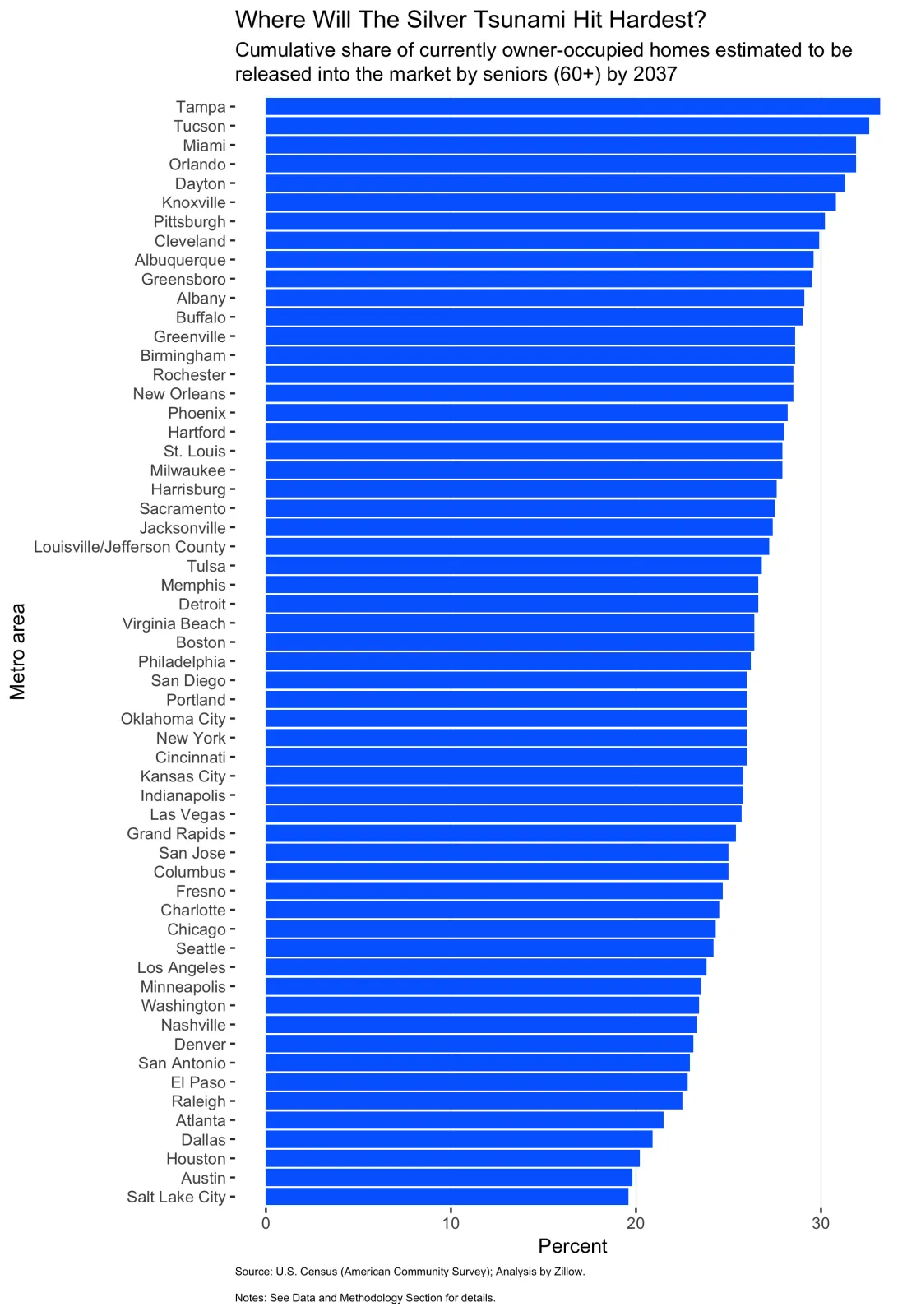

Zillow reports that over the next 20 years, more than a quarter (27.4 percent) of the nation’s currently owner-occupied homes are likely to hit the market as their current owners pass away or otherwise vacate their homes.

Places likely to be most impacted by this upcoming Silver Tsunami include both retirement hubs (Miami, Orlando, Tampa and Tucson) and regions where young residents have left (Cleveland, Dayton, Knoxville and Pittsburgh). The impact of the Silver Tsunami is also likely to vary greatly across different areas within metros.

Housing released by the Silver Tsunami will provide a substantial and sustained boost to housing supply, comparable in magnitude to the fluctuations that new home construction experienced in the 2000s boom-bust cycle.

It seems likely that, in the coming two decades, the construction industry will need to place a greater focus on updating existing properties, in addition to simply building new homes.

The massive Baby Boomer generation has already begun aging into retirement, and will begin passing away in large numbers in coming decades – releasing a flood of currently owner-occupied homes that could hit the market. That could help end the last few years’ inventory drought, as well as a more fundamental shortage of homes in certain places.

This Silver Tsunami of homes coming to market could be a good substitute for new home construction, which has been in short supply for the past decade in large part because of difficult-to-overcome challenges faced by builders.

Currently, 33.9 percent of owner-occupied U.S. homes are owned by residents aged 60 or older, and 55.2 percent by residents aged 50 or older. As these households age and begin vacating housing, that could represent upwards of 20 million homes hitting the market through the mid-2030s.

But while virtually all areas will feel the effects to some degree, this wave won’t hit all at once and won’t strike all markets equally. Certain markets will be more impacted than others, as will certain kinds of areas within a given market.

The median sales price in the Charleston market for November 2023 was $399,408, down just 0.15% from November 2022. The average days on market for November 2023 was 38 with approximately 2.32 months of inventory.

Hewing Farms is a new mungo homes community located in Summerville, SC. adjacent to the master-planned community of Carnes Crossroads right off of Hwy 17-A and only 3 miles from I-26.

The neighborhood offers a variety of community amenities including a cabana, pool, playground, walking trails, oyster shed and putting green.

The homes in Hewing Farms are designed with modern features, spacious layouts. There are two distinct Floorplan collections that contain one and two-story, hardi-plank homes that range from 1,700 to more than 4,330 square feet. Many floorplans feature the primary bedroom on the first floor, and include a designated home office or bonus room.

The community is conveniently located near shopping, dining, and entertainment options and the Hewing Farms schools are; Cane Bay Elementary, Cane Bay Middle, Cane Bay High School, Carolyn Lewis School

Always verify school attendance zones as they can change without notice.

Mortgage rates dropped significantly in the last few weeks.

The 30-year, fixed mortgage rate averaged 7.29% for the week ending Nov. 22, according to Freddie Mac‘s Primary Mortgage Market Survey. That’s down significantly from last week’s 7.44% and up from 6.58% the same week a year ago.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s average 30-year fixed rate on conventional loans at 7.283% on Wednesday.

Mortgage applications rose to their highest level in six weeks after the 30-year fixed mortgage rate fell last week.

Mortgage rates for the 30-year fixed loan averaged 7.44%, falling 6 basis points in one week, according to Freddie Mac‘s Primary Mortgage Market Survey.

On a seasonally adjusted basis, purchase applications rose by nearly 4% over the week, with increases in both conventional and government purchase loan demand.

The average loan size on a purchase application was $403,600, the lowest since January 2023. Joel Kan, MBA’s vice president and deputy chief economist, said this corroborates with other sources of home-sales data pointing to a rising share of first-time homebuyers entering the market.

Meanwhile, refinance applications rose slightly by 1.6% last week but remained subdued. The adjustable-rate mortgage (ARM) share of activity fell to 8.3% of total applications, down from 8.8% the previous week.

The share of Federal Housing Administration (FHA) loan activity increased to 14.8% of all applications, down from 14.4% the week prior. The share of Department of Veterans Affairs(VA) loan activity was 11.3%, up from 11.2% over the previous week, while the share of U.S. Department of Agriculture (USDA) loan activity fell to 0.4% from 0.5% week over week.

The deserted movie theater located at 2055 Eagle Landing Blvd., within walking distance of Northwoods Mall, in North Charleston is now the future site of the city’s next public affordable housing neighborhood.

The North Charleston Housing Authority recently purchased the 6.5-acre site for $3.85 million. The sale closed in late October.

Jeremy Erling, the housing agency’s executive director, said the group is currently searching for a developer to build “much needed” affordable housing units on the site. Preliminary studies suggested 130 units, but the end count could be higher or lower.

The authority has been on the hunt for a large property since last summer. After a few offers fell through, Erling said that the former theater site was an ideal fit.

The site has been vacant since 2006, when the discount North Charleston Cinema 10 closed. At one time a hotel was planned to be built but it never materialized.

Tax credit: These are dollar-for-dollar reductions on your tax bill. When you claim a tax credit, the amount you owe goes down the exact same dollar amount.

Tax incentive: These encourage taxpayers to do something, like install efficient appliances, in exchange for a tax reduction.

Tax refund: You’re probably familiar with this one already. You’ll get a refund if you pay more in taxes — say, through your paycheck withholdings — than you actually owe.

Tax rebate: These are retroactive tax decreases. Unlike refunds, they can come at any time of year. Rebates are often offered to stimulate the economy, because people tend to spend them immediately.

Tax break: A general term referring to various tax benefits. These could be credits, deductions, exemptions and others.

Tax benefit: Similar to a tax break, these lower your tax liability.

Home improvement tax deduction: Qualifying improvements to your home that qualify for tax deductions.

Most home improvements, like putting on a new roof or performing routine maintenance, don’t qualify for any immediate tax breaks. However, some (known as capital improvements) may raise the value of your home. In that case, you may see a benefit when you sell.

For immediate benefits, check out these incentives that will reduce your 2023 taxes:

Energy efficiency tax credits

Reducing energy consumption saves money and natural resources. The IRA includes multiple clean energy tax credits to help you do both.

Heat pumps: Your air conditioning and furnace are two of the biggest energy users in your home. Switching to an energy efficient heat pump can net you a 30% credit, up to $2,000.

Windows and doors: Replacing leaky doors and windows brings a 30% credit on the cost, up from 10% last year. Credits are capped at $600 for windows and $500 for two doors.

Electrical upgrades: If you need to update your electrical panel to handle new appliances, the government will pay 30%, up to $600.

Home energy audit: To get the most out of these tax incentives, start with a home energy audit. A credit of up to $150 offsets the cost.

Don’t stop there. “[I]incentives on items like solar, energy storage, EVs [electric vehicles] and more are incredibly generous,” says Greg Fasullo, CEO of Elevation, a residential clean technology company.

Installing solar panels gets you a 30% credit. Depending on the size of the project, Fasullo predicts you could save $6,000, based on the average rooftop solar installation cost of $20,000.

Home office tax deduction

Working from home since the pandemic? Fifty-eight percent of American workers are, too, at least part of the time.

If you use a portion of your home exclusively for business purposes, “you may be able to deduct a portion of your mortgage interest, property taxes, and other expenses related to that space,” says Seth Diener, a private wealth manager at Diener Money Management.

The Internal Revenue Service (IRS) has specific rules about what qualifies as a home office, though. If you’re doing Zoom calls from the kitchen table where you eat dinner every night, that doesn’t count. You must have a separate room or area that’s only used for your home office. If that’s you, you can calculate this deduction two ways:

Regular method: Figure out the percentage of your home you use for work. The deduction you can claim is based on this number, and whether your expenses are direct or indirect.

Simplified method: Calculate the square footage of your home office and multiply it by $5 per sq. ft., up to 300 sq. ft., with a maximum deduction of $1,500.

Medical improvements

“If you have medical upgrades that are prescribed by a doctor, such as wheelchair ramps or other accessibility features, these may be deductible as medical expenses,” says Andrew Latham, a certified financial planner and director of content at SuperMoney.com.

The IRS website offers a non-exhaustive list of qualifying capital expenses, including widening doorways, moving electrical devices, adding handrails and grading the exterior.

Note: If the medical home improvement raises the value of your home, the deduction will be based on the difference between the cost of the improvement and the increase in property value.

Rental property investments

Improvements to rental properties fall under a deduction called depreciation.

“Improvements to a rental property are usually considered deductible business expenses,” Latham says. “However, these incentives are subject to specific rules and limits, so it’s advisable to check current tax laws or consult with a tax professional.”

Federal vs. State Home Improvement Tax Incentives

What if you put in that heat pump and got back $2,000 from the federal government? Could you also claim the credit on your state return?

“Yes, in some instances, you can qualify for multiple tax breaks for the same project,” Latham says. “[I]f you install a new energy-efficient heat pump, you might be eligible for a federal tax credit, a state-level incentive, and potentially a rebate from your local utility company.”

Always check with a tax professional for advice as rules and laws change.

Home prices in the 20 biggest U.S. metros rose for the sixth month in a row, as the housing market continues to deal with a shortage of homes for sale.

The S&P CoreLogic Case-Shiller 20-city house price index rose 1% in August, as compared with the previous month.

On a year-over-year basis, home prices in the 20 major metro markets in the U.S. were up 2.2% nationally.

A broader measure of home prices, the national index, rose on a month-over-month basis in August by 0.9%, but rose 2.6% over the past year. All numbers are seasonally adjusted.

Key details: Chicago posted the strongest year-over-year home-price gains in the month of August, at 5%. It was the fourth month in a row that the city led the rankings.

New York and Detroit followed, up 4.98% and 4.8% respectively.

The West continued to lag behind the rest of the country: Home prices fell in Las Vegas and Phoenix the most.

Cities

Change from last year

Atlanta

3.4%

Boston

3.1%

Charlotte

3%

Chicago

5%

Cleveland

3.9%

Dallas

-1.7%

Denver

-0.6%

Detroit

4.8%

Las Vegas

-4.9%

Los Angeles

3.2%

Miami

3.3%

Minneapolis

1.9%

New York

5%

Phoenix

-3.9%

Portland

-1.5%

San Diego

4.1%

San Francisco

-2.5%

Seattle

-1.5%

Tampa

0%

Washington

3.4%

Composite-20

2.2%

A separate report from the Federal Housing Finance Agency also showed home prices rose in August, up 0.6% from July.

And over the last year, the FHFA index was up 5.6%.

Home prices were the strongest in the Middle Atlantic region, according to the government’s data.

Big picture: With homeowners not keen on selling their homes, the U.S. housing market will continue to face a shortage of homes for sale, and by extension, see home prices rise. Interested buyers continue to converge on limited inventory.

Until supply catches up, barring any major events, we’re not likely to see a big movement in home prices.

What S&P said: “On a year-to-date basis, the National Composite has risen 5.8%, which is well above the median full calendar year increase in more than 35 years of data,” said Craig J. Lazzara, managing director at S&P DJI.

“The year’s increase in mortgage rates has surely suppressed housing demand, but after years of very low rates, it seems to have suppressed supply even more,” he added.

“Unless higher rates or other events lead to general economic weakness, the breadth and strength of this month’s report are consistent with an optimistic view of future results,” Lazzara said.

What are they saying? “Another large gain in house prices in August suggests that the extremely limited supply of existing homes for sale continued to outweigh high mortgage rates,” Thomas Ryan, property economist at Capital Economics, wrote in a note.

“We think monthly gains in house prices will soften over the remainder of the year in response to the rise in mortgage rates to just under 8.0%. But an extreme lack of inventory in the existing homes market means we don’t anticipate any further house price falls,” he added.

Market reaction: Stocks were up in early trading on Tuesday. The yield on the 10-year Treasury note fell below 4.9%.

Nexton, the most innovative and walkable community in South Carolina, received the Grand Aurora Award in the category “Residential Housing Community of the Year – Masterplan,” at the 2023 Southeast Building Conference. The conference was held on July 21 at the Rosen Centre Hotel in Orlando, Fla.

This award is a testament to Nexton’s dedication to providing residents with environments that allow them to inspire, connect and thrive, and we are incredibly proud to be recognized,” says Cassie Cataline, marketing director at Nexton. “As a lifestyle-driven destination, we strive to blend thoughtful design, innovative technology and modern conveniences to attract numerous homebuyers, renters, businesses and visitors each year.”

Established by the Florida Home Builders Association in 1979, the Aurora Awards recognize outstanding projects from across the Southeast during the annual Southeast Building Conference Featuring 60 categories, the Aurora Awards encompass all facets of the residential, commercial and remodeling industries.

A jury of four acclaimed designers and builders met in May 2023 to select winning projects from a competition of nearly 400 entries. The Grand Award is the highest award an entry can receive in each category.

Celebrating the 10th anniversary of the community’s 2013 groundbreaking, Nexton is a lifestyle-driven destination that artfully blends the best of live, work and play by offering conveniences such as state-of-the-art schools, modern infrastructure, 20 miles of trails and 2,000 acres of green space. The community’s four residential neighborhoods include apartments, built-for-rent homes, townhomes and a variety of for-sale single-family homes that cater to first-time buyers, executives and 55+ retirees. Nexton has currently sold over 2,600 homes.

After already falling for two days, 30-year mortgage rates plummeted Thursday, shedding another two-tenths of a point. That drops the 30-year average to 7.92%, its cheapest level since September. Rates were down by double-digit basis points for almost every other loan type as well.

Since rates vary widely across lenders, it’s always smart to shop around for and compare rates regularly, no matter what type of loan you’re seeking.