Year over Year Review (2023 vs. 2024): Closed sales up 13.7% Median Sales price up 2.3 %

December 2024 stats for the entire Charleston MLS:

NEW SALES – Pending – There were 1106 new written sales in December 2024, a. predictor of future closed sales, which was up 6.3% versus December of 2023. YTD was up 2.4%.

CLOSED SALES – There were 1382 closed sales in December of 2024, up 13.7% from December of 2023 and up a negligible 1.1% YTD, compared to 2024.

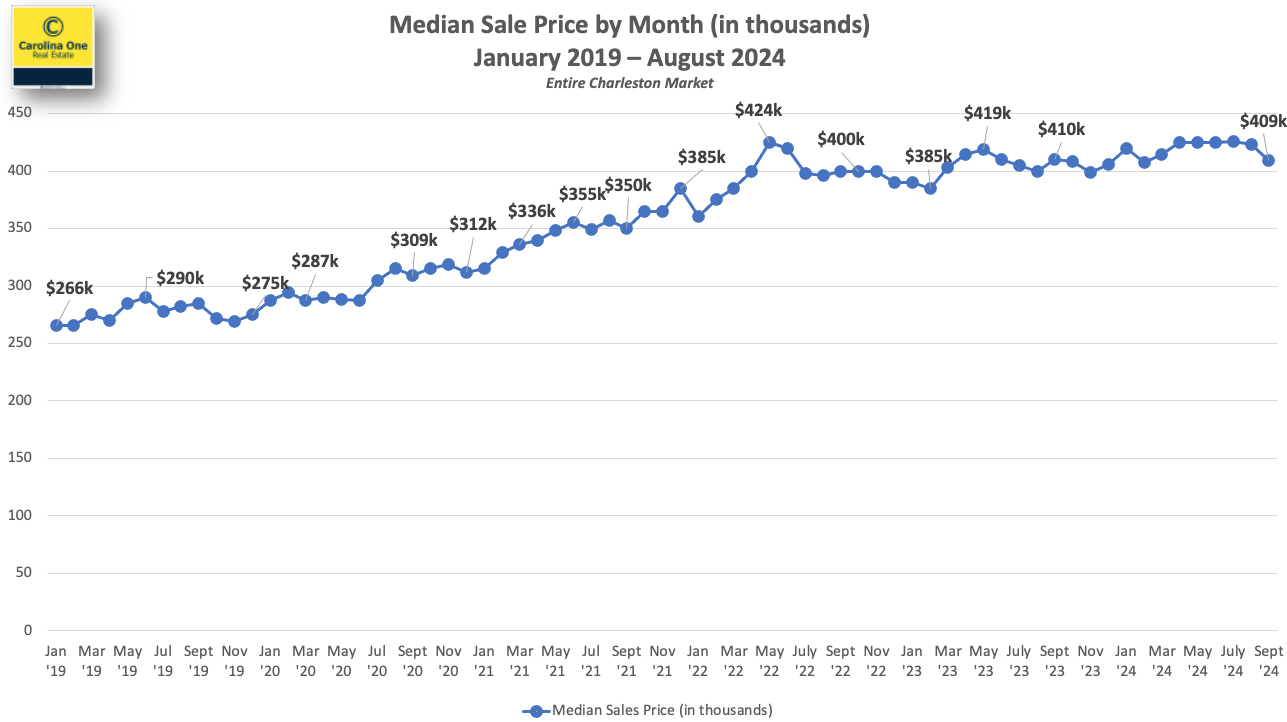

SALES PRICE – The Median sales price closed out at $414,296, up 2.30% over December of 2024 and The Year-to-date median sales price was up 4.1% over 2024. The average sales price for December 2024 was $612,457.

INVENTORY – Approximately 1165 new listings came online in December 2024, which is down -6.9% from December 2023 but up YTD 10.8% The market as a whole had approximately 2.6 months of inventory at December’s end with the average Days on Market at 50, up 25% from December of 2023 and up 14% year to date.

The National Association of Realtor’s economists recently weighed in on home sales, mortgage rates, the economy and changing buyer demographics and its effect on real estate for the year ahead.

Lawrence Yun, chief economist of the National Association of REALTORS®, along with NAR’s Deputy Chief Economist, Jessica Lautz, shared data and forecasts..

Their updated estimates show that the housing market is still dramatically undersupplied, and they estimate that U.S. housing stock is 3.7 million units below what is needed.

High mortgage rates and rising home prices have put a damper on affordability and are directly related to the supply shortage. Building more houses is essential but builders are also contending with high interest rates.

There is no silver bullet to alleviating this ongoing shortage but there are options being considered such as, accessory dwelling units (ADUs), Community Land Trusts, condominium conversions, and manufactured homes. They will continue to study this topic and work to uncover potential solutions.

Yun released a rosier forecast for the housing market for 2025 and 2026, with an outlook for higher home sales and moderating mortgage rates.

Here’s an overview of NAR’s predictions on key housing indicators for the year ahead.

Home Sales to Rise

With improving job numbers and recent gains in the stock market, more Americans may be motivated to act, Yun said.

Here’s Yun’s forecast over the next two years:

2025 sales projection: Existing home sales to rise 9% year-over-year; New home sales to jump by 11%.

2026 sales projection: Existing-home sales to rise 13% year-over-year; new home sales to increase by 8%.

Mortgage Rates to Moderate

The trajectory of mortgage rates will have a major bearing on how the housing market will fare, Yun said.

Mortgage rates may moderate but buyers may not see that anytime soon, Yun said. “Mortgage rates will not decline in tandem”… “With a large budget deficit, there’s less mortgage money available…. A large budget deficit will prevent mortgage rates from going down to 4%”

Nevertheless, the “locked-in” effect of homeowners feeling stuck-in-place with low 2% or 3% mortgage rates from recent years will lessen over time, as personal milestones (births, deaths, marriages, graduations, new jobs,etc.) trigger real estate moves.

Home Prices Increases Slowly After Rapid Rises

While homeowners have enjoyed record-breaking equity gains, home buyers’ have been struggling with affordability. A typical homeowner has accumulated $147,000 in housing wealth just over the last five years, according to NAR’s research. As a result, the spread in median net worth between homeowners and renters continues to grow. It stands at $415,000 for homeowners versus $10,000 for renters, Yun said.

“The strong price increases cannot be sustainable for another five years, or America will be divided … with only a few getting to experience the tremendous housing wealth,” Yun said. “If we bring more supply to the housing market, home price increases will not be as outrageous … and will be more in line with wages.”

Yun’s forecast:

2025 median home price: $410,700; up 2% over 2024.

2026 median home price: $420,000, up 2% over 2025.

A Different Type of Buyer Emerges

The profile of home buyers are changing, Lautz said, presenting data from NAR’s newly released 2024 Profile of Home Buyers and Sellers. Here’s a few of the changes observed in the report:

More buyers are skipping the mortgage. all-cash buyers have surged to record highs, accounting for 26% of home sales over the past year. Thirty-one percent of repeat buyers paid all-cash for their next home purchase.

First-time buyers are getting older. The median age of a first-time home buyer was 38, an all-time high. Twenty-five percent of first-time buyers used a gift or loan from a relative or friend for their home purchase; 20% took money out of financial assets like stocks, 401ks or cryptocurrency to afford homeownership; and 7% used inheritance money for their purchase—a record high, Lautz noted. First-time buyers are coming up with the highest down payments in nearly 30 years—at 9%—in order to afford the higher home prices.

The allure of cities grows. The pandemic may have unleashed a trend of suburban movers, but people are now heading back to city centers—the largest uptick in a decade, Lautz said.

More buyers are pooling their money. The number of multigenerational households surged to an all-time high of 17% over the past year. “The number one reason is for cost savings,” Lautz said. “They’re combining incomes” in order to afford homeownership. They’re also buying a multigenerational home to take care of aging parents or because of young adults are moving back home, Lautz noted.

Single women buyers continue to outpace single men buyers. A drop in marriage rates has triggered more consumers to enter the housing market on their own. Single women held a 24% share of the home-purchase market over the past year. For single men, it was 11%.

NEW SALES – Pending (Ratified contracts) – There were 1,266 new written sales in November 2024, a. predictor of future closed sales, which was up 12% versus November of 2023. YTD was up 3.6% at end of November. However, last week saw 167 properties go under contract market wide, down -15% to the same week last year.

CLOSED SALES – There were 1331 closed sales in November of 2024, up 3.9% from November of 2023 and up a negligible 0.1% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $419,000, up 5.4% over November of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for Movember 2024 was $611,213. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 30 months- 2 1/2 years!

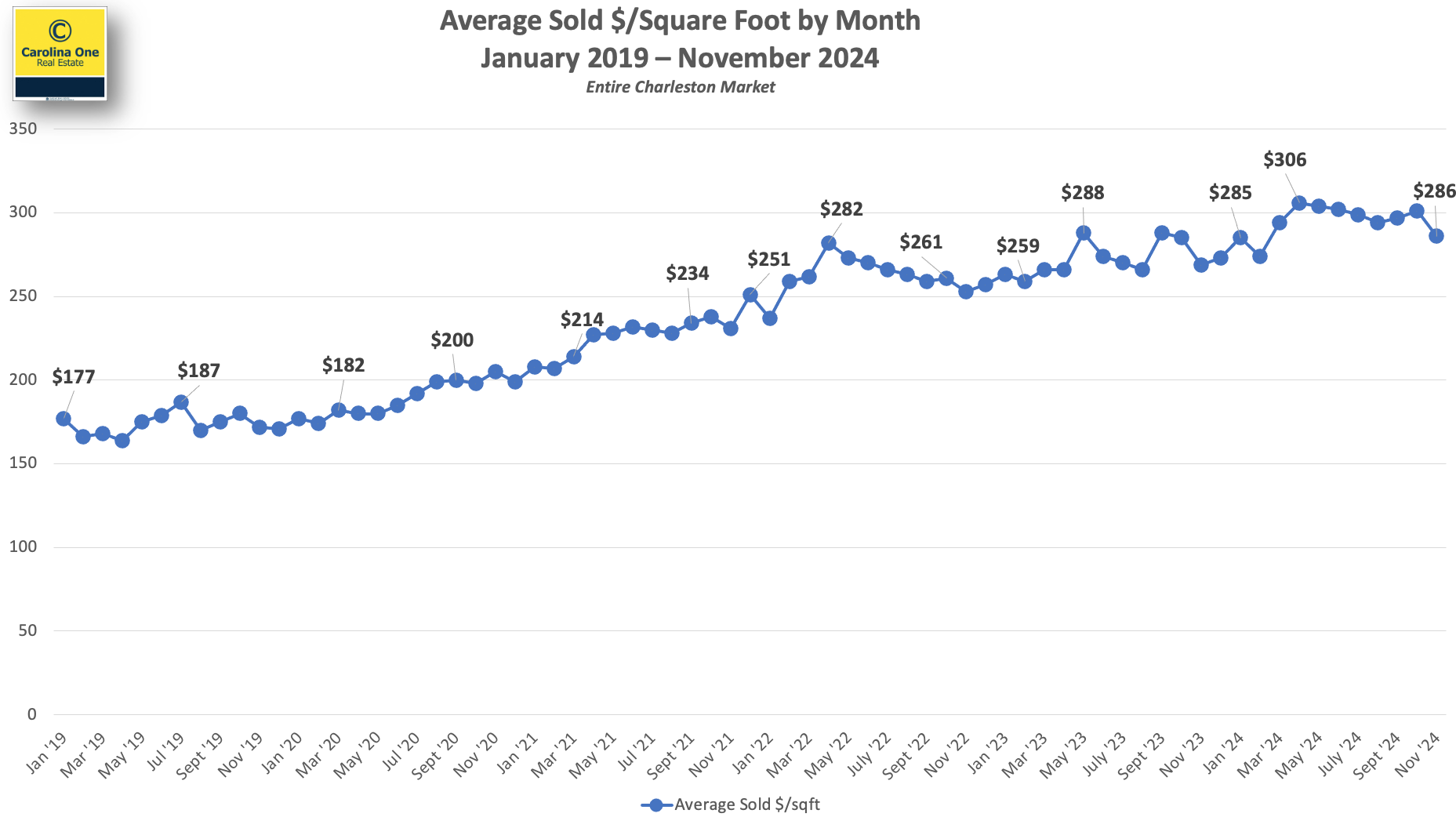

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $286 /sqft

INVENTORY – Approximately 1581 new listings came online in November 2024, which is up 0.6% from November 2023 and up YTD 11.7%

We still need roughly 2,500 additional listings market wide to achieve a balanced market (5 months of inventory)

The market as a whole has approximately 2.6 months of inventory with the Days on Market at 29. See absorption rate by area below:

NEW CONSTRUCTION – New construction represents 49% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – Represent a combined 0.7% of all available listings

If you have questions or have a real estate need, please don’t hesitate to contact me!

NEW SALES – Pending (Ratified contracts) – There were 1,393 new written sales in October 2024, a predictor of future closed sales, which was up 2% versus October of 2023. YTD was down -4%

However, Last week 242 properties went under contract market wide, which was up +16% compared to the same week last year.

CLOSED SALES – FLAT – There were 1,354 closed sales in October of 2024, down a negligible -0.7% from October 2023 and down -0.4% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $415,685, up 3% over October of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for October 2024 was $644,758. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 27+ months.

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $301 /sqft

INVENTORY – Approximately 1961 new listings came online in October 2024, which is up 4% from October 2023 and Third quarter Inventory levels were up 12.6% over 2023.

There were approximately 2.7 months of Inventory calculated in October 2024, with the median Days on Market at 25, up 56.2% from October 2023 and the median days on market up 46.7% YTD.

We still need additional listings market wide to achieve a balanced market of 5 months of inventory.

Absorption rate by Area

NEW CONSTRUCTION – New construction represents 48% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – have declined even further to a combined 0.7% of all available listings This market continues to be basically nonexistent and there are very few “newly distressed” properties in the pipeline.

MM+ We are roughly double the monthly pre-pandemic sales levels of over Million dollar plus properties. This market segment remains robust.

If you have questions or have a real estate need, please don’t hesitate to contact me!

NEW SALES – Pending (Ratified contracts) – New Written sales, a predictor of future closed sales, were down market wide -1% in September of ’24 versus September of ’23. However, last week 255 properties went under contract market wide, +3% from the same week last year. This is a strong and seasonally appropriate number.

CLOSED SALES – Year To date closed sales were at 13,390 at the end of September 2024. A very small difference from the 13,438 at the same time in 2023.

Third Quarter of 2024 closed sales were at 4,396, which is down 3 percent from 2023 (which had 4,510). As a reference, there were 5018 closed sales in 2022.

There were 1,254 closed sales in September 2024 which is down 11 percent from the 1,411 that we saw in September of 2023. Again, as a reference, there were 1,573 closed sales in September of 2022

SALES PRICE – The Median sale price closed out at $409,085 in September 2024. The Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 27+ months. The average sales price was $627,254 in September 2024.

AVERAGE SOLD PRICE PER SQFT

The median sales price has remained in a tight band but the average price per sqft remains near an all-time high, well above one year ago. Consumers are getting a smaller house for the money. Essentially, homes are continuing to appreciate despite a stable Median Sale Price.

INVENTORY – Approximately 2,000 new listings came online in September 2024, well ahead of last year’s number. Median Days on market was 26.

Inventory was at approximately 4,200 listings in September 2024. While this level of inventory is a significant increase, the gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is still substantial. See chart below. We need approximately 2,100 additional listings market wide to achieve a balanced market (5 months of inventory)

The Charleston market has about ten weeks of inventory as a whole – this can vary by price range and specific location. The most active areas have inventory levels in the 6-10 week range.

NEW CONSTRUCTION – New construction represents 45% of all pending contracts in the MLS and new construction comprises about 36% of the closings.

If you have questions or would like more information, please don’t hesitate to contact me.

Chances are at some point in your life you’ve heard the phrase, home is where the heart is. There’s a reason that’s said so often. Becoming a homeowner is emotional.

So, if you’re trying to decide if you want to keep on renting or if you’re ready to buy a home this year, here’s why it’s so easy to fall in love with homeownership.

Customizing to Your Heart’s Desire

Your house should be a space that’s uniquely you. And, if you’re a renter, that can be hard to achieve. When you rent, you don’t have much control over the upgrades, and you’ve got to be careful how many holes you put in the walls. But when you’re a homeowner, you have a lot more freedom. As the National Association of Realtors (NAR) says:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Whether you want to paint the walls a cheery bright color or go for a dark moody tone, you can match your interior to your vibe. Imagine how it would feel to come home at the end of the day and walk into a space that feels like you.

Greater Stability for the Ones You Love Most

One of the hardest things about renting is the uncertainty of what happens at the end of your lease. Does your payment go up so much that you have to move? What if your landlord decides to sell the property? It’s like you’re always waiting for the other shoe to drop. Jeff Ostrowski, a business journalist covering real estate and the economy, explains how homeownership can give you more peace of mind in a Money Geekarticle:

“Homeownership means you are the boss and have the biggest say in your lifestyle and family decisions. Suppose your kids are in public school and you don’t want to risk having them change schools because your landlord doesn’t renew your lease. Owning a home would remove much of the risk of having to move.”

A Feeling of Belonging

You may also find you feel much more at home in the community once you own a house. That’s because, when you buy a home, you’re staking a claim and saying, I’m a part of this community. You’ll have neighbors, block parties, and more. And that’ll give you the feeling of being a part of something bigger. As the International Housing Association explains:

“. . . homeowning households are more socially involved in community affairs than their renting counterparts. This is due to both the fact that homeowners expect to remain in the community for a longer period of time and that homeowners have an ownership stake in the neighborhood.”

The Emotional High of Achieving Your Dream

You’ll be able to walk up to your front door every day and have that sense of accomplishment welcome you home.

Overview of Benefits – Published by NAR

Appreciation. Historically, real estate has had long-term, stable growth in value and served as a good hedge against inflation. Census data shows the median price of a home jumped from $172,900 in Q4 2000 to $417,700 in Q4 2023. That’s greater than 6% appreciation per year on average.

Equity. Money paid for rent is money that you’ll never see again, but paying your mortgage month over month and year over year lets you build equity ownership interest in your home.

Tax benefits. If you itemize deductions on your federal tax return, the U.S. Tax Code lets you deduct the interest you pay on your mortgage, your property taxes (up to $10,000 according to current tax law), and some of the costs involved in buying a home. Be sure to talk to your accountant to see if it’s advantageous for you to itemize.

Savings. Building equity in your home is a ready-made savings plan. And when you sell, you can generally exclude up to $250,000 ($500,000 for a married couple) of gain without owing any federal income tax. The IRS provide guidance(link is external) on how to qualify for the exclusion.

Predictability. Unlike rent, your fixed-rate mortgage payments don’t rise from year to year. So, as a percentage of your income, your housing costs may actually decline over time. However, keep in mind that property taxes and insurance costs may increase.

Freedom. The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.

Stability. Remaining in one neighborhood for several years allows you and your family time to build long-lasting relationships within the community. It also offers children the benefit of educational and social continuity.

A home is a place that reflects who you are, a safe space for the ones you love the most, and a reflection of all you’ve accomplished.

Let’s connect if you’re ready to buy or sell a home!

Are you feeling a bit unsure about what’s really happening with mortgage rates? That might be because you’ve heard they’re coming down. But then you read somewhere else that they’re up again. And that may leave you scratching your head and wondering what’s true.

The simplest answer is: that what you read or hear will vary based on the time frame they’re looking at. Here’s some information that can help clear up the confusion.

Mortgage Rates Are Volatile by Nature

Mortgage rates don’t move in a straight line. There are too many factors at play for that to happen. Instead, rates bounce around because they’re impacted by things like economic conditions, decisions from the Federal Reserve, and so much more. That means they might be up one day and down the next depending on what’s going on in the economy and the world as a whole.

Take a look at the graph below. It uses data from Mortgage News Daily to show the ebbs and flows in the 30-year fixed mortgage rate since last October:

If you look at the graph, you’ll see a lot of peaks and valleys – some bigger than others. And when you use data like this to explain what’s happening, the story can be different based on which two points in the graph you’re comparing.

For example, if you’re only looking at the beginning of this month through now, you may think mortgage rates are on the way back up. But, if you look at the latest data point and compare it to the peak in October, rates have trended down. So, what’s the right way to look at it?

The Big Picture

Mortgage rates are always going to bounce around. It’s just how they work. So, you shouldn’t focus too much on the small, daily changes. Instead, to really understand the overall trend, zoom out and look at the big picture.

When you look at the highest point (October) compared to where rates are now, you can see they’ve come down compared to last year. And if you’re looking to buy a home, this is big news. Don’t let the little blips distract you. The experts agree, overall, that the larger downward trend could continue this year.

Despite the ups and downs, many analysists predict mortgage rates will, over-all, move in a slow declining path as the year progresses, but many factors can influence the trajectory and so only time will tell.

Sellers, including home builders, will sometimes use 2-1 buydowns as an incentive for potential purchasers

A 2-1 buydown is a concession or incentive negotiated with a seller or builder that temporarily reduces a buyer’s mortgage interest rate by 2 percentage points the first year and 1 percentage point the second year of your mortgage. The third year the interest rate goes back to the fixed rate obtained from the lender.

A 2-1 buydown is a type of financing that lowers the interest rate on a mortgage for the first two years before it rises to the regular, permanent rate.

The rate is typically two percentage points lower during the first year and one percentage point lower in the second year.

Sellers, including home builders, may offer a 2-1 buydown to make a property more attractive to buyers.

2-1 buydowns can be a good deal for homebuyers, provided that they will be able to afford the higher monthly payments once those begin.

Lenders charge an additional fee to make up for the interest that they won’t be receiving in those early years. A homebuyer or seller can pay for a buydown. That payment may be in the form of mortgage points, or a lump sum deposited in an escrow account with the lender and used to subsidize the borrower’s reduced monthly payments.

The 2-1 buydown is sometimes offered as an incentive and sometimes it is part of the buyer’s negotiations.

Example

Suppose a new home builder is offering a 2-1 buydown on its new homes. If the prevailing interest rate on 30-year mortgages is 6% for a particular buyer, this homebuyer could get a mortgage that charged just 4% in the first year, then 5% in the second year, and 6% starting in year three and continuing through the remaining years. The reduced payments in those first two years can result in substantial savings.