Homebuyers will soon have an added layer of protection when shopping around for a mortgage due to the new Homebuyers Privacy Protection Act. The new law is designed to prohibit the abuse of what’s known as trigger leads, which are when credit bureaus sell a borrower’s information immediately after a mortgage credit inquiry. The law makes it illegal for credit bureaus to do so without consumers’ consent.

“This new law is a major victory for mortgage borrowers that will protect them from the barrage of unwanted calls, texts, and emails they too often received immediately after applying for a mortgage,” said Mortgage Bankers Association President and CEO Bob Broeksmit. “It will create a more efficient, responsible, and respectful homebuying process when it goes into effect on March 5, 2026.”

NEW SALES – Pending (Ratified contracts) – New Written sales, a predictor of future closed sales, were down market wide -1% in September of ’24 versus September of ’23. However, last week 255 properties went under contract market wide, +3% from the same week last year. This is a strong and seasonally appropriate number.

CLOSED SALES – Year To date closed sales were at 13,390 at the end of September 2024. A very small difference from the 13,438 at the same time in 2023.

Third Quarter of 2024 closed sales were at 4,396, which is down 3 percent from 2023 (which had 4,510). As a reference, there were 5018 closed sales in 2022.

There were 1,254 closed sales in September 2024 which is down 11 percent from the 1,411 that we saw in September of 2023. Again, as a reference, there were 1,573 closed sales in September of 2022

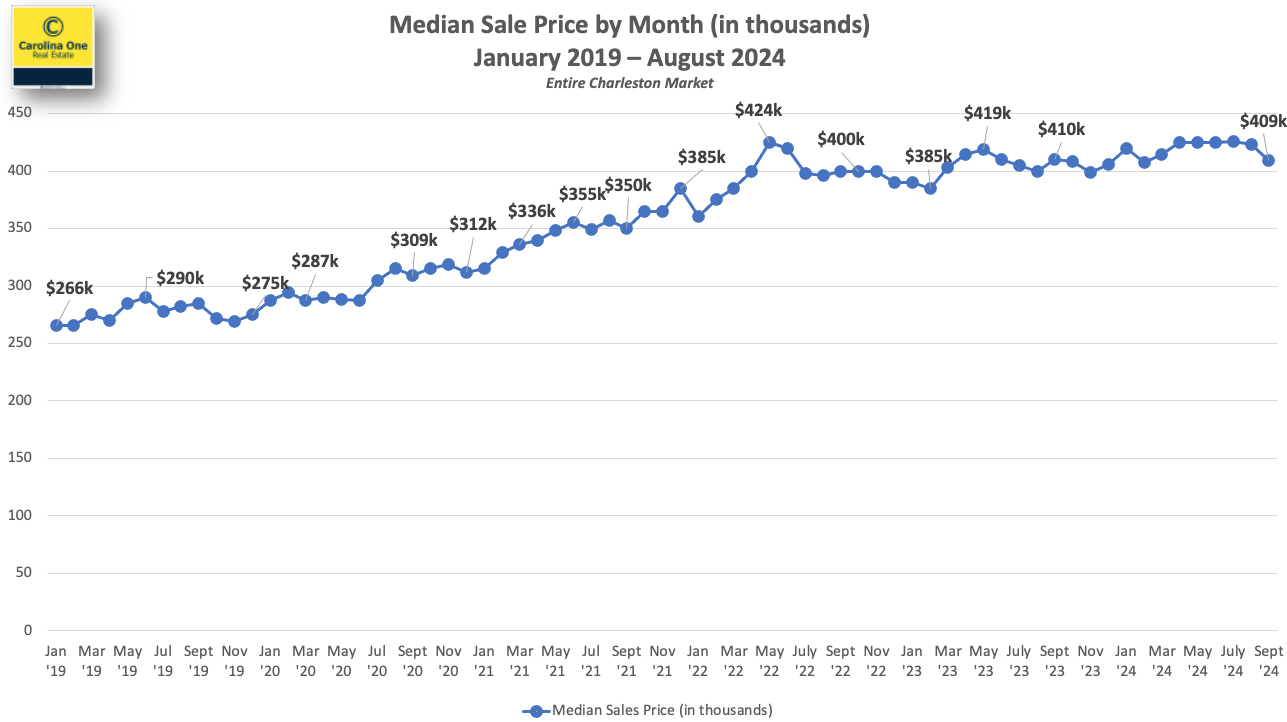

SALES PRICE – The Median sale price closed out at $409,085 in September 2024. The Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 27+ months. The average sales price was $627,254 in September 2024.

AVERAGE SOLD PRICE PER SQFT

The median sales price has remained in a tight band but the average price per sqft remains near an all-time high, well above one year ago. Consumers are getting a smaller house for the money. Essentially, homes are continuing to appreciate despite a stable Median Sale Price.

INVENTORY – Approximately 2,000 new listings came online in September 2024, well ahead of last year’s number. Median Days on market was 26.

Inventory was at approximately 4,200 listings in September 2024. While this level of inventory is a significant increase, the gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is still substantial. See chart below. We need approximately 2,100 additional listings market wide to achieve a balanced market (5 months of inventory)

The Charleston market has about ten weeks of inventory as a whole – this can vary by price range and specific location. The most active areas have inventory levels in the 6-10 week range.

NEW CONSTRUCTION – New construction represents 45% of all pending contracts in the MLS and new construction comprises about 36% of the closings.

If you have questions or would like more information, please don’t hesitate to contact me.

College Park Rd – Berkeley Farms Rd – Goose Creek City Council voted to annex 11 parcels of land totaling 36.25 acres on College Park Road and Berkeley Farms Road. The development plan will include single-family detached dwelling units as well as some multi-family units with 5 acres designated for open space with connected trails and walking paths.

Windsor Mill Road and Goose Greek Boulevard (Hwy 52) – Developers plan to transform this vacant corner into a mixed-use development. SoLiv at Goose Creek plans to encompass 30 acres, with the land assembled from multiple parties organized by a local developer. The preliminary plans consist of 42,000 square feet of commercial and retail space, with 130 active adult residential units and 300 multifamily units.

A Berkeley County property owner can peek through a stand of trees across the road and see part of Cane Bay Plantation. The other side of his land overlooks 1,700 acres of undeveloped land where Seattle-based Weyerhaeuser, the nation’s largest timber tract owner, wants to build another large-scale residential project.

Mr. Burbage Smoak’s property along the heavily traveled, two-lane Black Tom Road stands in the way of any plans Weyerhaeuser might have and Berkeley County Council appears determined to keep it that way.

Smoak’s vacant property includes 421 acres southwest of Moncks Corner, most of it is wetlands. However, He wants to build a strip of commercial buildings on 80 acres that front Black Tom Road — maybe some medical offices or retail space, something that will “support the residents of that area,” according to Kevin Berry, president of Earthsource Engineering, who is representing the landowner.

“We’re not just trying to put more residential rooftops in the area,” he said, adding he’s keenly aware of county council’s desire to slow residential growth so new roads and other critical infrastructure can catch up.

“The public sentiment, and they’ve articulated it well, is there’s frustration when development comes before infrastructure,” said county supervisor Johnny Cribb.

South Carolina is among a handful of Sunbelt states where growth is pulling away from the rest of the country, and one of the region’s top economists says there doesn’t seem to be anything on the horizon to stem the acceleration.

“I don’t see anything in the data that makes me think that growth in the Carolinas, in particular, is going to slow down,” Laura Ullrich, a Charlotte-based economist with the Federal Reserve Bank of Richmond, said during the S.C. International Trade Conference on the Isle of Palms.

The lures that have drawn newcomers from other states — jobs, weather and relatively lower costs — aren’t going to change, Ullrich said. Already, South Carolina ranks as the nation’s fastest-growing state percentagewise, with 1.7 percent growth in 2023, according to census data. That’s nearly 91,000 more people than the previous year, with roughly 19,000 of them moving to the three-county Charleston region.

“And, quite frankly, we still have several mid-sized metros that have a lot of growing to do,” Ullrich said

“If you live in Charleston, things seem super expensive here,” she said. “But it’s a lot cheaper than a house in Fairfax County, Virginia, and a heck of a lot cheaper than San Diego. So, if you look at the areas where that migration is coming from, they are very expensive. Yes, it’s expensive to buy a house in Mount Pleasant. But if you move from San Diego, you might buy a house in Mount Pleasant and another on Lake Murray.”

At the same time, wages are often much lower in South Carolina, and that can amplify the housing crisis regardless of cost comparisons.

“Everybody is worried about housing,” Ullrich said. “The only ways to fix it are, basically, subsidies and density. And people don’t want to talk about density. It’s really hard because everyone wants affordable housing but when density is going up down the road, people complain to their city, and they don’t do it.”

There are a few intangible variables that could crimp growth, such as rising geopolitical tensions or a surprise event that no one can forecast. But Ullrich said the biggest question is how quickly the Fed will lower interest rates going forward.

“Is it going to be an elevator or slow stair steps?” she said.

The answer could go a long way in determining how the housing crisis — both affordability and availability — shakes out in the Charleston region and throughout the Sunbelt.

Nexton, recently announced the addition of Stanley Martin Homes, to the community’s builder program. With plans to develop a collection of townhomes and condos, this project is one of several Stanley Martin developments launching in the Charleston area.

Nexton ranks among the best-selling communities in the nation and boasts a variety of neighborhoods that feature local and national builders and include a diverse array of homes.

Nexton has established itself as a live-work-play destination that features dining, shopping, services and hospitality. Nexton has delivered over 500,000 square feet of office space and offers conveniences such as sought-after schools, grocery stores, modern infrastructure, 20 miles of trails and 2,000 acres of green space.

Are you feeling a bit unsure about what’s really happening with mortgage rates? That might be because you’ve heard they’re coming down. But then you read somewhere else that they’re up again. And that may leave you scratching your head and wondering what’s true.

The simplest answer is: that what you read or hear will vary based on the time frame they’re looking at. Here’s some information that can help clear up the confusion.

Mortgage Rates Are Volatile by Nature

Mortgage rates don’t move in a straight line. There are too many factors at play for that to happen. Instead, rates bounce around because they’re impacted by things like economic conditions, decisions from the Federal Reserve, and so much more. That means they might be up one day and down the next depending on what’s going on in the economy and the world as a whole.

Take a look at the graph below. It uses data from Mortgage News Daily to show the ebbs and flows in the 30-year fixed mortgage rate since last October:

If you look at the graph, you’ll see a lot of peaks and valleys – some bigger than others. And when you use data like this to explain what’s happening, the story can be different based on which two points in the graph you’re comparing.

For example, if you’re only looking at the beginning of this month through now, you may think mortgage rates are on the way back up. But, if you look at the latest data point and compare it to the peak in October, rates have trended down. So, what’s the right way to look at it?

The Big Picture

Mortgage rates are always going to bounce around. It’s just how they work. So, you shouldn’t focus too much on the small, daily changes. Instead, to really understand the overall trend, zoom out and look at the big picture.

When you look at the highest point (October) compared to where rates are now, you can see they’ve come down compared to last year. And if you’re looking to buy a home, this is big news. Don’t let the little blips distract you. The experts agree, overall, that the larger downward trend could continue this year.

Despite the ups and downs, many analysists predict mortgage rates will, over-all, move in a slow declining path as the year progresses, but many factors can influence the trajectory and so only time will tell.

if you’re looking to buy a home, you’ve probably been paying close attention to mortgage rates. Over the last couple of years, they hit record lows, rose dramatically, and are now dropping back down a bit. Ever wonder why?

The answer is complicated because there’s a lot that can influence mortgage rates. Here are just a few of the most impactful factors at play.

Inflation and the Federal Reserve

The Federal Reserve (Fed) doesn’t directly determine mortgage rates. But the Fed does move the Federal Funds Rate up or down in response to what’s happening with inflation, the economy, employment rates, and more. As that happens, mortgage rates tend to respond. Business Insider explains:

“The Federal Reserve slows inflation by raising the federal funds rate, which can indirectly impact mortgages. High inflation and investor expectations of more Fed rate hikes can push mortgage rates up. If investors believe the Fed may cut rates and inflation is decelerating, mortgage rates will typically trend down.”

Over the last couple of years, the Fed raised the Federal Fund Rate to try to fight inflation and, as that happened, mortgage rates jumped up, too. Fortunately, the expert outlook for inflation and mortgage rates is that both should become more favorable over the course of the year. As Danielle Hale, Chief Economist at Realtor.com, says:

“[Mortgage rates will continue to ease in 2024 as inflation improves . . .”

There’s even talk the Fed may actually cut the Fed Funds Rate this year because inflation is cooling, even though it’s not yet back to their ideal target.

The 10-Year Treasury Yield

Additionally, mortgage companies look at the 10-Year Treasury Yield to decide how much interest to charge on home loans. If the yield goes up, mortgage rates usually go up, too. The opposite is also true. According to Investopedia:

“One frequently used government bond benchmark to which mortgage lenders often peg their interest rates is the 10-year Treasury bond yield.”

Historically, the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate has been fairly consistent, but that’s not the case recently. That means, there’s room for mortgage rates to come down. So, keeping an eye on which way the treasury yield is trending can give experts an idea of where mortgage rates may head next.

Bottom Line

With the Fed meets, experts in the industry will be keeping a close watch to see what they decide and what impact it’ll have on the economy.

The Federal Reserve held interest rates steady on Wednesday but signaled that rates could fall in the coming months if inflation continues to cool.

He cautioned, however, that the economy remains unpredictable and said the central bank would proceed cautiously. ”The economic outlook is uncertain and we remain highly attentive to inflation risks,” Powell said.

The Fed has been pleasantly surprised by the rapid drop in inflation in recent months. Core prices in December — which exclude food and energy prices — were up just 2.9% from a year ago, according to the Fed’s preferred inflation yardstick. That’s a smaller increase than the 3.2% core inflation rate that Fed officials had projected in December.

If that positive trend continues, the Fed may be able to start cutting interest rates as early as this spring. However, he sounded doubtful about a rate cut at the Fed’s next meeting in March as many investors in Wall Street had hoped for. The comments disappointed investors, with the Dow Jones Industrial Average tumbling 317 points.

Investors are still hopeful about a rate cut in May, with markets putting the likelihood of that at better than 90%.

Home prices in the 20 biggest U.S. metros rose for the sixth month in a row, as the housing market continues to deal with a shortage of homes for sale.

The S&P CoreLogic Case-Shiller 20-city house price index rose 1% in August, as compared with the previous month.

On a year-over-year basis, home prices in the 20 major metro markets in the U.S. were up 2.2% nationally.

A broader measure of home prices, the national index, rose on a month-over-month basis in August by 0.9%, but rose 2.6% over the past year. All numbers are seasonally adjusted.

Key details: Chicago posted the strongest year-over-year home-price gains in the month of August, at 5%. It was the fourth month in a row that the city led the rankings.

New York and Detroit followed, up 4.98% and 4.8% respectively.

The West continued to lag behind the rest of the country: Home prices fell in Las Vegas and Phoenix the most.

Cities

Change from last year

Atlanta

3.4%

Boston

3.1%

Charlotte

3%

Chicago

5%

Cleveland

3.9%

Dallas

-1.7%

Denver

-0.6%

Detroit

4.8%

Las Vegas

-4.9%

Los Angeles

3.2%

Miami

3.3%

Minneapolis

1.9%

New York

5%

Phoenix

-3.9%

Portland

-1.5%

San Diego

4.1%

San Francisco

-2.5%

Seattle

-1.5%

Tampa

0%

Washington

3.4%

Composite-20

2.2%

A separate report from the Federal Housing Finance Agency also showed home prices rose in August, up 0.6% from July.

And over the last year, the FHFA index was up 5.6%.

Home prices were the strongest in the Middle Atlantic region, according to the government’s data.

Big picture: With homeowners not keen on selling their homes, the U.S. housing market will continue to face a shortage of homes for sale, and by extension, see home prices rise. Interested buyers continue to converge on limited inventory.

Until supply catches up, barring any major events, we’re not likely to see a big movement in home prices.

What S&P said: “On a year-to-date basis, the National Composite has risen 5.8%, which is well above the median full calendar year increase in more than 35 years of data,” said Craig J. Lazzara, managing director at S&P DJI.

“The year’s increase in mortgage rates has surely suppressed housing demand, but after years of very low rates, it seems to have suppressed supply even more,” he added.

“Unless higher rates or other events lead to general economic weakness, the breadth and strength of this month’s report are consistent with an optimistic view of future results,” Lazzara said.

What are they saying? “Another large gain in house prices in August suggests that the extremely limited supply of existing homes for sale continued to outweigh high mortgage rates,” Thomas Ryan, property economist at Capital Economics, wrote in a note.

“We think monthly gains in house prices will soften over the remainder of the year in response to the rise in mortgage rates to just under 8.0%. But an extreme lack of inventory in the existing homes market means we don’t anticipate any further house price falls,” he added.

Market reaction: Stocks were up in early trading on Tuesday. The yield on the 10-year Treasury note fell below 4.9%.