CLOSED SALES – There were 1,381 closed sales in September of 2025, up 8.9% from September of 2024.

PRICE PER SQFT – The average price per sqft for all residential property types was at $296,up 0.7%

SALES PRICE – The median sales price closed out at $423,930 in September 2025, up+3.4% over September of 2024 and the average sales price for August 2025 was $$634,965 The median sales price is still holding steady. It has been in a tight band between 400k and 425K most of the last 3 years.

NEW WRITTEN SALES (Pending) – There were 1,355 new written sales in September 2025, up 0.8% versus September 2024.

INVENTORY – Approximately 2,016 new listings (all property types) came online in September of 2025, which is up 0.1% from September 2024 and the average Days on Market was at 52 (up 20.9%) with 3.7 months of inventory

NEW CONSTRUCTION

New homes represent 23% of the available inventory

18% of all closings in Charleston County were new construction

35% of all closings in Dorchester County were new construction

53% of all closings in Berkeley County were new construction

APR (Annual Percentage Rate) includes costs and fees associated with the loan. The interest rate does not. The interest rate is simply the rate you pay on the loan, excluding any other costs.

Looking at the interest rate alone is not an effective way to evaluate a loan. The APR is much more effective, as it factors in the interest rate PLUS any other costs to finance the loan, providing a much more holistic view.

When you apply for a loan, you should always be able to see both the interest rate and the APR. If you don’t, ask your lender to provide both.

If you compare two loans with the same interest rate (note rate) and the APR is higher on one – you should find out what the additional costs are. This comparison will help you evaluate the loan products more effectively.

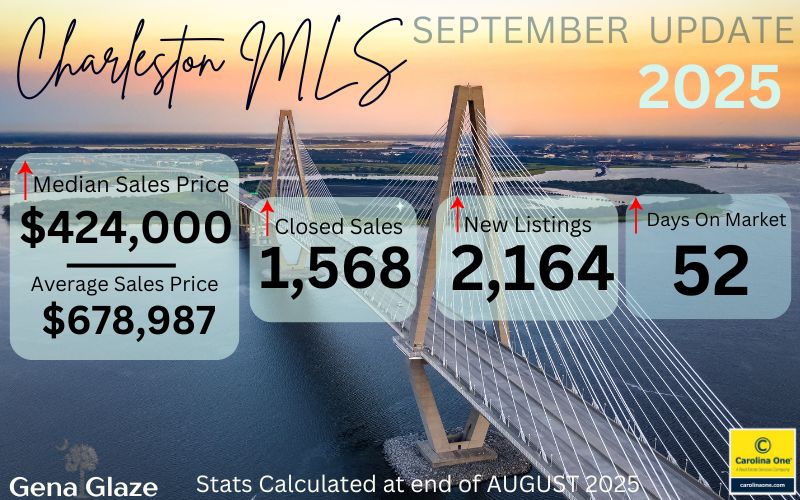

SALES PRICE – The median sales price closed out at $424,000 in August 2025, up+1.2% over August of 2024 and the average sales price for August 2025 was $678,987.

NEW WRITTEN SALES (Pending) – There were 1,568 new written sales in August 2025, up 11.9% versus August 2024. Approximately 480 of these sales were new construction, up+15.7%

CLOSED SALES – There were 1,547 closed sales in August of 2025, up 0.9% from August of 2024. New construction closed sales accounted for 28% of these sales, up +11.6%

INVENTORY – Approximately 2,164 new listings (all property types) came online in August of 2025, which is up +11.1% from August 2024 and the average Days on Market was at 52 (up 23.8%) with 4.1 months of inventory. 581 of August’s new listings were new construction, up 26.3% Previously owned homes (non-new construction) days on market was up+47.1%.

PRICE PER SQFT – The average price per sqft for all residential property types was at $230, up 3.6%.

SHOWINGS PER LISTING – 3.8 | down -7.3%

AUGUST STATS BY COUNTY:

Berkeley – The median sales price was $399,923 | up +0.2% The average sales price was $466,057 and the average days on market was 54. Closed sales (503) were up 0.6%, year over year, 45% of the closed sales were new construction (up 10%)

Charleston – The median sales price was $675,000 | up +12.5%. The average sales price was $1,031,255 and the average days on market was 49 | up+48.5%. Closed sales (652) | up +2.5% New Construction represented 12 % of these sales (up 65.2%).

Dorchester – The median sales price was $372,500 | up +0.5%. The average sales price was $385,433 and the average days on market was 41 | up +32.3%. Closed sales (317) were down -11.7%. New Construction represented 40% of the closed sales.

SALES PRICE – The median sales price closed out at $430,000 in July 2025, up +1.2% over July of 2024 and the average sales price for July 2025 was $620,556

NEW WRITTEN SALES (Pending) – There were 1,577 new written sales in July 2025, up 11% versus July 2024.

CLOSED SALES – There were 1,719 closed sales in July of 2025, up 7.4% from July of 2024.

INVENTORY – Approximately 2,290 new listings (all property types) came online in July 2025, which is up +5% from July 2024 and the average Days on Market was at 45 with 3.6 months of inventory (up 16%). 1712 of July’s new listings were existing homes (non-new construction) this category is at 3.9 months of inventory, up 30%

PRICE PER SQFT – The average price per sqft for all residential property types was at $289 but for resales (non-new construction) it was calculated at $311 / sqft. Despite a fairly stable Median Sale Price, this increase in price per sqft suggests consumers are getting a smaller house for the money (higher Sold $/sqft).

New Construction – New construction represents about 36% of the closings in MLS. In Berkeley County new construction represents 56% of all closed sales.

JULY STATS BY COUNTY:

Berkeley – The median sales price was $395,000 | down -0.3%. The average sales price was $500,965 and the average days on market was 45 | up +21.6%

Charleston – The median sales price was $623,225 | down -1.7%The average sales price was $870,712 and the average days on market was 39 | up +25.8%

Dorchester – The median sales price was $389,500 | up +2.3%. The average sales price was $417,491 and the average days on market was 42 | up +20%

JULY STATS – QUICK VIEW OF MUNICIPLAITIES:

Goose Creek– The median sales price was $314,900 | down -4.3% The average sales price was $317,088 |

Hanahan – The median sales price was $365,000 | down -1.3%, The average sales price was $431,131

Summerville – The median sales price was $399,990 | no change 0.0%, The average sales price $431,092

North Charleston – The median sales price was $346,450 | down -0.4% The average sales price was $392,508

Charleston / West Ashley – The median sales price was $585,000 | down -8.5% The average sales price was $875,381

Mount Pleasant -The median sales price was $955,000 | up +9.1%, The average sales price was $1,127,187

Daniel Island -The median sales price was $1,600,000 | up +7.4% The average sales price was $1,314,444

James Island The median sales price was $338,000 | down -47.6%, The average sales price was $338,000

February 2024 Update for the entire Charleston MLS:

NEW SALES – Pending – There were 1379 new written sales in January 2025, down -6.1% versus January of 2024.

CLOSED SALES – There were 1045 closed sales in January of 2025, up 2.8% from January of 2024

SALES PRICE – The Median sales price closed out at $415,917, up 0.2% over January of 2024 and the average sales price for January 2024 was $631,715

INVENTORY – Approximately 1,907 new listings came online in January 2025, which is up +2.3% from January 2024 and the average Days on Market was at 50, up 28.2% from January of 2024 with 2.7 months of inventory.

In today’s market, more and more home buyers are getting assistance with their down payment in the form of gift funds from friends and family. According to a recent study, in 2023, 39% of home buyers who financed their home with a mortgage loan used gifted funds as at least one source for their down payment, up nine percentage points from 2018. While it’s great to have help, there are rules around financial gifts that you need to know in order to smoothly navigate the process.

What is a down payment gift?

Down payment money is considered a “gift” when people, usually friends or family, financially contribute money that will help the home buyer pay for a down payment on a home. there is generally no limit on how much a borrower is allowed to receive as a gift

Who is eligible to Gift you down payment money?

Depending on the loan type, gifts can come from the buyer’s relative, employer, or close friend with a “clearly defined and documented” interest in the borrower, or a charitable organization, governmental agency, or a public entity that has a program providing home ownership assistance for low and moderate-income families or first-time home buyers. However, donations for down payments cannot come from people who are directly affiliated with the home buying transaction which includes builders, developers, or real estate agents.

What are the rules for mortgage down payments?

For Fannie Mae backed loans, a minimum borrower contribution from the borrower’s own funds is not required. This means that 100% of the money that is needed to make up the down payment can come from a gift. On the other hand, with FHA loans, the borrower is required to provide a minimum personal cash investment of at least 3.5% for the down payment. regardless of the loan type, gift funds must be a “bona fide gift,” and not a loan that requires repayment.

While there is no limit to how much money you can accept as a gift for a home down payment, when you’re going through the mortgage loan application process, you’ll need to make sure that you have proper documentation of the gift money in the form of a letter, with specific requirements outlined by your lender, from the donor of the funds. this is required to show your letter that you don’t owe someone a large sum of money that you won’t be able to pay back on top of your monthly mortgage payment.

Year over Year Review (2023 vs. 2024): Closed sales up 13.7% Median Sales price up 2.3 %

December 2024 stats for the entire Charleston MLS:

NEW SALES – Pending – There were 1106 new written sales in December 2024, a. predictor of future closed sales, which was up 6.3% versus December of 2023. YTD was up 2.4%.

CLOSED SALES – There were 1382 closed sales in December of 2024, up 13.7% from December of 2023 and up a negligible 1.1% YTD, compared to 2024.

SALES PRICE – The Median sales price closed out at $414,296, up 2.30% over December of 2024 and The Year-to-date median sales price was up 4.1% over 2024. The average sales price for December 2024 was $612,457.

INVENTORY – Approximately 1165 new listings came online in December 2024, which is down -6.9% from December 2023 but up YTD 10.8% The market as a whole had approximately 2.6 months of inventory at December’s end with the average Days on Market at 50, up 25% from December of 2023 and up 14% year to date.

The National Association of Realtor’s economists recently weighed in on home sales, mortgage rates, the economy and changing buyer demographics and its effect on real estate for the year ahead.

Lawrence Yun, chief economist of the National Association of REALTORS®, along with NAR’s Deputy Chief Economist, Jessica Lautz, shared data and forecasts..

Their updated estimates show that the housing market is still dramatically undersupplied, and they estimate that U.S. housing stock is 3.7 million units below what is needed.

High mortgage rates and rising home prices have put a damper on affordability and are directly related to the supply shortage. Building more houses is essential but builders are also contending with high interest rates.

There is no silver bullet to alleviating this ongoing shortage but there are options being considered such as, accessory dwelling units (ADUs), Community Land Trusts, condominium conversions, and manufactured homes. They will continue to study this topic and work to uncover potential solutions.

Yun released a rosier forecast for the housing market for 2025 and 2026, with an outlook for higher home sales and moderating mortgage rates.

Here’s an overview of NAR’s predictions on key housing indicators for the year ahead.

Home Sales to Rise

With improving job numbers and recent gains in the stock market, more Americans may be motivated to act, Yun said.

Here’s Yun’s forecast over the next two years:

2025 sales projection: Existing home sales to rise 9% year-over-year; New home sales to jump by 11%.

2026 sales projection: Existing-home sales to rise 13% year-over-year; new home sales to increase by 8%.

Mortgage Rates to Moderate

The trajectory of mortgage rates will have a major bearing on how the housing market will fare, Yun said.

Mortgage rates may moderate but buyers may not see that anytime soon, Yun said. “Mortgage rates will not decline in tandem”… “With a large budget deficit, there’s less mortgage money available…. A large budget deficit will prevent mortgage rates from going down to 4%”

Nevertheless, the “locked-in” effect of homeowners feeling stuck-in-place with low 2% or 3% mortgage rates from recent years will lessen over time, as personal milestones (births, deaths, marriages, graduations, new jobs,etc.) trigger real estate moves.

Home Prices Increases Slowly After Rapid Rises

While homeowners have enjoyed record-breaking equity gains, home buyers’ have been struggling with affordability. A typical homeowner has accumulated $147,000 in housing wealth just over the last five years, according to NAR’s research. As a result, the spread in median net worth between homeowners and renters continues to grow. It stands at $415,000 for homeowners versus $10,000 for renters, Yun said.

“The strong price increases cannot be sustainable for another five years, or America will be divided … with only a few getting to experience the tremendous housing wealth,” Yun said. “If we bring more supply to the housing market, home price increases will not be as outrageous … and will be more in line with wages.”

Yun’s forecast:

2025 median home price: $410,700; up 2% over 2024.

2026 median home price: $420,000, up 2% over 2025.

A Different Type of Buyer Emerges

The profile of home buyers are changing, Lautz said, presenting data from NAR’s newly released 2024 Profile of Home Buyers and Sellers. Here’s a few of the changes observed in the report:

More buyers are skipping the mortgage. all-cash buyers have surged to record highs, accounting for 26% of home sales over the past year. Thirty-one percent of repeat buyers paid all-cash for their next home purchase.

First-time buyers are getting older. The median age of a first-time home buyer was 38, an all-time high. Twenty-five percent of first-time buyers used a gift or loan from a relative or friend for their home purchase; 20% took money out of financial assets like stocks, 401ks or cryptocurrency to afford homeownership; and 7% used inheritance money for their purchase—a record high, Lautz noted. First-time buyers are coming up with the highest down payments in nearly 30 years—at 9%—in order to afford the higher home prices.

The allure of cities grows. The pandemic may have unleashed a trend of suburban movers, but people are now heading back to city centers—the largest uptick in a decade, Lautz said.

More buyers are pooling their money. The number of multigenerational households surged to an all-time high of 17% over the past year. “The number one reason is for cost savings,” Lautz said. “They’re combining incomes” in order to afford homeownership. They’re also buying a multigenerational home to take care of aging parents or because of young adults are moving back home, Lautz noted.

Single women buyers continue to outpace single men buyers. A drop in marriage rates has triggered more consumers to enter the housing market on their own. Single women held a 24% share of the home-purchase market over the past year. For single men, it was 11%.

NEW SALES – Pending (Ratified contracts) – There were 1,266 new written sales in November 2024, a. predictor of future closed sales, which was up 12% versus November of 2023. YTD was up 3.6% at end of November. However, last week saw 167 properties go under contract market wide, down -15% to the same week last year.

CLOSED SALES – There were 1331 closed sales in November of 2024, up 3.9% from November of 2023 and up a negligible 0.1% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $419,000, up 5.4% over November of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for Movember 2024 was $611,213. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 30 months- 2 1/2 years!

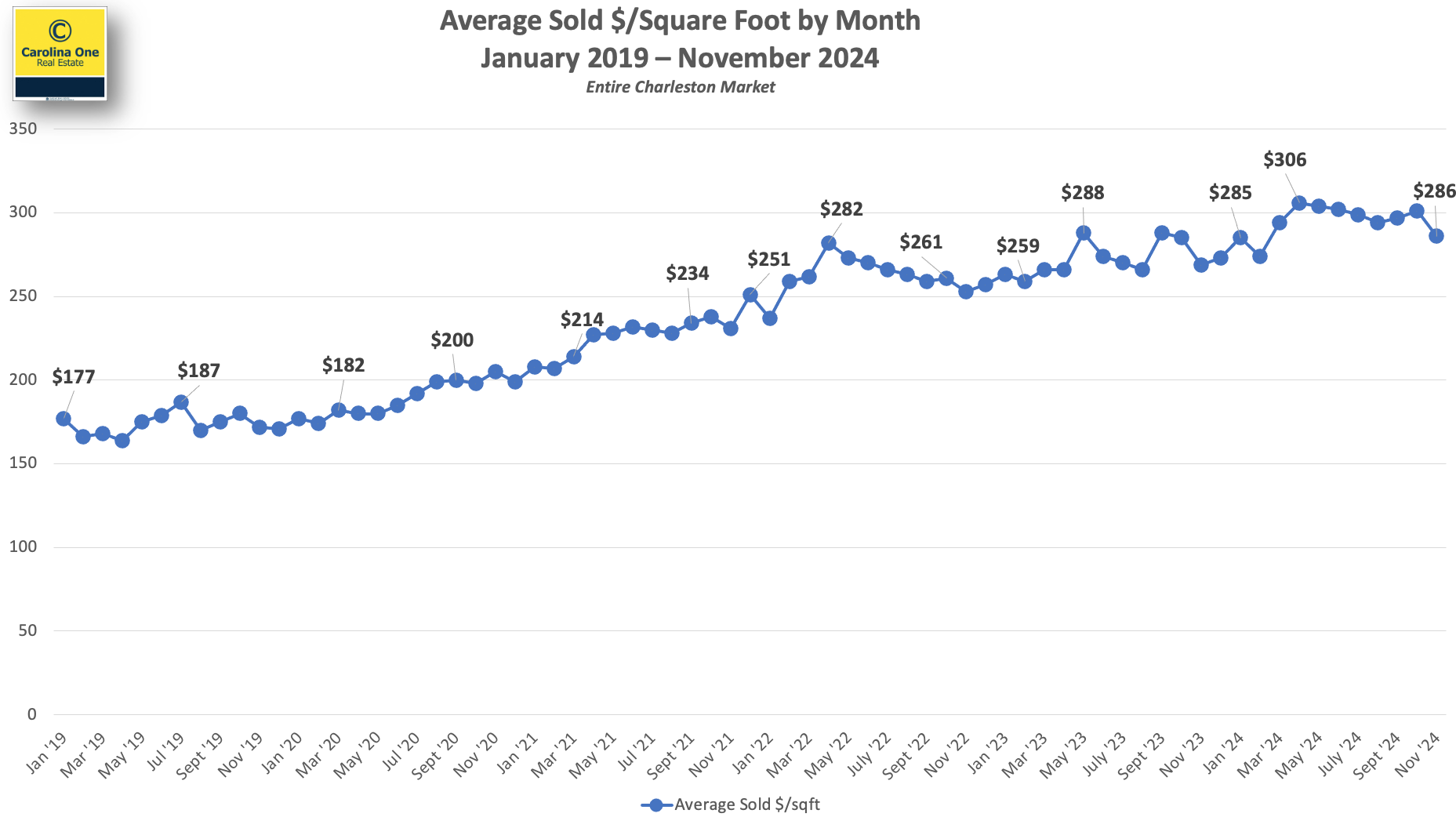

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $286 /sqft

INVENTORY – Approximately 1581 new listings came online in November 2024, which is up 0.6% from November 2023 and up YTD 11.7%

We still need roughly 2,500 additional listings market wide to achieve a balanced market (5 months of inventory)

The market as a whole has approximately 2.6 months of inventory with the Days on Market at 29. See absorption rate by area below:

NEW CONSTRUCTION – New construction represents 49% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – Represent a combined 0.7% of all available listings

If you have questions or have a real estate need, please don’t hesitate to contact me!

NEW SALES – Pending (Ratified contracts) – There were 1,393 new written sales in October 2024, a predictor of future closed sales, which was up 2% versus October of 2023. YTD was down -4%

However, Last week 242 properties went under contract market wide, which was up +16% compared to the same week last year.

CLOSED SALES – FLAT – There were 1,354 closed sales in October of 2024, down a negligible -0.7% from October 2023 and down -0.4% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $415,685, up 3% over October of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for October 2024 was $644,758. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 27+ months.

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $301 /sqft

INVENTORY – Approximately 1961 new listings came online in October 2024, which is up 4% from October 2023 and Third quarter Inventory levels were up 12.6% over 2023.

There were approximately 2.7 months of Inventory calculated in October 2024, with the median Days on Market at 25, up 56.2% from October 2023 and the median days on market up 46.7% YTD.

We still need additional listings market wide to achieve a balanced market of 5 months of inventory.

Absorption rate by Area

NEW CONSTRUCTION – New construction represents 48% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – have declined even further to a combined 0.7% of all available listings This market continues to be basically nonexistent and there are very few “newly distressed” properties in the pipeline.

MM+ We are roughly double the monthly pre-pandemic sales levels of over Million dollar plus properties. This market segment remains robust.

If you have questions or have a real estate need, please don’t hesitate to contact me!