New rules regarding the sale of residential real estate from the Financial Crimes Enforcement Network (FinCEN)—a bureau of the U.S. Treasury—became effective March 1, 2026.

FinCEN will require a Real Estate Report to be filed for non‑traditionally financed or‑cash transfers of residential property when the buyer is a legal entity or a trust. This is a nationwide requirement with no minimum purchase price.

A transaction is generally reportable if all three of these are true:

The property is residential real estate (1–4 family homes, condos, townhomes, co‑ops, and certain land intended for such use).

The buyer is an entity or trust (not an individual person).

The transaction is cash or non‑traditionally financed, meaning there is no traditional institutional mortgage from a lender that has federal anti‑money‑laundering requirements. This will include financing by hard money lenders and seller financing.

If all three apply, a federal report filing is required by the closing agents unless a specific allowable exemption exists.

The Real Estate Report to FinCEN contains information identifying the reporting person, details of the residential real property being transferred, information about the transferor (seller), information about the transferee entity or trust, and identities of individuals representing the transferee entity or trust in the transaction.

FinCEN states the new rule aims to curb money laundering and the use of shell companies to hide ownership of real estate. More details at FinCEN website:

Covenants, Conditions, and Restrictions (CCRs) are legal documents in real estate, common in planned communities and subdivisions. These recorded rules govern land use and development, establishing a framework for how properties within a specific area can be utilized. CCRs maintain community standards and can help preserve property value to ensure individual property use aligns with the neighborhood’s collective vision.

“Covenants” are promises by property owners to perform or refrain from specific actions, such as maintaining a home’s exterior or adhering to landscaping guidelines. “Conditions” are requirements for property ownership, often relating to improvements or obtaining approval for changes. “Restrictions” impose limitations on property use, which might include prohibitions on commercial activities or specific vehicle parking.

Common CCR’s

CCRs include rules and regulations for community standards. Architectural guidelines cover things like exterior paint colors, fencing materials, and home additions. Landscaping rules focus on lawn care, tree removal, and approved plant types. Pet restrictions might limit the number, size, or breed of animals and often include waste disposal requirements.

Parking rules may govern where vehicles can be parked, prohibit oversized vehicles or limit street parking. Limitations on property use, such as commercial businesses from operating from a residence or restricting short-term rentals could also be included in CCR’s.

Establishment and Enforcement

CCRs come into existence through a formal process, typically initiated by the developer of a planned community or subdivision. These documents are legally recorded with the county recorder’s office, making them part of the public record and binding on all current and future property owners within that community. This recording ensures that the rules “run with the land,” meaning they apply to the property itself, regardless of who owns it.

The Homeowners Association (HOA) may play a central role in enforcing CCRs once the community is established. Enforcement mechanisms vary but commonly include issuing warnings for minor infractions. For continued non-compliance, HOAs can levy fines, which may be assessed periodically until the violation is resolved. In more serious cases, an HOA might place a lien on the property for unpaid fines or assessments. Legal action, such as a lawsuit to compel compliance or recover damages, is another enforcement tool available to some HOAs.

Some governing documents may have a provision to amend the CCR’s, such as a vote of the majority of the members, but rules can vary.

Prospective buyers should review a property’s CCRs to understand their rights and obligations.

For communities without an HOA, CCRs might still be recorded, enforcement may be handled by a local municipality.

Do you need to prep your home prior to selling to help maximize your profit?

Home Enhance provides you a line of credit to get your home market-ready. From repairs and upgrades to moving and storage, Home Enhance can help unlock your home’s potential with nothing due until closing.

Unsecured (no lien) personal line of credit up to $50,000

No impact to credit score when applying

Freedom to use any contractor or home vendor

Low interest that only accrues on what is used

Nothing due until closing

Plus: Apply in 90 seconds, Access funds same day as approval, No cost if funds aren’t used, All home prep expenses in one place, Works with estates, trusts, LLC’s, POAs, Use funds beyond home improvements (moving, storage, temp housing, etc.)

What does the seller pay? $499 origination fee +8.99 – 16.99% interest only accrues on funds that are used. – Rate depends on credit.

If you are interested in this program, please contact me.

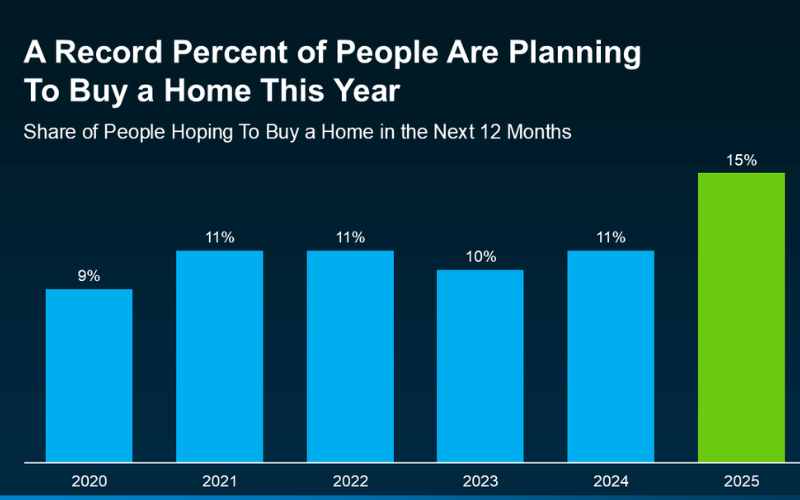

According to a recent NerdWallet survey, 15% of Americans are planning to purchase a home this year. That’s actually a record high for this survey (see graph below):

The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening but does indicate that buyers are optimistic. Whether they’re feeling more confident about moving, or saved money, or simply can’t wait any longer – this seems to be the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring.

The National Association of Realtor’s economists recently weighed in on home sales, mortgage rates, the economy and changing buyer demographics and its effect on real estate for the year ahead.

Lawrence Yun, chief economist of the National Association of REALTORS®, along with NAR’s Deputy Chief Economist, Jessica Lautz, shared data and forecasts..

Their updated estimates show that the housing market is still dramatically undersupplied, and they estimate that U.S. housing stock is 3.7 million units below what is needed.

High mortgage rates and rising home prices have put a damper on affordability and are directly related to the supply shortage. Building more houses is essential but builders are also contending with high interest rates.

There is no silver bullet to alleviating this ongoing shortage but there are options being considered such as, accessory dwelling units (ADUs), Community Land Trusts, condominium conversions, and manufactured homes. They will continue to study this topic and work to uncover potential solutions.

Yun released a rosier forecast for the housing market for 2025 and 2026, with an outlook for higher home sales and moderating mortgage rates.

Here’s an overview of NAR’s predictions on key housing indicators for the year ahead.

Home Sales to Rise

With improving job numbers and recent gains in the stock market, more Americans may be motivated to act, Yun said.

Here’s Yun’s forecast over the next two years:

2025 sales projection: Existing home sales to rise 9% year-over-year; New home sales to jump by 11%.

2026 sales projection: Existing-home sales to rise 13% year-over-year; new home sales to increase by 8%.

Mortgage Rates to Moderate

The trajectory of mortgage rates will have a major bearing on how the housing market will fare, Yun said.

Mortgage rates may moderate but buyers may not see that anytime soon, Yun said. “Mortgage rates will not decline in tandem”… “With a large budget deficit, there’s less mortgage money available…. A large budget deficit will prevent mortgage rates from going down to 4%”

Nevertheless, the “locked-in” effect of homeowners feeling stuck-in-place with low 2% or 3% mortgage rates from recent years will lessen over time, as personal milestones (births, deaths, marriages, graduations, new jobs,etc.) trigger real estate moves.

Home Prices Increases Slowly After Rapid Rises

While homeowners have enjoyed record-breaking equity gains, home buyers’ have been struggling with affordability. A typical homeowner has accumulated $147,000 in housing wealth just over the last five years, according to NAR’s research. As a result, the spread in median net worth between homeowners and renters continues to grow. It stands at $415,000 for homeowners versus $10,000 for renters, Yun said.

“The strong price increases cannot be sustainable for another five years, or America will be divided … with only a few getting to experience the tremendous housing wealth,” Yun said. “If we bring more supply to the housing market, home price increases will not be as outrageous … and will be more in line with wages.”

Yun’s forecast:

2025 median home price: $410,700; up 2% over 2024.

2026 median home price: $420,000, up 2% over 2025.

A Different Type of Buyer Emerges

The profile of home buyers are changing, Lautz said, presenting data from NAR’s newly released 2024 Profile of Home Buyers and Sellers. Here’s a few of the changes observed in the report:

More buyers are skipping the mortgage. all-cash buyers have surged to record highs, accounting for 26% of home sales over the past year. Thirty-one percent of repeat buyers paid all-cash for their next home purchase.

First-time buyers are getting older. The median age of a first-time home buyer was 38, an all-time high. Twenty-five percent of first-time buyers used a gift or loan from a relative or friend for their home purchase; 20% took money out of financial assets like stocks, 401ks or cryptocurrency to afford homeownership; and 7% used inheritance money for their purchase—a record high, Lautz noted. First-time buyers are coming up with the highest down payments in nearly 30 years—at 9%—in order to afford the higher home prices.

The allure of cities grows. The pandemic may have unleashed a trend of suburban movers, but people are now heading back to city centers—the largest uptick in a decade, Lautz said.

More buyers are pooling their money. The number of multigenerational households surged to an all-time high of 17% over the past year. “The number one reason is for cost savings,” Lautz said. “They’re combining incomes” in order to afford homeownership. They’re also buying a multigenerational home to take care of aging parents or because of young adults are moving back home, Lautz noted.

Single women buyers continue to outpace single men buyers. A drop in marriage rates has triggered more consumers to enter the housing market on their own. Single women held a 24% share of the home-purchase market over the past year. For single men, it was 11%.

The latest monthly housing report from Realtor.com® reveals that the typical listed price per square foot grew by a whopping 52.7% from May 2019 to May 2024.

The price per square foot is a crucial metric in real estate because it allows for easy comparison between different properties, regardless of their size. And while this is valuable information, it’s only one data point of many that buyers and sellers should consider.

Examining the markets with the steepest rises in price per square foot reveals substantial growth in popular metropolitan areas. Based on listing price, properties in the New York City metro area (+84.7%), Boston (+72.9%), and Nashville, TN (+68.6%), have seen the great increases in price per square foot since May 2019.

LOCAL – CHARLESTON MLS

Locally, our median price per sqft has increased about 65% from May of 2019 to May of 2024. Our median price per/sqft in May of 2019 was $150 / sqft and in May of 2024 it was $229 / sqft .

Our median sales price has increased about 67% from May of 2019 to May of 2024. Our median sales price in May of 2019 was $285,000 and in May of 2024 it was $425,000

Are you thinking about making a move? If so, now may be the perfect time to start the process. That’s because experts say the best week to list your house is just around the corner.

A recent Realtor.comstudy looked at housing market trends over the past several years (with the exception of 2020, since it was an unusual year), and found the best week to put your house on the market this year is April 14-20:

“Every year, one week stands out from the rest as that perfect stretch of time when it’s great to be a home seller. This year, the week of April 14–20 is the best time to sell—that is, if sellers want to see lots of interest in their homes, sell quickly, and pocket some extra cash, according to Realtor.com® data.”

While the spring market is a great time to sell no matter the week, this may be the peak sweet spot. And if you’ve been putting your plans on the back burner and waiting for the right time to act, this could be the nudge you need to make your move happen. As Hannah Jones, Senior Economic Research Analyst at Realtor.comexplains:

“The third week of April brings the best combination of housing market factors for sellers. The best week offers higher buyer demand, lower competition [from other sellers], and fewer price reductions than the typical week of the year.”

If you have considered selling, feel free to contact me for a no-obligation consultation.

If you’re planning to move soon, you might be wondering if there’ll be more homes to choose from, where prices and mortgage rates are headed, and how to navigate today’s market. If so, here’s what the professionals are saying about what’s in store for this season.

Odeta Kushi, Deputy Chief Economist, First American:

“. . . it seems our general expectation for the spring is that we will see a pickup in inventory. In fact, that already seems to be happening. But it won’t necessarily be enough to satiate demand.”

“Where we are right now is the best of both worlds. Price increases are slowing, which is good for buyers, and prices are still relatively high, which is good for sellers.”

“There are slightly more homes for sale than this time last year, and there is still plenty of competition for well-priced houses. Buyers should prep their credit scores and sellers should prep their properties now, attractive listings are going pending in less than a month, and time on market will shrink in the weeks ahead.”

“While mortgage rates remain elevated, home shoppers who are looking to buy this spring could find more affordable homes on the market than they saw at the same time last year. Specifically, there were 20.6% more homes available for sale ranging between $200,000 and $350,000 in February 2024 than a year ago, surpassing growth in other price ranges.”

If you’re looking to sell, this spring might be your sweet spot because there just aren’t many homes on the market. Sure, inventory is rising, but it’s nowhere near enough to meet today’s buyer demand. That’s why they’re still selling so quickly.

If you’re looking to buy, the growing number of homes for sale this spring means you’ll have more choices than this time last year. But be prepared to move quickly since there’ll be plenty of competition with other buyers.

If you need assistance buying or selling a home in the Charleston Area, feel free to contact me! I would be glad to help!

Wondering if it still makes sense to sell your house right now? Everyone’s situation is unique, but the current market could prove to be beneficial for you.

An article from Calculated Risk shows there are 15.6% more homes for sale now, nationally, compared to the same week last year. That tells us inventory has grown. But going back to 2019, the last normal year in the housing market, there are nearly 40% fewer homes available now:

How this could benefit you when you sell.

1. You Have More Options for Your Move

If you are going to move to another home, the year-over-year growth gives you more options for your home search. This means it may be a little less of a challenge to find what you’re looking for.

2. You Still Won’t Have as Much Competition When You Sell

Even though there are more homes for sale now, there still aren’t as many as there’d be in a normal year. Remember, the data from Calculated Risk shows we’re down nearly 40% compared to 2019. And that large a deficit won’t be solved overnight. As a recent article from Realtor.comexplains:

“. . . the number of homes for sale and new listing activity continues to improve compared to last year. However the inventory of homes for sale still has a long journey back to pre-pandemic levels.”

Less competition means you may find an eager buyer quickly and get your home sold for top dollar.

Bottom Line

So, If you’re a looking to make a move, NOW could prove to be a great time! You’ll have more options when buying your next home than you did last year, and there’s not a ton of competition from other sellers.

If you have considered selling, I would be happy to provide you with information and resources to help you determine if the timing is right for you to make a move.

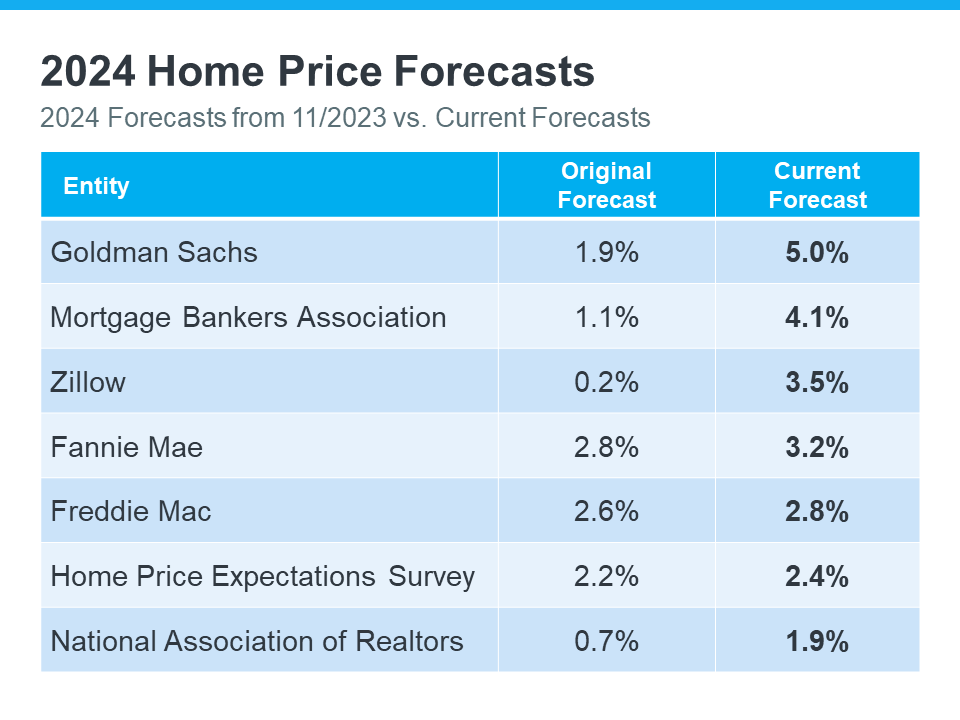

Over the past few months, experts have revised their 2024 home price forecasts based on the latest data and market signals, and they’re even more confident prices will rise, not fall.

What’s caused the change?

2024 Home Price Forecasts: Then and Now

The chart below shows what seven expert organizations think will happen to home prices in 2024. It compares their first 2024 home price forecasts (made at the end of 2023) with their newest projections:

The middle column shows that, at first, these experts thought home prices would only go up a little this year. But if you look at the column on the right, you’ll see they’ve all updated their forecasts and now think prices will go up more than they originally thought. And some of the differences are major.

There are two big factors keeping such strong upward pressure on home prices. The first is how few homes are for sale right now. According to Business Insider:

“Low home inventory is a chronic problem in the US. This has generally kept home prices up . . .”

A lack of housing inventory has been pushing prices up for a long time now – and that’s not expected to change dramatically this year. But what has changed a bit is mortgage rates.

Late last year when most housing market experts were calling for home prices to rise only a little bit in 2024, mortgage rates were up and buyer demand was more moderate.

Now that rates have come down from their peak last October, and with further declines expected over the course of the year, buyer demand has picked up. That increase in demand, along with an ongoing lack of inventory, is what’s caused the experts to feel the upward pressure on prices will be stronger than they expected a couple months ago.

A Look Forward To Get Ahead of the Next Forecast Revisions

Real estate experts regularly revise their home price forecasts as the housing market shifts. It’s a normal part of their job that ensures their projections are always up-to-date and factor in the latest changes in the housing market.

That means they’ll continue to revise their projections as the housing market changes, just as they’ve always done. How those forecasts change next is anyone’s guess but pay attention to mortgage rates.

If they trend down as the year goes on, as they’re expected to do, that could lead to more buyer demand and even higher home price forecasts.

Basically, it’s all about supply and demand. With supply still so limited, anything that causes demand to go up will likely cause prices to go up, too.

Bottom Line

At first, experts believed home prices would only go up a little this year. But now, they’ve changed their minds and are forecasting that prices will grow even more than they originally thought.

If you have considered buying or selling a home this year, I would love to help! Please feel free to contact me.

{kind=link}