Have you been thinking about selling your house? If so, here’s some good news. While the housing market isn’t as frenzied as it was during the ‘unicorn’ years when houses were selling quicker than ever, they’re still selling faster than normal.

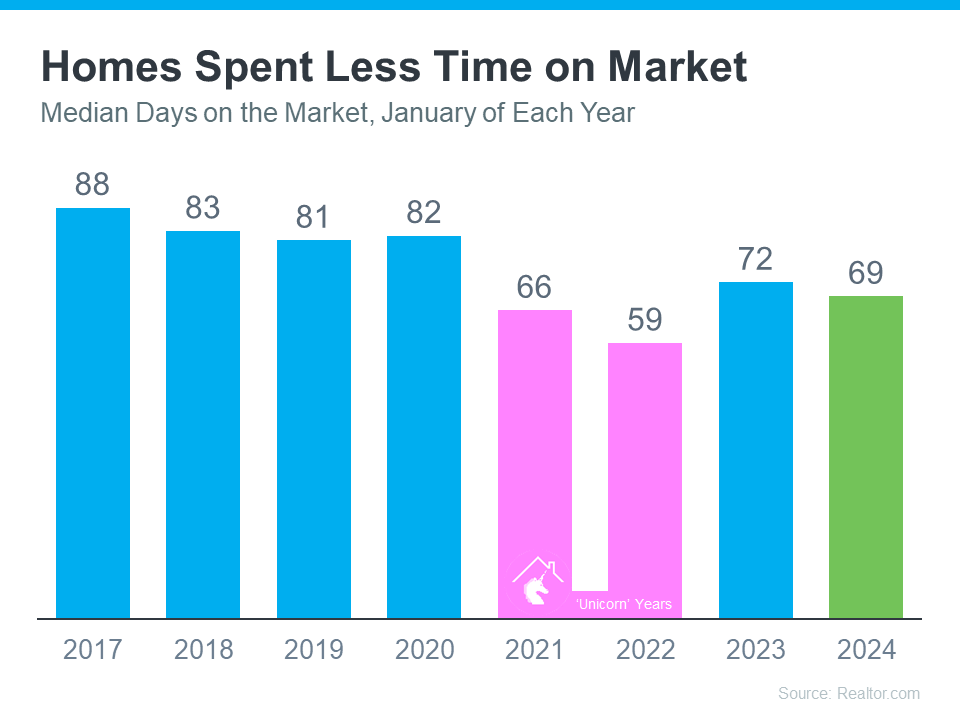

The graph below uses data from Realtor.com to tell the story of median days on the market for every January from 2017 all the way through the latest numbers available. For Realtor.com, days on the market means from the time a house is listed for sale until its closing date or the date it’s taken off the market. This metric can help give you an idea of just how quickly homes are selling compared to more normal years:

When you look at the most recent data (shown in green), it’s clear homes are selling faster than they usually would (shown in blue). In fact, the only years when houses sold even faster than they are right now were the abnormal ‘unicorn’ years (shown in pink). According to Realtor.com:

“Homes spent 69 days on the market, which is three days shorter than last year and more than two weeks shorter than before the COVID-19 pandemic.”

Locally, The Charleston MLS is currently at 27 days on Market.

What Does This Mean for You?

Homes are selling faster than the norm for this time of year – and your house may sell quickly too. That’s because more people are looking to buy now that mortgage rates have come down, but there still aren’t enough homes to go around. Mike Simonsen, Founder of Altos Research, says:

“. . . 2024 is starting stronger than last year. And demand is increasing each week.”

Bottom Line

If you’re wondering if it’s a good time to sell your home, the most recent data suggests it is. The housing market appears to be stronger than it usually is at this time of year. To get the latest updates on what’s happening in our local market, let’s connect.

According to the latest report from Zillow, reported by Globalflare, the state of South Carolina was recently ranked as the #1 state in America for selling the most homes per capita.

The Palmetto State is currently experiencing an impressive rate of 77.30 homes sold for every 100,000 residents. Over the course of the last month, a total of 4,071 houses and apartments changed hands, with an average selling price of $301,659.

Methodology: Zillow was checked to see recently sold houses and apartments over the last 30 days across America.

A capital gain is the profit made when selling an investment or asset, including real estate. The capital gains tax is the levy on that profit when an investment is sold. It is owed for the tax year during which the investment is sold.

Long-term capital gains tax is the tax levied on profits of an asset or investment that was owned for over one year. The long-term capital gains tax rate vary and depend on your income but the rates are typically lower than your ordinary income tax rate

If the investment or asset is owned for less than a year when the gain is made, then the short-term capital gains tax applies. The short-term rate is typically determined by the taxpayer’s ordinary income bracket – but can vary in some circumstances.

The Primary Residence Exclusion. IRS – Section 121

The Internal Revenue Service (IRS) allows homeowners to exclude a certain amount of gains that result from the sale of their primary home from their income. This is known as the Section 121 rule.

Single Homeowners may exclude up to $250,000 of gains on the sale of their property, and married homeowners filing jointly can exclude up to $500,000.

To be eligible for these exclusions You must have owned the home for at least two years AND have lived in the home as your primary residence for at least two years of the previous five years prior to the sale date. The two-year period does not have to be consecutive. See More Here at IRS

Investment Property Deferment- 1031 Tax Exchange in Real Estate

Section 1031 is a provision of the Internal Revenue Code (IRC) that allows a businesses or the owners of investment property to defer federal taxes on some exchanges of real estate. The provision is used by investors who are selling one property and reinvesting the proceeds in one or more other properties.

Qualifying Section 1031 exchanges are called 1031 exchanges, or like-kind exchanges.

In General, A 1031 exchange allows investors to defer taxes on the profits of sold investments. The exchange can be complex with rigid time frames for identifying the replacement property and reqiures a Qualified Intermediary (QI) to oversee and process and the funds.

Tax laws and codes are complex and can change, always consult a tax professional to review your unique situation.

Charleston Area Regional Transportation Authority’s (CARTA) plans to build a park-and-ride facility at the fairgrounds. This park-and-ride facility is a part of CARTA’s Lowcountry Rapid Transit Plan – the first-ever large-scale transportation project in the region.

CARTA Chairman Mike Seekings, says this $600 million plan is the result of over a decade of regional planning. If plans go through, the facility will take up about six acres of the 180 acres available for parking on the fairgrounds.

Mike Jernigan, a member of the Exchange Board as well as the former president of the Coastal Carolina Fair, says that their initial discussions with CARTA were about leasing an acre to an acre and a half of land for a bus stop, but he said that CARTA wanted more land to either purchase or take by eminent domain.

Seekings is surprised by this response. He says that they spoke with the leadership of the fairgrounds early in the process and have had conversations over many years about this area of land.

Officials with the Coastal Carolina Fair say that their issue is not the size of the facility, though, but the location. The park-and-ride facility would be located in lot 2A of the fairgrounds which is adjacent to Highway 78 and Gate 2 – one of the major entrances of the fairgrounds.

“We feel like supporting public transportation is a good thing. We’re not opposed to that in any way,” Jernigan says. We just feel like this location is the wrong location. That there are other options that are available adjacent to our property, or even at a different place on our property, but not to take our prime parking spot.”

EV battery component maker Redwood Materials has just broke ground on their massive new $3.5 billion plant at the new Battery Materials Campus, situated in the Camp Hall Commerce Park in northern Berkeley County. The company’s new anode recycling and battery component manufacturing facility will span over 600 acres.

The company’s $3.5 billion investment, marks the largest economic development announcement in the history of South Carolina, and is expected to create 1,500 new jobs.

Founded in 2017, Redwood Materials stands out as the world’s first company to recycle used electric vehicle batteries and other battery types. It extracts vital components from these batteries, which are currently sourced exclusively from Asia, and supplies them to car manufacturers for use in new electric vehicle batteries.

The tiny town in northwest Dorchester County might be getting some new next-door neighbors, and more, in one residential influx than it has ever seen before.

If approved by the county, a “cluster” housing development proposed by the D.R. Horton, a national builder, would bring more than 330 new homes and a new zoning designation for roughly 300 rural acres near the “Town of Friendly People.”

While the development would land on Sugar Hill Road outside town limits, St. George would provide water to the development while Dorchester County Water and Sewer would provide sewer services, said Kiera Reinertsen, the county’s planning director. The development would also add an estimated 100 students to Dorchester School District Four and draw on services and amenities from St. George’s Fire Station Nine, Davis-Bailey Park and the town’s library.

“We’ve never had this many houses come in at one time since I’ve been here,” said Mayor Kevin Hart, who has lived in the town for 35 years.

“We haven’t had a housing development like this in this area before. There’s no way we can stop them, but we have to make plans. We won’t know it works until we see how it goes,” Hart said. ”… Some want to keep our small-town feeling. It’s a tough battle, and we knew it was coming. You can see the progress coming all way up Highway 78. Harleyville is having the same challenge as St. George.

Described as “America’s largest home builder” on its web site, with operations in 45 markets nationwide and 1 million homes constructed since its inception in 1978, D.R. Horton wants to change zoning for the property for the proposed development from agricultural residential, which allows one-acre home lots, to single family residential (R-1), which reduces lot sizes to a third of an acre.

The cluster concept proposed relies on meeting the greenspace requirement by using that of an old golf club adjacent to the property to be developed. Members of the county’s Planning, Development and Building (PDB) Committee reviewed the request for information only on Jan. 8.

In an R-1 zone, said Reinertsen, there is a requirement that 30 percent of developable acreage be conserved as open space and 20 to 25 percent of that is required to be usable open space.

“Cluster developments allow for smaller lot size but preserve greater areas of open space. I believe that the intent is that a lot of that golf course area or all of it will remain open space. I believe they are looking to develop 338 homes over the next 4 to 5 years,” Reinertsen explained during the committee meeting.

“The services are in place to support a development like this.”

He didn’t disagree with the services available to the development, but PDB chairman and County Councilman David Chinnis took issue with two other factors in the cluster proposal. One point of contention Chinnis raised was the development’s cluster design, which he said not only depends on a housing community having accessible green space nearby, but also that the green space is developable.

“I see some open space that is created as open space because the development possibilities are nearly zero, because of the disconnect from the property. I need to know how they intend to connect it. If they’re getting credit for open space, I expect it to be something that is usable, not just something that is imaginary. Cluster ordinance benefits only really apply if it’s developable green space,” said Chinnis, explaining later to The Post and Courier that the spirit of the county’s cluster development ordinance was to create something similar to community pocket parks.

The benefit to homeowners is green space around their homes, he said, while the benefit to the developer is that it costs less to install utilities when homes are closer together.

D.R. Horton’s proposal still must clear several more bureaucratic hurdles, including a second review by the PDB with a vote, and three readings with votes by the full County Council.

if you’re looking to buy a home, you’ve probably been paying close attention to mortgage rates. Over the last couple of years, they hit record lows, rose dramatically, and are now dropping back down a bit. Ever wonder why?

The answer is complicated because there’s a lot that can influence mortgage rates. Here are just a few of the most impactful factors at play.

Inflation and the Federal Reserve

The Federal Reserve (Fed) doesn’t directly determine mortgage rates. But the Fed does move the Federal Funds Rate up or down in response to what’s happening with inflation, the economy, employment rates, and more. As that happens, mortgage rates tend to respond. Business Insider explains:

“The Federal Reserve slows inflation by raising the federal funds rate, which can indirectly impact mortgages. High inflation and investor expectations of more Fed rate hikes can push mortgage rates up. If investors believe the Fed may cut rates and inflation is decelerating, mortgage rates will typically trend down.”

Over the last couple of years, the Fed raised the Federal Fund Rate to try to fight inflation and, as that happened, mortgage rates jumped up, too. Fortunately, the expert outlook for inflation and mortgage rates is that both should become more favorable over the course of the year. As Danielle Hale, Chief Economist at Realtor.com, says:

“[Mortgage rates will continue to ease in 2024 as inflation improves . . .”

There’s even talk the Fed may actually cut the Fed Funds Rate this year because inflation is cooling, even though it’s not yet back to their ideal target.

The 10-Year Treasury Yield

Additionally, mortgage companies look at the 10-Year Treasury Yield to decide how much interest to charge on home loans. If the yield goes up, mortgage rates usually go up, too. The opposite is also true. According to Investopedia:

“One frequently used government bond benchmark to which mortgage lenders often peg their interest rates is the 10-year Treasury bond yield.”

Historically, the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate has been fairly consistent, but that’s not the case recently. That means, there’s room for mortgage rates to come down. So, keeping an eye on which way the treasury yield is trending can give experts an idea of where mortgage rates may head next.

Bottom Line

With the Fed meets, experts in the industry will be keeping a close watch to see what they decide and what impact it’ll have on the economy.

The Federal Reserve held interest rates steady on Wednesday but signaled that rates could fall in the coming months if inflation continues to cool.

He cautioned, however, that the economy remains unpredictable and said the central bank would proceed cautiously. ”The economic outlook is uncertain and we remain highly attentive to inflation risks,” Powell said.

The Fed has been pleasantly surprised by the rapid drop in inflation in recent months. Core prices in December — which exclude food and energy prices — were up just 2.9% from a year ago, according to the Fed’s preferred inflation yardstick. That’s a smaller increase than the 3.2% core inflation rate that Fed officials had projected in December.

If that positive trend continues, the Fed may be able to start cutting interest rates as early as this spring. However, he sounded doubtful about a rate cut at the Fed’s next meeting in March as many investors in Wall Street had hoped for. The comments disappointed investors, with the Dow Jones Industrial Average tumbling 317 points.

Investors are still hopeful about a rate cut in May, with markets putting the likelihood of that at better than 90%.

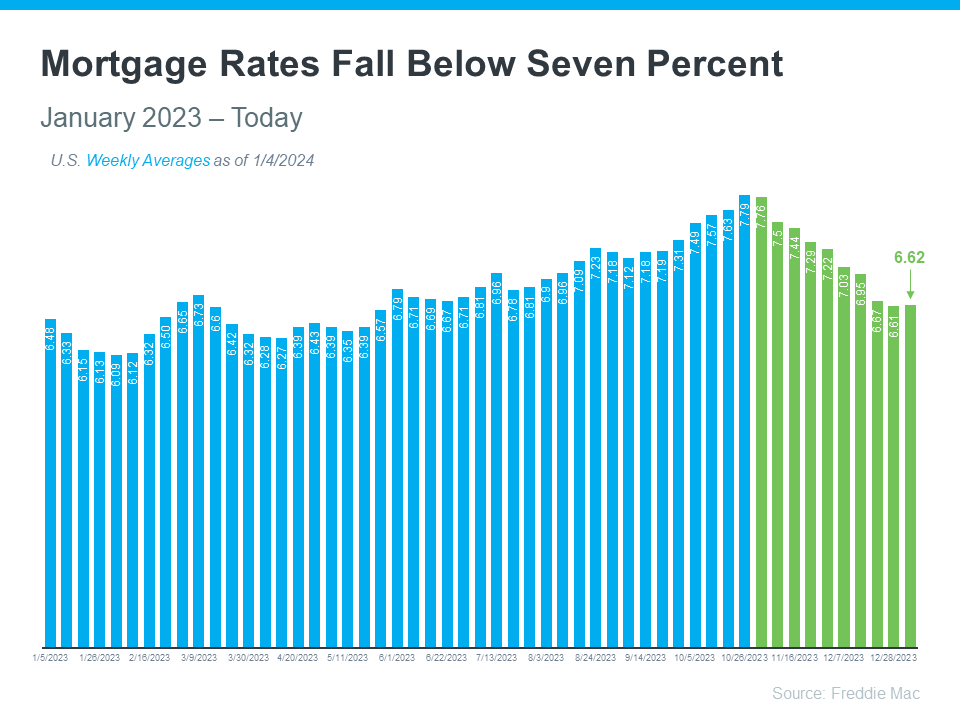

If you want to buy a home, it’s important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph below) and many analysts predict a continued easing of mortgages rates throughout 2024.

This recent trend is great news for buyers. As a recent article from Bankratesays:

“The rate cool-off somewhat eases the housing affordability squeeze.”

And according to Edward Seiler, AVP of Housing Economics and Executive Director of the Research Institute for Housing America at the Mortgage Bankers Association (MBA):

“MBA expects that affordability conditions will continue to improve as mortgage rates decline . . .”

Here’s a bit more context on how this could help with your plans to buy a home.

How Mortgage Rates Affect Your Search for a Home

Understanding the connection between mortgage rates and your monthly home payment is crucial for understanding the sales price you can afford. The chart below illustrates how your ability to afford a home changes when mortgage rates shift. (see chart below):

More information about interest rates at Freddie Mac

Newcomers to S.C. greatly accelerated during the pandemic years as remote employment took hold and that trend has continued. South Carolina was recently crowned the fastest-growing state in the nation by the U.S. Census Bureau based on percentage growth, adding roughly 90,000 additional residents to the population.

Top 10 States or State Equivalent by Percent Growth: 2022 to 2023

Rank

Geographic Area

April 1, 2020 (Estimates Base)

July 1, 2022

July 1, 2023

Percent Growth

1

South Carolina

5,118,422

5,282,955

5,373,555

1.7

2

Florida

21,538,216

22,245,521

22,610,726

1.6

3

Texas

29,145,459

30,029,848

30,503,301

1.6

4

Idaho

1,839,117

1,938,996

1,964,726

1.3

5

North Carolina

10,439,459

10,695,965

10,835,491

1.3

6

Delaware

989,946

1,019,459

1,031,890

1.2

7

District of Columbia

689,548

670,949

678,972

1.2

8

Tennessee

6,910,786

7,048,976

7,126,489

1.1

9

Utah

3,271,614

3,381,236

3,417,734

1.1

10

Georgia

10,713,771

10,913,150

11,029,227

1.1

This population boom created more demand for housing, but inventory has been constrained, keeping prices afloat and putting pressures on rents.

The population growth is mainly concentrated in larger cities with populations declining in some rural areas. Local governments increasingly engage in managing growth and pursuing affordable housing options for workforce.

Mortgage interest rates have fallen from their peak of nearly 8 percent in 2023, and many financial experts speculate interest rates will continue to moderate. Inventory is expected to rise, and lower interest rates should help make homes more affordable. Whether the rising supply can keep up with demand remains to be seen.