Agrihood site to include fitness, lake house, water slide and sports courts

A Charleston-area master-planned community where 3,600 homes will be built at completion will break ground in the fall on several new amenities.

Coming to Carnes Crossroads in Goose Creek will be a 10-acre farm with organically grown products, a barn to pick up produce, community house near Lake Hewitt, fitness center, pool with a slide tower, and courts for tennis, pickleball and half-court basketball.

A product of Boston-based Freehold Communities, the development with 700 homes on the ground as of Sept. 15, features more than 9 miles of walking trails, schools and monthly farmers markets with Lowcountry vendors. The 2,300-acre Carnes Crossroads community is approved for about 4,500 homes.

“The central component of the barn within our Amenity Center encourages our vision for a vibrant, healthy and connected lifestyle for our residents,” said Gerrit Albert, Freehold’s division president for South Carolina and Georgia. “The addition of these community spaces will foster a sense of togetherness and engagement that is central to our Agrihood mission.”

(1) Written sales market wide finished 13% less in August of ’23 versus August of ’22.

It was anticipated that sales would be -15% for the year (versus 2022) with the first half of the year being much worse than -15% and the back half of the year being better than -15%

Based on interest rates remaining stubbornly and persistently high, we are now anticipating that the second half of the year will be similar to the first half of the year with sales in the -15% year-over-year range

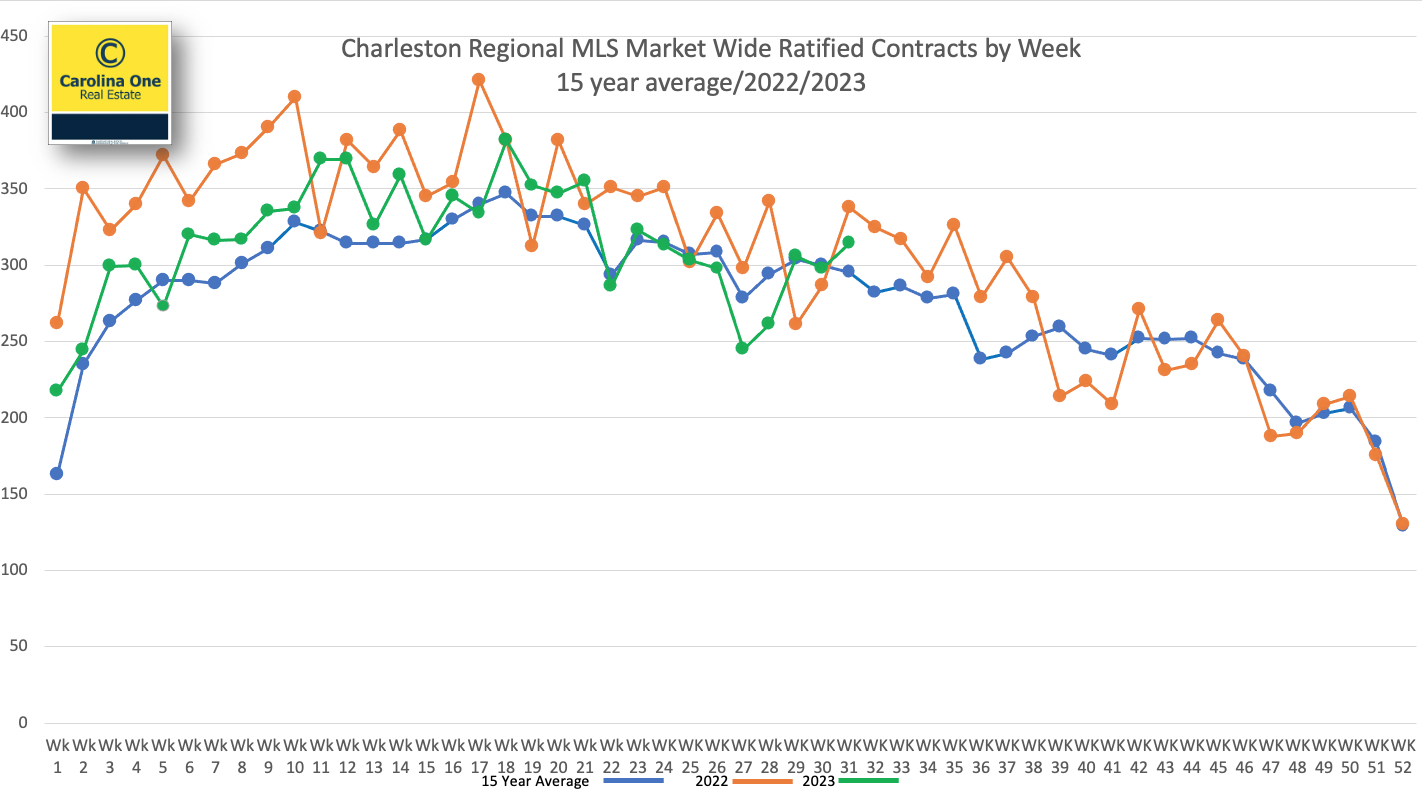

(2) Last week saw 239 properties go under contract, a very “normal” number for this time of year but far below the “juiced up” pandemic years of 2020 and 2021. Sales (green line) have remained remarkably close to the 15 year average (blue line) for about three and a half months.

The orange line represents ratified contracts by week last year…the green line is this year…and the blue line is the 15 year average for each week.

(3) Mortgage rates remaining elevated is holding back sales.

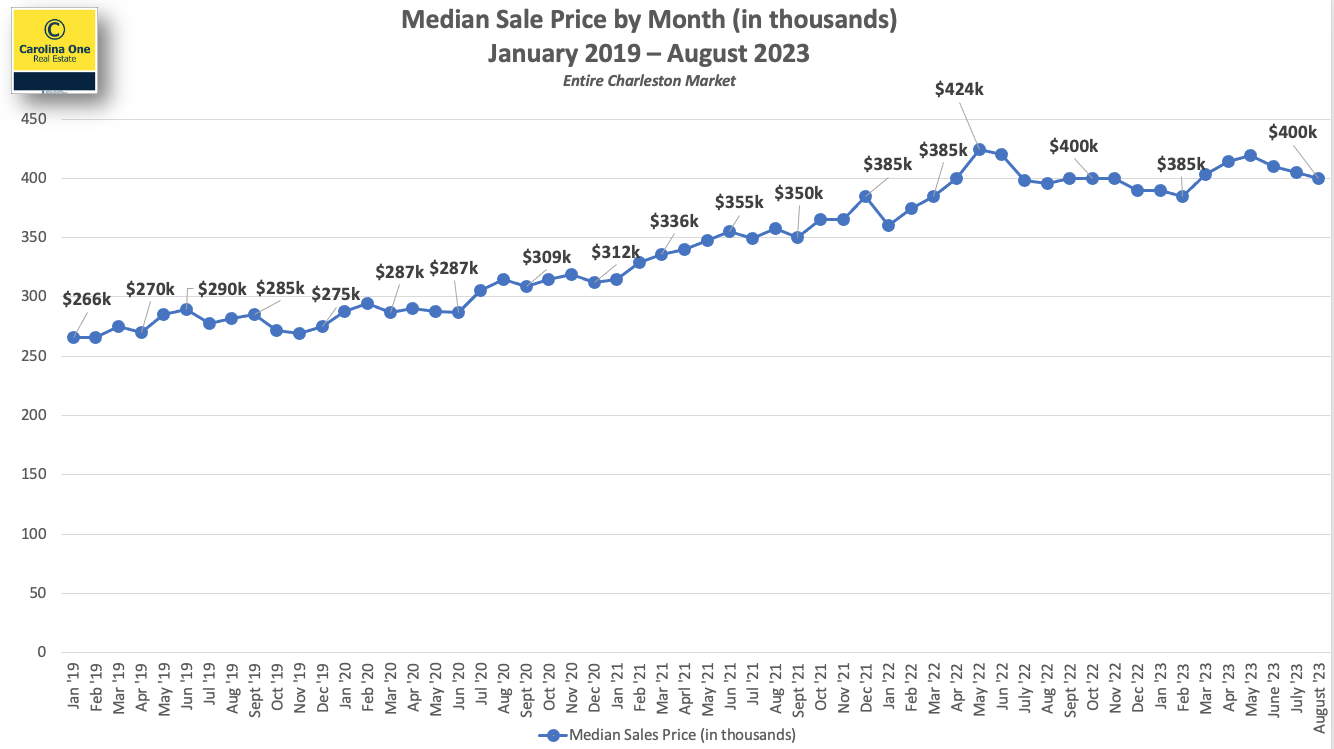

4) The Median sale price in the Charleston market continues to stay in a tight band between $400k and $420k where it has been for most of the last 16 months.

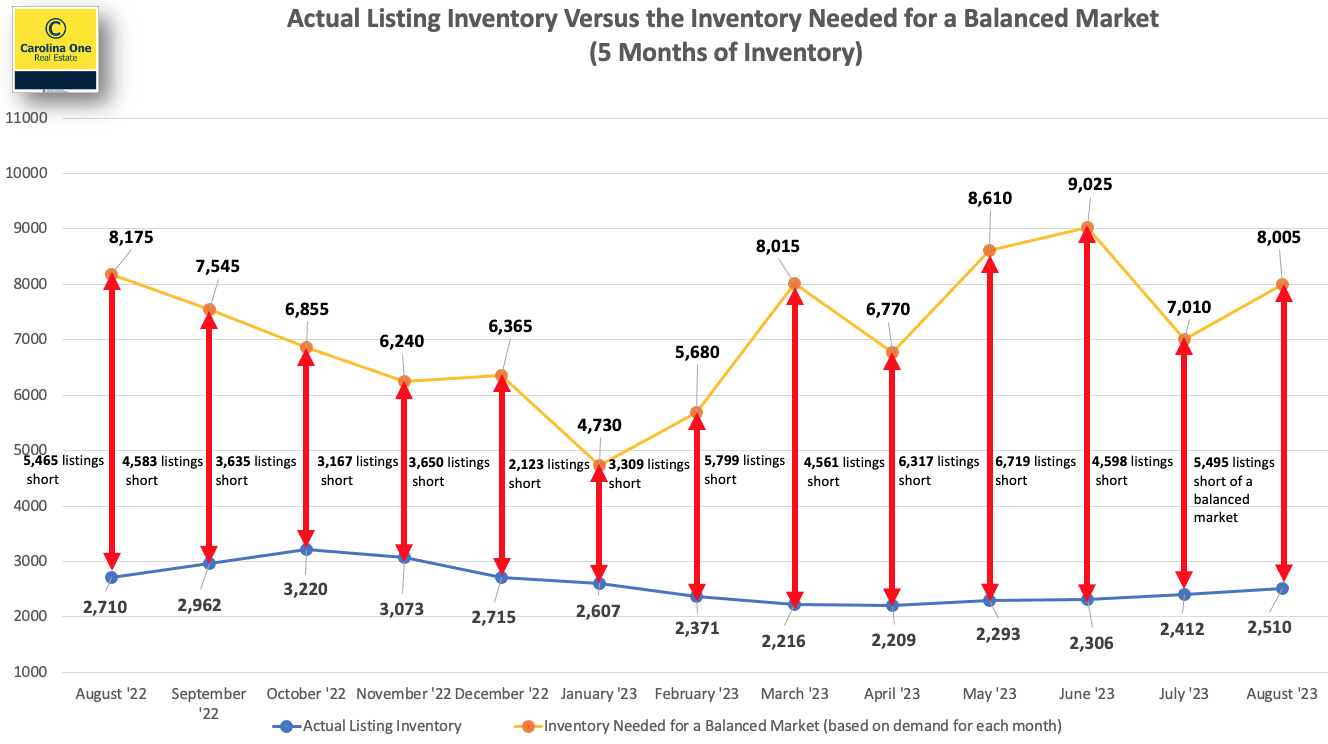

(5) Active Inventory stands at 2,510 listings. We haven’t seen much inventory growth this summer and inventory typically starts a slow seasonal decline in September or October. It is believed this may likely put upward pressure on prices, or at the very least hold prices steady.

While this level of inventory is a significant increase over the 1,035 listing “floor” that we set in February of 2022:

Roughly an additional 5,500 listings is needed market wide to achieve a balanced market (5 months of inventory)

The gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is substantial. The chart below is an attempt to express this visually.

(6) The number of new listings taken in August was even with the same month a year prior for the first time in two years, but inventory still remains low.

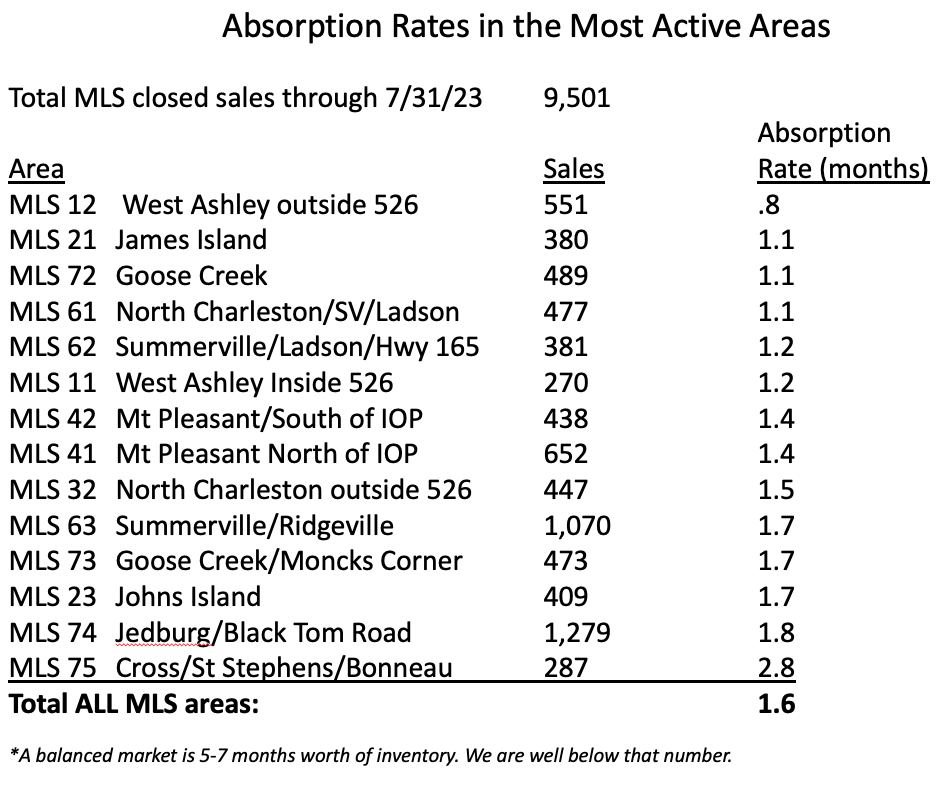

7) The Charleston market has about six or seven weeks of inventory as a whole, still solidly a seller’s market (this can vary by price range and specific location). The most active areas have inventory levels in the 3-6 week range.

(8) New construction represents 46% of all pending contracts in the MLS and new construction comprises about 32% of the closings.

New Homes “pendings” will always be higher than new homes closings as new construction typically sits in pending status for far longer than a resale, and the new homes tend to “pile up” in pending status, so new homes actually represent about 32% of the sales market currently

New homes represent 33% of the available inventory, currently.

(9) Foreclosures and Short Sales continue to hold at a combined .6% of all available listings currently. This is down from 1.8% of all available listings on 1/1/2020. This market has very few “newly distressed” properties in the pipeline.

“Serious delinquencies fell to the lowest level since August 2006; the July delinquency rate was negligibly higher than the lowest level ever recorded.” – Black Knight Mortgage Monitor statement from two weeks ago.

Record home equity is driving the low delinquency rate along with high levels of employment.

(10)We are at roughly double the monthly pre-pandemic sales levels of $1MM+ properties. This market segment remains surprisingly robust.

SC Housing has down payment assistance for buyer’s who Qualify. The assistance is forgivable after 15 years.

The home sales price and income limit recently increased. Currently, the sales price limit is $395,000 for most SC counties. The income limit for for 1 or 2 person households in Berkeley County is now $121,500 and for households of 3 or more people, it is $141,820. The chart below shows the various counties and income limits.

With our connection with Contractors on Call, I can help you work out the details of home repairs without paying until you close your home! Very Convenient!

Contractors on Call, powered by Punchlist, has fast and free estimates, their work offers a transferable warranty and they have all licensed trades under one roof. This can be a convenient option for homeowners looking to sell their property.

Home Swap is a loan program designed to help current homeowners buy a new home without having to sell their existing home first. It functions similar to a traditional bridge loan, which is a short-term loan that people can use in the lead up to securing long-term financing. Instead of having to sell first and then find temporary housing while searching for a new home to buy (or worse, take on two mortgages), homeowners get the flexibility to close on their new home and then go through the process of selling. That means no double mortgages and no juggling timelines to try and minimize the period in between closings.

How does Knock Home Swap work?

The Home Swap program works like this:

Homeowners get pre-approved and fully underwritten for a homebuying loan with Knock, the company behind Home Swap. Secured at a convenience fee of 1.25% of the new home’s purchase price, the loan also includes a down payment advance. (Home Swap users can pay that 1.25% can at closing or roll it into what they borrow.)

When they find the home they want to buy, the purchasers put in their offer without a sales contingency—meaning they do not have to sell their previous home to close. Upon move-in, they’ll start making payments on their new mortgage while a Knock Equity Advance covers payments on their old mortgage for up to six months.

While settling into their new home, the homeowners will list their old home for sale. If they need to make any improvements before the sale, they can take out up to $25,000 in Home Swap loans for the job.

Homeowners sell their old homes using a real estate agent of their choice. Suppose the home doesn’t sell on the open market within the six months that mortgage payments are being fronted through Home Swap. In that case, homeowners have the option to sell their home directly to Knock for a pre-determined offer—usually about 80% to 85% of fair market value for the property.

Just like with a standard home loan, Knock sells your loan after you close, and you’ll make your mortgage payments to the company that buys it. Payment for the Home Swap loan is a 1.25% convenience fee.

What are the benefits of using Home Swap?

The biggest benefit is that homeowners do not have to sell their current home before buying their new one. This is a huge advantage since most people don’t have the financial flexibility to take on the risk of paying two mortgages at the same time. Of course, you’re still paying for your first mortgage with Home Swap, but it’s rolled into the amount that you borrow so that you won’t be cutting two checks every month.

Another major benefit is that buyers can avoid a sale contingency.

Home Swap vs. traditional lending

Keep in mind that with convenience comes fees, so you’ll pay extra for it through that set 1.25% convenience fee, which may be more than the origination fee you would have secured on a traditional loan.

What’s the same?

Closing costs

You’ll still owe all normal closing costs if you go with Home Swap, including title-related fees, attorney fees, and lending fees. The one difference here is that if you go with Home Swap, you’ll also owe a 1.25% convenience fee; however that can roll into your mortgage if you don’t want to pay it at closing.

Varying rates

As with any home loan, your rates will still depend on your qualifications. The better your credit and the less risky of a borrower you are, the better terms you’ll get on your loan, whether that’s with Home Swap or with another lender.

Flexible housing options

Like with any home loan, you can use Home Swap to buy and sell various housing types. Condos, townhomes, and new construction are all eligible and will not preclude you from getting financing.

What’s different?

Non-contingent financing

So long as your qualifying information doesn’t change between when you’re approved and when you close, you’re guaranteed cash-backed, non-contingent financing with a Home Swap loan. This gives the seller 100% assurance that financing will come through on closing day, regardless of whether your other home is sold.

No-sale contingencies are possible with traditional lending, but because they’re risky for lenders, you’ll need to have the cash to support them. Home equity loans, bridge loans, or savings are ways to do it, but they’ll exist separately from your new mortgage.

Market availability – (AVAILBLE IN SC)

Other options for buying and selling a house at the same time

Home Swap is a nice option for buyers who also need to sell, but it’s not the only one. If you’re in the market to buy and sell at the same time, here are some of the other ways that you can finance the move.

Home Equity Line of Credit (HELOC)

A HELOC is a loan that allows homeowners to borrow up to the amount of equity in their current home. The longer you’ve lived in your current home, the more equity you’ll have in it—and the more you’ll be able to borrow with a HELOC.

HELOCs are sort of like credit cards in that you have a set limit to the loan (your equity balance), and you can take out what you need when you need it. To buy a new home, however, you can go ahead and take out as much of the limit as you need and then put that toward your purchase.

Note that while a standard HELOC repayment period is about 20 years, you have to pay back the loan in full before you close on a sale of the property. That shouldn’t be an issue as long as you can sell your home for at least as much as your mortgage is currently worth.

Bridge loan

Home Swap is an example of a bridge loan, a short-term loan that you can take out to “bridge” the period between buying a new home and selling your old one. A standard bridge loan (also known as a swing loan or gap financing) won’t come with the additional perks of Home Swap, but it could still be a good choice depending on your circumstances.

Like a HELOC, you’ll borrow against your home’s equity with a bridge loan. Unlike a HELOC, you don’t have an extended repayment period that can hold you over if your home doesn’t sell right away. Bridge loan repayment periods usually start after 12 months, at which point you’d be responsible for paying back the loan and paying the mortgage on your new home, provided you weren’t able to sell.

The benefits to a bridge loan are the flexibility it affords and that it gives you the ability to put down a non-contingent offer and, potentially, a higher down payment as well. Drawbacks include the aforementioned short repayment period, high interest rates, and additional closing costs.

Information from Knock.com

If you would like to explore buying a new home and selling your current home, I would love to help!

Tucked away in The Hamlets of Crowfield Plantation, is a rare property that offers privacy and tranquility in a desirable community with easy access to all that the Low Country has to offer!

This Luxury property has a private security gate, 7795 sqft, 7 Bedrooms, 8 Bathrooms, A State-Of-The Art Movie Theatre, A 6 Car Garage, A Separate Apartment, One Acre Lot, Golf Course and Pond Views, and so much more!

Nestled in the heart of Goose Creek, South Carolina, lies a community that exudes elegance, charm and character. Known as Crowfield Plantation, this stunning residential community has earned the reputation as a hidden gem within the Charleston metro area.

The development of Crowfield began in the early 1990’s and was built on a historic site.

The neighborhood’s peaceful environment offers an escape from the hustle and bustle of everyday life, as well as a welcome retreat from the busier parts of the Lowcountry. The community consists of residential and commercial parcels and offers a variety of housing types and price-ranges.

Today, Crowfield Plantation offers its residents a myriad of recreational and entertainment options. Its scenic lake, ponds and walking trails are a popular spot for runners and walkers alike, and the community pools, parks, clubhouse and tennis courts provide endless opportunities for leisure activities. The Crowfield golf course is located in The Hamlets of Crowfield Plantation which is a great feature for avid golfers and visitors alike. VIEW ALL HOMES AVAILABLE FOR SALE IN CROWFIELD

With easy access to Interstate 26 and a location that’s close to local attractions, Charleston and Summerville, Crowfield Plantation residents have plenty of shopping and dining options. There are also several public schools located nearby.

But perhaps what sets Crowfield Plantation apart from other residential communities is the true sense of community and it’s serene environment. Crowfield’s immense greenspace, tree-filled buffers, lakes, ponds and playgrounds along with community events. create a true sense of camaraderie, tranquility and belonging.

So if you’re looking for a peaceful escape that offers a strong sense of community and a wealth of recreational opportunities, consider Crowfield Plantation as your next home.

1) Written sales market wide finished -7% in July of ’23 versus July of ’22.

July finishing at -7% to last July is an excellent outcome

(2) Early August showed a relatively strong 314 properties go under contract. Sales (green line) have remained remarkably close to the 15 year average (blue line) for about two and a half months.

The orange line represents ratified contracts by week last year…the green line is this year…and the blue line is the 15 year average for each week.

Green line=2023 Orange Line=2022 Blue Line=15-year average

(3) Mortgage rates remain elevated, and this is obviously holding back sales levels.

6.5% may be the “magic number”

When 30 year mortgage rates trend below that number and stay there for a reasonable period of time, buyers will come off of the sidelines and resale listing inventory will start to come back online at a higher rate than what we are seeing currently

(4) The Median sale price in the Charleston market continues to stay in a tight band between $400k and $420k where it has been for most of the last 15 months, sitting at $405k in June.

(5) Active Inventory stands at 2,412 listings. We haven’t seen much inventory growth this summer and inventory typically starts a slow seasonal decline in September or October. This will also likely put upward pressure on prices, or at the very least hold prices steady.

While this level of inventory is a significant increase over the 1,035 listing “floor” that we set in February of 2022:

We need roughly 4,600 additional listings market wide to achieve a balanced market (5 months of inventory)

The gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is substantial. The chart below is an attempt to express this visually.

(6) There continues to be a reluctance of owners to list their property; new listings taken were down 17% in July of ’23 versus July of ’22.

7) The Charleston market has about six or seven weeks of inventory as a whole, still solidly a seller’s market (this can vary by price range and specific location, of course). The most active areas have inventory levels in the 3-5 week range.

(8) New construction represents 46% of all pending contracts in the MLS and new construction comprises about 32% of the closings.

New Homes “pendings” will always be higher than new homes closings as new construction typically sits in pending status for far longer than a resale, and the new homes tend to “pile up” in pending status, so new homes actually represent about 32% of the sales market currently

New homes represent 33% of the available inventory currently

New construction does not appear to be poised to ride to the rescue of our inventory problem; the last 12 months of permits issued in the tri-county sits at almost exactly the midpoint (5,354 single family permits) between the historical high point (8,084 permits) and the historical low point (2,732 permits)

To meet demand in a low resale inventory environment, it is projected that we need approximately 7,000-8,000 new single-family builds in Charleston annually.

(9) Foreclosures and Short Sales continue to hold at a combined .6% of all available listings currently. This is down from 1.8% of all available listings on 1/1/2020. This market has been and continues to be basically nonexistent and there are very few “newly distressed” properties in the pipeline.

“Serious delinquencies fell to the lowest level since August 2006; June delinquency rate was the third lowest on record.” – Black Knight Mortgage Monitor Headline from last week

Record home equity is driving the low delinquency rate along with high levels of employment. Many homeowners do not want to walk away from their equity.

(10)We are at roughly double the monthly pre-pandemic sales levels of $1MM+ properties. This market segment remains surprisingly robust.

f you have considered buying or selling a home in The Tri-County area, I would love to help!

{kind=link}