The interest rate is a critical factor influencing your mortgage’s monthly payment. A higher rate translates to greater overall interest costs and, consequently, higher monthly payments. Conversely, a lower rate reduces the interest paid, leading to lower monthly installments.

A small change can significantly impact the overall cost of your loan. A 1% interest rate drop can increase their buying power by about 10%, allowing a buyer to afford more home for the same monthly payment.

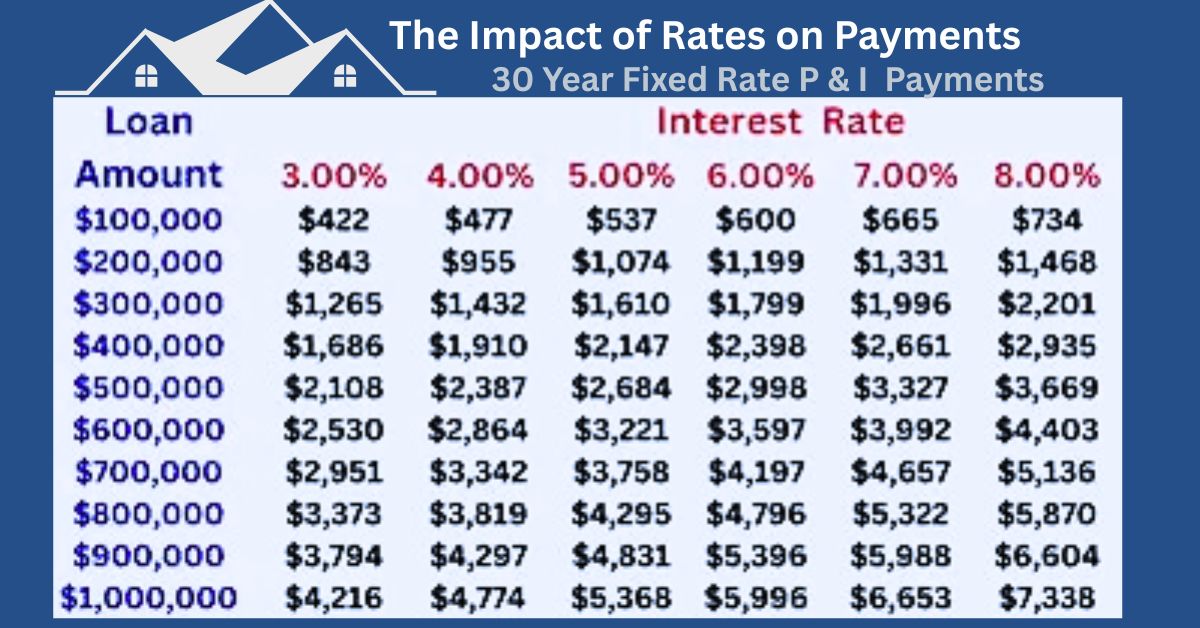

To illustrate this effect, consider the following examples using a $300,000, 30-year fixed-rate mortgage:

- Scenario 1 (5% Rate): The monthly payment is approximately $1,610.

- Scenario 2 (4% Rate): The monthly payment drops to approximately $1,432.

This 1% difference in the interest rate results in a monthly savings of $178, which accumulates into significant savings over the mortgage’s term.

Factors that Influence Your Interest Rate

When shopping for a mortgage, securing the best possible interest rate is a primary goal. Several factors influence the rate you receive, and by focusing on these areas, you can potentially lower your overall borrowing costs.

- Credit Score: A higher credit score is strongly correlated with a lower interest rate. To improve your score, Roland Wilcox of Sierra Capital Mortgage in Pasadena, California, recommends:

- Consistently paying all bills on time.

- Keeping credit card balances below 30% of the credit limit.

- Maintaining older credit accounts.

- Diversifying the types of credit you use.

- Down Payment Amount: Making a larger down payment can help you qualify for a more favorable interest rate.

- Loan Term: While longer loan terms typically result in lower monthly payments, they usually lead to higher total interest costs over the life of the loan. Example: A 15 year mortgage would typically have a lower rate than a 30 year mortgage.

- Mortgage Type: Certain mortgage options, such as loans backed by government entities, may be offered with lower interest rates. There are also state programs that have lower than market rates from some qualified buyers. Example: SC State Housing Authority.

Exploring Options for a Lower Rate

- Shop Around: Compare rates from several lenders before making a final decision.

- Refinance Your Existing Mortgage: If interest rates have significantly decreased since you obtained your original mortgage, refinancing could be a beneficial option. Refinancing involves taking out a new loan to pay off the existing one, and if the new rate is lower, it can reduce your monthly payments.

If you need assistance buying a house and shopping for a mortgage – I can help, feel free to contact me!

Gena Glaze 843-343-8239

Discover more from Real Estate Matters in Charleston SC - Gena Glaze

Subscribe to get the latest posts sent to your email.