An accessory dwelling unit (ADU), sometimes called a carriage house or in-law suite, is a separate, detached living space with a kitchen, bathroom and sleeping area on the same property as a single-family home.

As the cost of housing continues to rise, local leaders are looking to allow these accessory dwelling units in residential areas to provide more housing options.

Leaders in the local government of North Charleston recently proposed a new ordinance that would allow homeowners to rent the separate unit to a long-term tenant, which would provide additional income to the homeowner and increase housing stock.

North Charleston currently allows ADUs in a few overlay districts, such as the Olde North Charleston Historic District and Neighborhood Conservation District, which covers a strip of Park Circle between Spruill and Virginia avenues. The new ordinance is aimed at areas like Park Circle where larger lot sizes can accommodate additional density, as opposed to already dense areas like Liberty Hill, Chicora-Cherokee and Accabee.

According to the proposed ordinance, an ADU cannot be more than two-thirds the size of the principal dwelling unit or exceed 800 square feet. The lot size must be at least 4,500 square feet. An additional off-street parking spot for the ADU must be provided. All ADUs must be permitted by the city.

It’s intentional that these additional units are small, said Tim Macholl, the city’s director of planning and zoning, during a November committee meeting. He said the space is ideal for a college student who is spending the summer at home or in-laws staying in town. It also provides an opportunity for additional income for homeowners if they choose to rent it out, he added. However, these units are not eligible for short-term rental permits, so they can not be used for vacation rental services, like Airbnb.

The demand for ADU’s is on the rise. They offer some affordable housing solutions, an option for multi-generational living and versatility of home space as they can be used as home offices, living spaces or possibly rentals.

Goose Creek also has previsions in their ordinance for ADU’s and many other municipalities are incorporating guidelines as well to accommodate the ADU trend.

If you are considering an ADU, check with your local municipality and Homeowner Association to make sure they are allowed and to obtain the guidelines, rules and permitting requirements.

Year over Year Review (2023 vs. 2024): Closed sales up 13.7% Median Sales price up 2.3 %

December 2024 stats for the entire Charleston MLS:

NEW SALES – Pending – There were 1106 new written sales in December 2024, a. predictor of future closed sales, which was up 6.3% versus December of 2023. YTD was up 2.4%.

CLOSED SALES – There were 1382 closed sales in December of 2024, up 13.7% from December of 2023 and up a negligible 1.1% YTD, compared to 2024.

SALES PRICE – The Median sales price closed out at $414,296, up 2.30% over December of 2024 and The Year-to-date median sales price was up 4.1% over 2024. The average sales price for December 2024 was $612,457.

INVENTORY – Approximately 1165 new listings came online in December 2024, which is down -6.9% from December 2023 but up YTD 10.8% The market as a whole had approximately 2.6 months of inventory at December’s end with the average Days on Market at 50, up 25% from December of 2023 and up 14% year to date.

Finalized on January 7, a new rule from the Consumer Financial Protection Bureau (CFPB) prohibits credit reporting agencies from including medical debt information in the credit reports and scores they provide to lenders. It’s expected to impact nearly 15 million Americans who have previously been haunted by an estimated $49 billion in medical bills on their credit reports.

The new rule will go into effect 60 days after publication in the Federal Register. It typically takes about three business days for a new document to be added into the Federal Register, which effectively serves as official notice of the rule. So, don’t expect your credit score to improve overnight; it will be several weeks before affected consumers will see the changes.

The credit improvement could help many qualify to buy a home. However, two industry groups filed lawsuits seeking to block the rule

The National Association of Realtor’s economists recently weighed in on home sales, mortgage rates, the economy and changing buyer demographics and its effect on real estate for the year ahead.

Lawrence Yun, chief economist of the National Association of REALTORS®, along with NAR’s Deputy Chief Economist, Jessica Lautz, shared data and forecasts..

Their updated estimates show that the housing market is still dramatically undersupplied, and they estimate that U.S. housing stock is 3.7 million units below what is needed.

High mortgage rates and rising home prices have put a damper on affordability and are directly related to the supply shortage. Building more houses is essential but builders are also contending with high interest rates.

There is no silver bullet to alleviating this ongoing shortage but there are options being considered such as, accessory dwelling units (ADUs), Community Land Trusts, condominium conversions, and manufactured homes. They will continue to study this topic and work to uncover potential solutions.

Yun released a rosier forecast for the housing market for 2025 and 2026, with an outlook for higher home sales and moderating mortgage rates.

Here’s an overview of NAR’s predictions on key housing indicators for the year ahead.

Home Sales to Rise

With improving job numbers and recent gains in the stock market, more Americans may be motivated to act, Yun said.

Here’s Yun’s forecast over the next two years:

2025 sales projection: Existing home sales to rise 9% year-over-year; New home sales to jump by 11%.

2026 sales projection: Existing-home sales to rise 13% year-over-year; new home sales to increase by 8%.

Mortgage Rates to Moderate

The trajectory of mortgage rates will have a major bearing on how the housing market will fare, Yun said.

Mortgage rates may moderate but buyers may not see that anytime soon, Yun said. “Mortgage rates will not decline in tandem”… “With a large budget deficit, there’s less mortgage money available…. A large budget deficit will prevent mortgage rates from going down to 4%”

Nevertheless, the “locked-in” effect of homeowners feeling stuck-in-place with low 2% or 3% mortgage rates from recent years will lessen over time, as personal milestones (births, deaths, marriages, graduations, new jobs,etc.) trigger real estate moves.

Home Prices Increases Slowly After Rapid Rises

While homeowners have enjoyed record-breaking equity gains, home buyers’ have been struggling with affordability. A typical homeowner has accumulated $147,000 in housing wealth just over the last five years, according to NAR’s research. As a result, the spread in median net worth between homeowners and renters continues to grow. It stands at $415,000 for homeowners versus $10,000 for renters, Yun said.

“The strong price increases cannot be sustainable for another five years, or America will be divided … with only a few getting to experience the tremendous housing wealth,” Yun said. “If we bring more supply to the housing market, home price increases will not be as outrageous … and will be more in line with wages.”

Yun’s forecast:

2025 median home price: $410,700; up 2% over 2024.

2026 median home price: $420,000, up 2% over 2025.

A Different Type of Buyer Emerges

The profile of home buyers are changing, Lautz said, presenting data from NAR’s newly released 2024 Profile of Home Buyers and Sellers. Here’s a few of the changes observed in the report:

More buyers are skipping the mortgage. all-cash buyers have surged to record highs, accounting for 26% of home sales over the past year. Thirty-one percent of repeat buyers paid all-cash for their next home purchase.

First-time buyers are getting older. The median age of a first-time home buyer was 38, an all-time high. Twenty-five percent of first-time buyers used a gift or loan from a relative or friend for their home purchase; 20% took money out of financial assets like stocks, 401ks or cryptocurrency to afford homeownership; and 7% used inheritance money for their purchase—a record high, Lautz noted. First-time buyers are coming up with the highest down payments in nearly 30 years—at 9%—in order to afford the higher home prices.

The allure of cities grows. The pandemic may have unleashed a trend of suburban movers, but people are now heading back to city centers—the largest uptick in a decade, Lautz said.

More buyers are pooling their money. The number of multigenerational households surged to an all-time high of 17% over the past year. “The number one reason is for cost savings,” Lautz said. “They’re combining incomes” in order to afford homeownership. They’re also buying a multigenerational home to take care of aging parents or because of young adults are moving back home, Lautz noted.

Single women buyers continue to outpace single men buyers. A drop in marriage rates has triggered more consumers to enter the housing market on their own. Single women held a 24% share of the home-purchase market over the past year. For single men, it was 11%.

NEW SALES – Pending (Ratified contracts) – There were 1,266 new written sales in November 2024, a. predictor of future closed sales, which was up 12% versus November of 2023. YTD was up 3.6% at end of November. However, last week saw 167 properties go under contract market wide, down -15% to the same week last year.

CLOSED SALES – There were 1331 closed sales in November of 2024, up 3.9% from November of 2023 and up a negligible 0.1% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $419,000, up 5.4% over November of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for Movember 2024 was $611,213. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 30 months- 2 1/2 years!

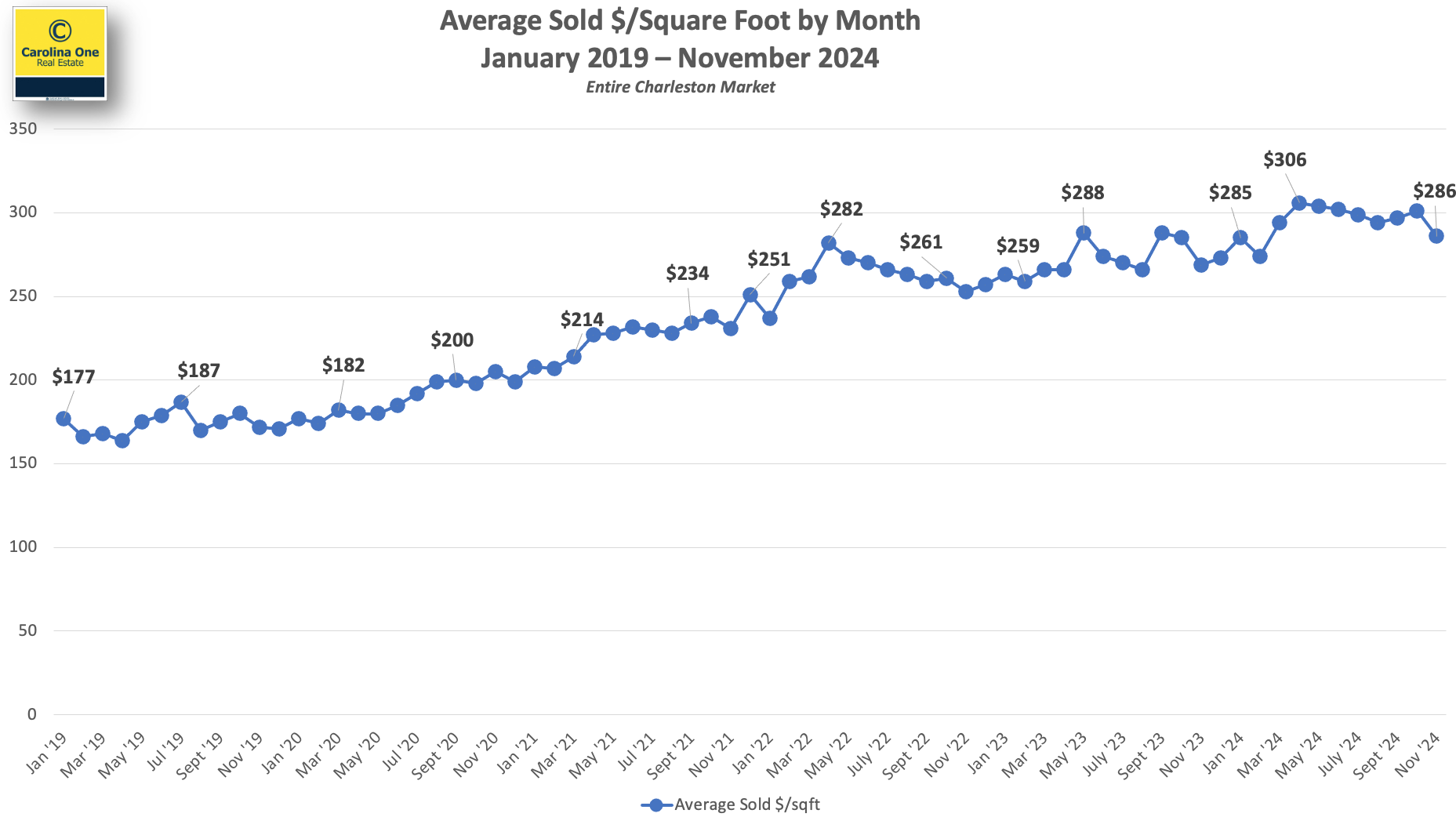

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $286 /sqft

INVENTORY – Approximately 1581 new listings came online in November 2024, which is up 0.6% from November 2023 and up YTD 11.7%

We still need roughly 2,500 additional listings market wide to achieve a balanced market (5 months of inventory)

The market as a whole has approximately 2.6 months of inventory with the Days on Market at 29. See absorption rate by area below:

NEW CONSTRUCTION – New construction represents 49% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – Represent a combined 0.7% of all available listings

If you have questions or have a real estate need, please don’t hesitate to contact me!

NEW SALES – Pending (Ratified contracts) – There were 1,393 new written sales in October 2024, a predictor of future closed sales, which was up 2% versus October of 2023. YTD was down -4%

However, Last week 242 properties went under contract market wide, which was up +16% compared to the same week last year.

CLOSED SALES – FLAT – There were 1,354 closed sales in October of 2024, down a negligible -0.7% from October 2023 and down -0.4% YTD, compared to 2023.

SALES PRICE – The Median sales price closed out at $415,685, up 3% over October of 2023 and The Year-to-date median sales price was up 4.25% over 2023. The average sales price for October 2024 was $644,758. The Median sale price in the Charleston market continues to stay in a tight band between $400k and $425k where it has been for most of the last 27+ months.

AVERAGE SOLD PRICE PER SQFT

The average price per sqft still remains near an all-time high at approximately $301 /sqft

INVENTORY – Approximately 1961 new listings came online in October 2024, which is up 4% from October 2023 and Third quarter Inventory levels were up 12.6% over 2023.

There were approximately 2.7 months of Inventory calculated in October 2024, with the median Days on Market at 25, up 56.2% from October 2023 and the median days on market up 46.7% YTD.

We still need additional listings market wide to achieve a balanced market of 5 months of inventory.

Absorption rate by Area

NEW CONSTRUCTION – New construction represents 48% of all pending contracts in the MLS and new construction comprises approximately 36% of the closings.

FORECLOSURES AND SHORT SALES – have declined even further to a combined 0.7% of all available listings This market continues to be basically nonexistent and there are very few “newly distressed” properties in the pipeline.

MM+ We are roughly double the monthly pre-pandemic sales levels of over Million dollar plus properties. This market segment remains robust.

If you have questions or have a real estate need, please don’t hesitate to contact me!

The city of Charleston’s Design Review Board approved guidelines for a proposed overhaul of Citadel Mall into the mixed-use “Epic Center” concept with greenspace, entertainment, retail and housing.

When transformed, the Epic Center project could have more than 4 million square feet of mixed uses, including offices, medical facilities, meeting spaces, residences, restaurants and a world-class sports facility, according to Citadel Mall’s lead investor Richard Davis.

Futuristic plans show large-scale development around the mall with multistory buildings and a mix of uses. The development is projected to begin in 2025.

Many experts expect rates to fall below 6% in 2025, but the forecast is far from guaranteed. In January 2023, some analysts thought that rates would be around 4.5% by the end of 2024, which is obviously not happening.

Fed Chair Jerome Powell says it best: “Forecasting’s are highly uncertain….Forecasting is very difficult.”

Rates will likely continue moderating in 2025 and 2026 but will stay relatively high as long as the economy keeps outpacing expectations, but over-all economists don’t anticipate a dip into the 3% or 4% range in the foreseeable future.

Here are the mortgage rate predictions as reported by US News:

• Fannie Mae: Rates Will Average 5.7% in 2025

The October Housing Forecast from Fannie Mae puts the average 30-year fixed rate at 6% by year-end, a decline from 6.5% in the third quarter. All told, the mortgage giant predicts mortgage rates will average 6.6% in 2024 and 5.7% in 2025.

• MBA: Rates Will Fall to 5.9% in 2025

The Mortgage Bankers Association predicts in its October Mortgage Finance Forecast that mortgage rates will fall from 6.5% in the third quarter of 2024 to 6.3% by the fourth quarter. The industry group expects rates will fall to 5.9% in the third quarter of 2025 and will continue declining to 5.9% in late 2025 and early 2026.

• NAHB: Rates Will Average 5.94% in 2025

The National Association of Home Builders expects the 30-year mortgage rate to average 5.94% in 2025, falling to 5.69% in 2026, according to its October Housing and Interest Rate Forecast. The trade group is forecasting that “sustained, sub-6% mortgage interest rates” will begin in the second quarter of 2025, something it previously forecasted to happen in the fourth quarter.

• Wells Fargo: Rates Will Average 5.86% in 2025

In its latest U.S. Economic Outlook, the Economics Group of Wells Fargo Bank puts the 30-year conventional mortgage rate at 6.3% in the fourth quarter of 2024 – a slight increase from when rates dipped in the third quarter. Wells Fargo economists predict that the average rate will dip below 6% in the second quarter of 2025, which is pushed further out from their previous forecast that expected sub-6% rates in the first quarter.

The Cottages at Ingleside in North Charleston, developed by Alabama-based Capstone Communities, is the newest build-for-rent neighborhood to join the Lowcountry lineup.

As the build-to-rent model gains popularity, Capstone is actively looking for new development prospects in South Carolina beyond its North Charleston, Summerville and Myrtle Beach communities.

The model is especially enticing following the last few years as housing prices increased, mortgage rates remained high, and inventory has been low.

In 2023, the Build to Rent (BTR) category grew to 75,000 units nationally — an 87 percent increase year over year and an all-time high. For-sale new builds declined 6.9 percent for the second year in a row nationally, according to national direct lender Arbor.

“It’s a reaction to housing affordability at a more than decade low because of high mortgage interest rates,” said Robert Dietz, chief economist with the National Association of Home Builders.

A National Association of Realtors analysis noted that developers who specialize in other niches, such as family or senior housing, are also “dipping their toes into BTR to diversify their portfolios, since that segment represents a high-performance asset class offering faster lease-ups and lower turnover than apartments.”

Down the line, developers have several options, Dietz said.

“There’s the one where the builder builds it and then sells it almost immediately to an investor,” he said. “There is a version where the builder holds it and operates it for a few years and sells it. … And then there’s ones where they claim to hold it forever, and it depends a lot on how it’s financed. I think we’ll have to wait and see in about three or four years.”

While there’s a nationwide debate over whether the build-to-rent trend is snatching up key properties that could have been available for buyers, Dietz countered that a home is a home. The model converts an owner into a renter, but still adds to the nation’s much-needed housing stock, Dietz noted.

Carnes Crossroads is a thoughtfully designed master planned community with a variety of home styles. The community features scenic parks, pools, playgrounds, lakes, and biking trails and a community dock.

New features on the horizon are a lake house, pickleball and tennis courts, and resort style pool with a water slide and the addition of an 11-acre farm that will be right in the middle of the neighborhood.

This new “Agrihood,” brings agriculture into the neighborhood, making the farm accessible to residents. The farm will have a staff that will grow all kinds of fruits and vegetables. Once a month, staff will have a farm share program providing each household a share of the harvest.