The Federal Reserve held interest rates steady on Wednesday but signaled that rates could fall in the coming months if inflation continues to cool.

He cautioned, however, that the economy remains unpredictable and said the central bank would proceed cautiously. ”The economic outlook is uncertain and we remain highly attentive to inflation risks,” Powell said.

The Fed has been pleasantly surprised by the rapid drop in inflation in recent months. Core prices in December — which exclude food and energy prices — were up just 2.9% from a year ago, according to the Fed’s preferred inflation yardstick. That’s a smaller increase than the 3.2% core inflation rate that Fed officials had projected in December.

If that positive trend continues, the Fed may be able to start cutting interest rates as early as this spring. However, he sounded doubtful about a rate cut at the Fed’s next meeting in March as many investors in Wall Street had hoped for. The comments disappointed investors, with the Dow Jones Industrial Average tumbling 317 points.

Investors are still hopeful about a rate cut in May, with markets putting the likelihood of that at better than 90%.

Tax credit: These are dollar-for-dollar reductions on your tax bill. When you claim a tax credit, the amount you owe goes down the exact same dollar amount.

Tax incentive: These encourage taxpayers to do something, like install efficient appliances, in exchange for a tax reduction.

Tax refund: You’re probably familiar with this one already. You’ll get a refund if you pay more in taxes — say, through your paycheck withholdings — than you actually owe.

Tax rebate: These are retroactive tax decreases. Unlike refunds, they can come at any time of year. Rebates are often offered to stimulate the economy, because people tend to spend them immediately.

Tax break: A general term referring to various tax benefits. These could be credits, deductions, exemptions and others.

Tax benefit: Similar to a tax break, these lower your tax liability.

Home improvement tax deduction: Qualifying improvements to your home that qualify for tax deductions.

Most home improvements, like putting on a new roof or performing routine maintenance, don’t qualify for any immediate tax breaks. However, some (known as capital improvements) may raise the value of your home. In that case, you may see a benefit when you sell.

For immediate benefits, check out these incentives that will reduce your 2023 taxes:

Energy efficiency tax credits

Reducing energy consumption saves money and natural resources. The IRA includes multiple clean energy tax credits to help you do both.

Heat pumps: Your air conditioning and furnace are two of the biggest energy users in your home. Switching to an energy efficient heat pump can net you a 30% credit, up to $2,000.

Windows and doors: Replacing leaky doors and windows brings a 30% credit on the cost, up from 10% last year. Credits are capped at $600 for windows and $500 for two doors.

Electrical upgrades: If you need to update your electrical panel to handle new appliances, the government will pay 30%, up to $600.

Home energy audit: To get the most out of these tax incentives, start with a home energy audit. A credit of up to $150 offsets the cost.

Don’t stop there. “[I]incentives on items like solar, energy storage, EVs [electric vehicles] and more are incredibly generous,” says Greg Fasullo, CEO of Elevation, a residential clean technology company.

Installing solar panels gets you a 30% credit. Depending on the size of the project, Fasullo predicts you could save $6,000, based on the average rooftop solar installation cost of $20,000.

Home office tax deduction

Working from home since the pandemic? Fifty-eight percent of American workers are, too, at least part of the time.

If you use a portion of your home exclusively for business purposes, “you may be able to deduct a portion of your mortgage interest, property taxes, and other expenses related to that space,” says Seth Diener, a private wealth manager at Diener Money Management.

The Internal Revenue Service (IRS) has specific rules about what qualifies as a home office, though. If you’re doing Zoom calls from the kitchen table where you eat dinner every night, that doesn’t count. You must have a separate room or area that’s only used for your home office. If that’s you, you can calculate this deduction two ways:

Regular method: Figure out the percentage of your home you use for work. The deduction you can claim is based on this number, and whether your expenses are direct or indirect.

Simplified method: Calculate the square footage of your home office and multiply it by $5 per sq. ft., up to 300 sq. ft., with a maximum deduction of $1,500.

Medical improvements

“If you have medical upgrades that are prescribed by a doctor, such as wheelchair ramps or other accessibility features, these may be deductible as medical expenses,” says Andrew Latham, a certified financial planner and director of content at SuperMoney.com.

The IRS website offers a non-exhaustive list of qualifying capital expenses, including widening doorways, moving electrical devices, adding handrails and grading the exterior.

Note: If the medical home improvement raises the value of your home, the deduction will be based on the difference between the cost of the improvement and the increase in property value.

Rental property investments

Improvements to rental properties fall under a deduction called depreciation.

“Improvements to a rental property are usually considered deductible business expenses,” Latham says. “However, these incentives are subject to specific rules and limits, so it’s advisable to check current tax laws or consult with a tax professional.”

Federal vs. State Home Improvement Tax Incentives

What if you put in that heat pump and got back $2,000 from the federal government? Could you also claim the credit on your state return?

“Yes, in some instances, you can qualify for multiple tax breaks for the same project,” Latham says. “[I]f you install a new energy-efficient heat pump, you might be eligible for a federal tax credit, a state-level incentive, and potentially a rebate from your local utility company.”

Always check with a tax professional for advice as rules and laws change.

Home prices in the 20 biggest U.S. metros rose for the sixth month in a row, as the housing market continues to deal with a shortage of homes for sale.

The S&P CoreLogic Case-Shiller 20-city house price index rose 1% in August, as compared with the previous month.

On a year-over-year basis, home prices in the 20 major metro markets in the U.S. were up 2.2% nationally.

A broader measure of home prices, the national index, rose on a month-over-month basis in August by 0.9%, but rose 2.6% over the past year. All numbers are seasonally adjusted.

Key details: Chicago posted the strongest year-over-year home-price gains in the month of August, at 5%. It was the fourth month in a row that the city led the rankings.

New York and Detroit followed, up 4.98% and 4.8% respectively.

The West continued to lag behind the rest of the country: Home prices fell in Las Vegas and Phoenix the most.

Cities

Change from last year

Atlanta

3.4%

Boston

3.1%

Charlotte

3%

Chicago

5%

Cleveland

3.9%

Dallas

-1.7%

Denver

-0.6%

Detroit

4.8%

Las Vegas

-4.9%

Los Angeles

3.2%

Miami

3.3%

Minneapolis

1.9%

New York

5%

Phoenix

-3.9%

Portland

-1.5%

San Diego

4.1%

San Francisco

-2.5%

Seattle

-1.5%

Tampa

0%

Washington

3.4%

Composite-20

2.2%

A separate report from the Federal Housing Finance Agency also showed home prices rose in August, up 0.6% from July.

And over the last year, the FHFA index was up 5.6%.

Home prices were the strongest in the Middle Atlantic region, according to the government’s data.

Big picture: With homeowners not keen on selling their homes, the U.S. housing market will continue to face a shortage of homes for sale, and by extension, see home prices rise. Interested buyers continue to converge on limited inventory.

Until supply catches up, barring any major events, we’re not likely to see a big movement in home prices.

What S&P said: “On a year-to-date basis, the National Composite has risen 5.8%, which is well above the median full calendar year increase in more than 35 years of data,” said Craig J. Lazzara, managing director at S&P DJI.

“The year’s increase in mortgage rates has surely suppressed housing demand, but after years of very low rates, it seems to have suppressed supply even more,” he added.

“Unless higher rates or other events lead to general economic weakness, the breadth and strength of this month’s report are consistent with an optimistic view of future results,” Lazzara said.

What are they saying? “Another large gain in house prices in August suggests that the extremely limited supply of existing homes for sale continued to outweigh high mortgage rates,” Thomas Ryan, property economist at Capital Economics, wrote in a note.

“We think monthly gains in house prices will soften over the remainder of the year in response to the rise in mortgage rates to just under 8.0%. But an extreme lack of inventory in the existing homes market means we don’t anticipate any further house price falls,” he added.

Market reaction: Stocks were up in early trading on Tuesday. The yield on the 10-year Treasury note fell below 4.9%.

Tucked away in The Hamlets of Crowfield Plantation, is a rare property that offers privacy and tranquility in a desirable community with easy access to all that the Low Country has to offer!

This Luxury property has a private security gate, 7795 sqft, 7 Bedrooms, 8 Bathrooms, A State-Of-The Art Movie Theatre, A 6 Car Garage, A Separate Apartment, One Acre Lot, Golf Course and Pond Views, and so much more!

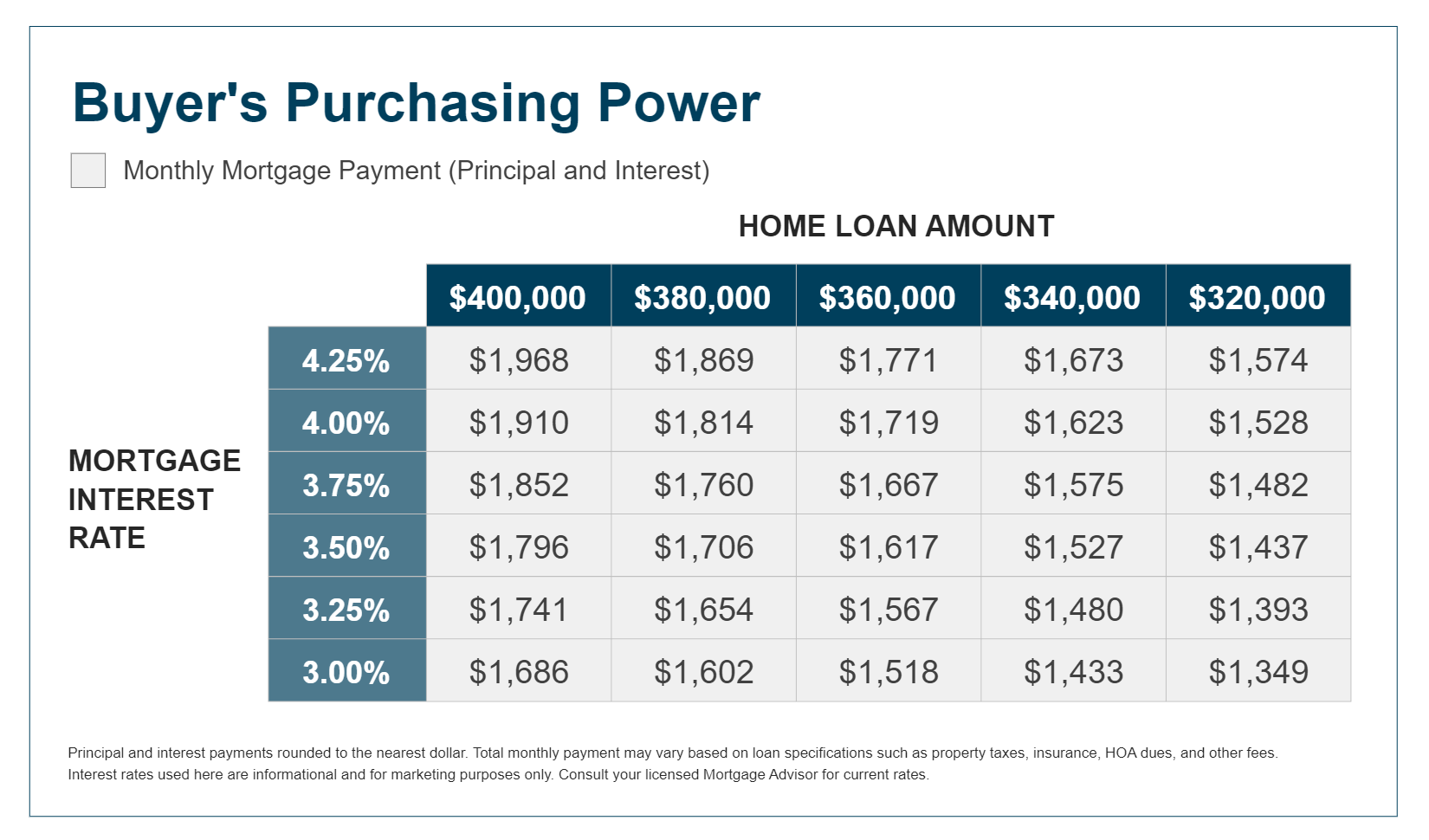

This chart shows how 1.25 % increase in rate could affect monthly principal and interest payment. For Example; the P&I payment on $400,000 at a rate of 3% is $1,686 per month but that same price calculated with a 4.25 % rate is $1,968 per month. A difference of $282 per month.

If you’re thinking about selling your house in 2022, you truly have a once-in-a-lifetime opportunity at your fingertips.

When selling anything, you always hope for strong demand for the item coupled with a limited supply. That maximizes your leverage when you’re negotiating the sale. Home sellers are in that exact situation right now. Here’s why.

Demand Is Very Strong

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), 6.18 million homes were sold in 2021. This was the largest number of home sales in 15 years. Lawrence Yun, Chief Economist for NAR, explains:

“Sales for the entire year finished strong, reaching the highest annual level since 2006. . . . With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases.”

Demand isn’t expected to weaken this year, either. In addition, the Mortgage Finance Forecast, published last week by the Mortgage Bankers’ Association (MBA), calls for existing-home sales to reach 6.4 million homes this year.

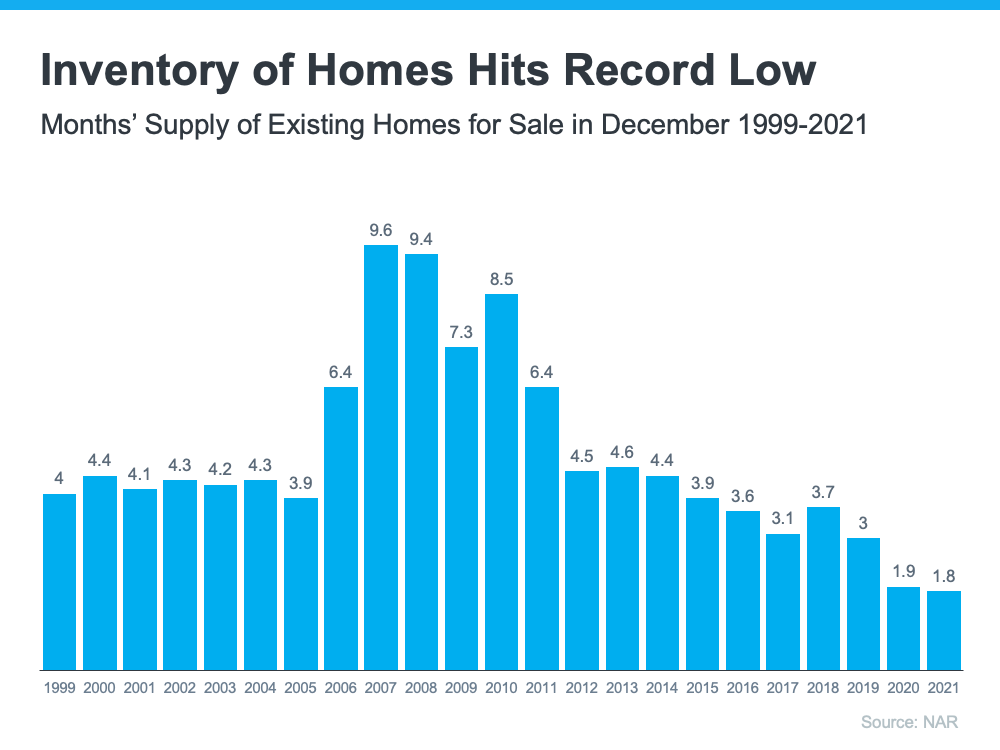

Supply Is Very Limited

The same sales report from NAR also reveals the months’ supply of inventory just hit the lowest number of the century. It notes:

“Total housing inventory at the end of December amounted to 910,000 units, down 18% from November and down 14.2% from one year ago (1.06 million). Unsold inventory sits at a 1.8-month supply at the present sales pace, down from 2.1 months in November and from 1.9 months in December 2020.”

The reality is, inventory decreases every year in December. That’s just how the typical seasonal trend goes in real estate. However, the following graph emphasizes how this December was lower than any other December going all the way back to 1999.

Right Now, Sellers Have Maximum Leverage

As mentioned above, when there’s strong demand for an item and a limited supply of it available, the seller has maximum leverage in the negotiation. In the case of homeowners who are thinking about selling, there may never be a better time than right now. While demand is this high and inventory is this low, you’ll have leverage in all aspects of the sale of your house.

Today’s buyers know they need to be flexible negotiators that make very competitive offers, so here are a few areas that could tip in your favor when your house goes on the market:

Competitive sales price

Flexible closing date

Potential for a leaseback to allow you more time to find a home

Minimal offer contingencies

Bottom Line

If you’re thinking of selling your house this year, now is the optimal time to list it. Let’s connect to discuss how you can put your house on the market today.

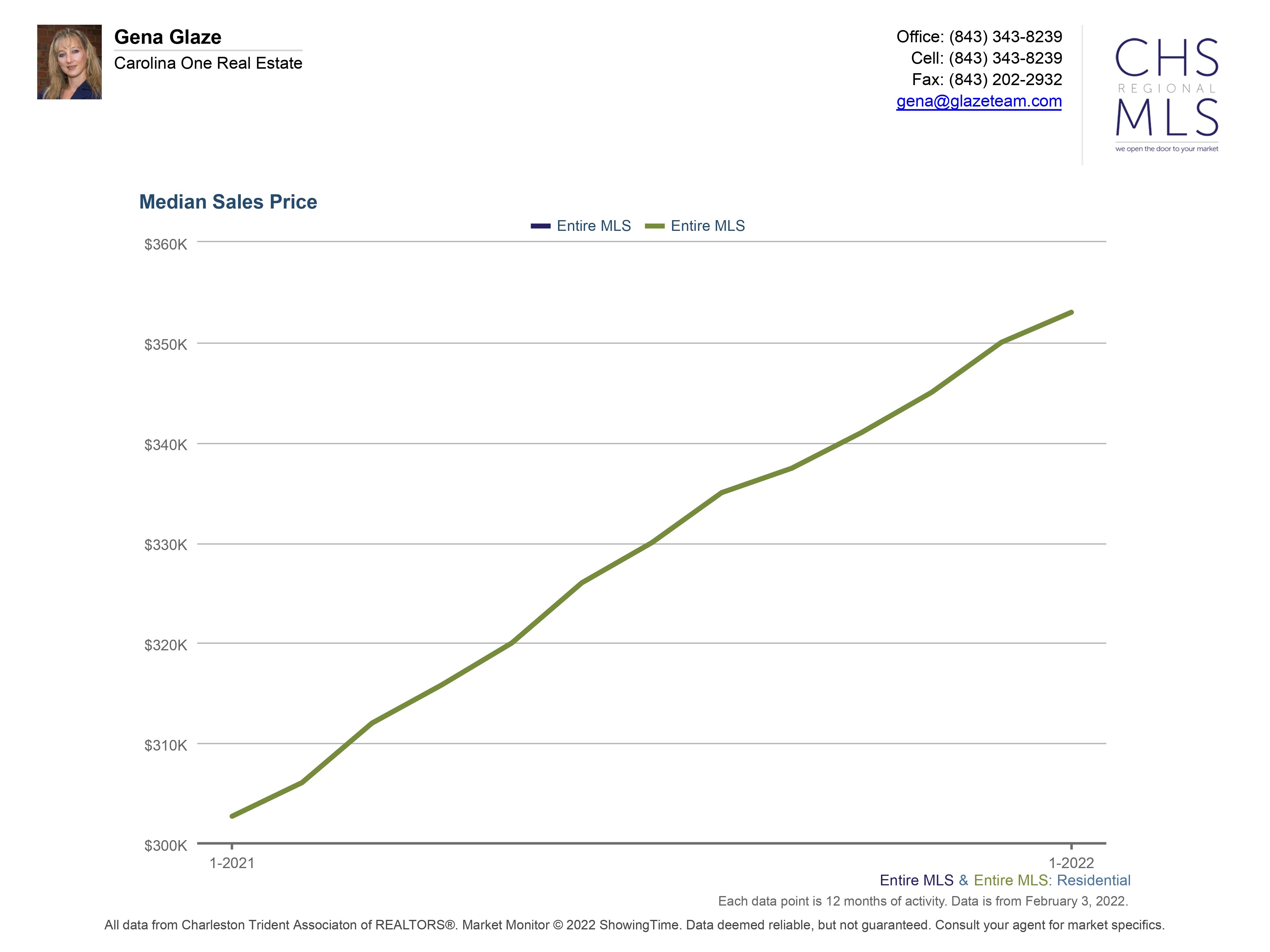

Prices grew 16.6% in 12 months according to the stats recorded by our Local MLS, Charleston-Trident Association of Realtors. In January of 2021. The median sales price was documented at just under $305,000 and by January of 2022 the median sales price was $353,000, up 16.6%.

Many members of Generation Z (Gen Z) are aging into adulthood and deciding whether to rent or buy a home. If you find yourself in this group, it’s important to understand you’re never too young to start thinking about homeownership. The sooner you start planning, the sooner you can move on from renting.

As you set off on your journey and plan your next move, here are a few reasons to think about homebuying this year.

The Reasons Gen Z Want To Become Homeowners

While the majority of Gen Z haven’t entered the housing market yet, a large portion plan to according to a realtor.comreport. The report found that 72% of Gen Z would rather purchase a home than rent long-term. As George Ratiu, Manager of Economic Research for realtor.com,says:

“With nearly three-quarters of those surveyed preferring to buy versus renting long-term, the housing industry should be prepared for millions of Gen Z buyers to bring a new wave of demand along a similar stage-of-life timeline as the millennial generation before them.”

But why do so many members of Gen Z value homeownership? According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), young homebuyers – more than any other age group – want to become homeowners because they want to have a place of their very own.

That may be because one of the biggest benefits of homeownership is having a place that you can truly make your own by customizing it to your style and personality. Whether that’s the décor, painting, or renovations, when you own your home, you don’t have to limit yourself to what your lease and landlord will allow.

Not to mention, owning a home provides much greater long-term stability and security than renting. When you own a home, there’s also protection from steadily rising rental costs because your monthly mortgage payment is locked in for the length of your loan (typically 15 to 30 years).

Work with a Real Estate Professional To Achieve Your Goals

Whether you’re just getting started on your homebuying journey, you want to learn more about the process, or you’re fully committed to buying your first home this year, it’s especially important to connect with a trusted real estate advisor soon, as you won’t be the only first-time buyer in the market. According to a recent survey from realtor.com, a majority of first-time buyers surveyed are looking to purchase a home in 2022. As the survey notes:

“First-time home buyers retain their optimism despite a challenging housing market in the past year. Hoping to achieve their goal of homeownership and provide a comfortable space for their families, young buyers are setting out to learn what they can about the market and setting their list of priorities for their home purchase.”

That means you’ll likely face strong competition from other first-time buyers. One way to get a leg-up on that competition is to work with a real estate professional to make sure you have the support you need to make an informed and confident decision.

Bottom Line

If you’re planning your next move, you’re not alone. Just know it’s never too early to consider the benefits of homeownership over renting. To learn more, contact me!

If you’re thinking about selling your house in 2022, you truly have a once-in-a-lifetime opportunity at your fingertips. When selling anything, you always hope for strong demand for the item coupled with a limited supply. That maximizes your leverage when you’re negotiating the sale. Home sellers are in that exact situation right now. Here’s why.

Demand Is Very Strong

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), 6.18 million homes were sold in 2021. This was the largest number of home sales in 15 years. Lawrence Yun, Chief Economist for NAR, explains:

“Sales for the entire year finished strong, reaching the highest annual level since 2006. . . . With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases.”

Demand isn’t expected to weaken this year, either. In addition, the Mortgage Finance Forecast, published last week by the Mortgage Bankers’ Association (MBA), calls for existing-home sales to reach 6.4 million homes this year.

Supply Is Very Limited

The same sales report from NAR also reveals the months’ supply of inventory just hit the lowest number of the century. It notes:

“Total housing inventory at the end of December amounted to 910,000 units, down 18% from November and down 14.2% from one year ago (1.06 million). Unsold inventory sits at a 1.8-month supply at the present sales pace, down from 2.1 months in November and from 1.9 months in December 2020.”

The reality is, inventory decreases every year in December. That’s just how the typical seasonal trend goes in real estate. However, the following graph emphasizes how this December was lower than any other December going all the way back to 1999.

Right Now, Sellers Have Maximum Leverage

As mentioned above, when there’s strong demand for an item and a limited supply of it available, the seller has maximum leverage in the negotiation. In the case of homeowners who are thinking about selling, there may never be a better time than right now. While demand is this high and inventory is this low, you’ll have leverage in all aspects of the sale of your house.

Today’s buyers know they need to be flexible negotiators that make very competitive offers, so here are a few areas that could tip in your favor when your house goes on the market:

Competitive sales price

Flexible closing date

Potential for a leaseback to allow you more time to find a home

Minimal offer contingencies

Bottom Line

If you’re thinking of selling your house this year, now is the optimal time to list it. Let’s connect to discuss how you can put your house on the market today.

![Americans Choose Real Estate as the Best Investment [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2022/01/20143424/20220121-NM.png)