A capital gain is the profit made when selling an investment or asset, including real estate. The capital gains tax is the levy on that profit when an investment is sold. It is owed for the tax year during which the investment is sold.

Long-term capital gains tax is the tax levied on profits of an asset or investment that was owned for over one year. The long-term capital gains tax rate vary and depend on your income but the rates are typically lower than your ordinary income tax rate

If the investment or asset is owned for less than a year when the gain is made, then the short-term capital gains tax applies. The short-term rate is typically determined by the taxpayer’s ordinary income bracket – but can vary in some circumstances.

The Primary Residence Exclusion. IRS – Section 121

The Internal Revenue Service (IRS) allows homeowners to exclude a certain amount of gains that result from the sale of their primary home from their income. This is known as the Section 121 rule.

Single Homeowners may exclude up to $250,000 of gains on the sale of their property, and married homeowners filing jointly can exclude up to $500,000.

To be eligible for these exclusions You must have owned the home for at least two years AND have lived in the home as your primary residence for at least two years of the previous five years prior to the sale date. The two-year period does not have to be consecutive. See More Here at IRS

Investment Property Deferment- 1031 Tax Exchange in Real Estate

Section 1031 is a provision of the Internal Revenue Code (IRC) that allows a businesses or the owners of investment property to defer federal taxes on some exchanges of real estate. The provision is used by investors who are selling one property and reinvesting the proceeds in one or more other properties.

Qualifying Section 1031 exchanges are called 1031 exchanges, or like-kind exchanges.

In General, A 1031 exchange allows investors to defer taxes on the profits of sold investments. The exchange can be complex with rigid time frames for identifying the replacement property and reqiures a Qualified Intermediary (QI) to oversee and process and the funds.

Tax laws and codes are complex and can change, always consult a tax professional to review your unique situation.

Newcomers to S.C. greatly accelerated during the pandemic years as remote employment took hold and that trend has continued. South Carolina was recently crowned the fastest-growing state in the nation by the U.S. Census Bureau based on percentage growth, adding roughly 90,000 additional residents to the population.

Top 10 States or State Equivalent by Percent Growth: 2022 to 2023

Rank

Geographic Area

April 1, 2020 (Estimates Base)

July 1, 2022

July 1, 2023

Percent Growth

1

South Carolina

5,118,422

5,282,955

5,373,555

1.7

2

Florida

21,538,216

22,245,521

22,610,726

1.6

3

Texas

29,145,459

30,029,848

30,503,301

1.6

4

Idaho

1,839,117

1,938,996

1,964,726

1.3

5

North Carolina

10,439,459

10,695,965

10,835,491

1.3

6

Delaware

989,946

1,019,459

1,031,890

1.2

7

District of Columbia

689,548

670,949

678,972

1.2

8

Tennessee

6,910,786

7,048,976

7,126,489

1.1

9

Utah

3,271,614

3,381,236

3,417,734

1.1

10

Georgia

10,713,771

10,913,150

11,029,227

1.1

This population boom created more demand for housing, but inventory has been constrained, keeping prices afloat and putting pressures on rents.

The population growth is mainly concentrated in larger cities with populations declining in some rural areas. Local governments increasingly engage in managing growth and pursuing affordable housing options for workforce.

Mortgage interest rates have fallen from their peak of nearly 8 percent in 2023, and many financial experts speculate interest rates will continue to moderate. Inventory is expected to rise, and lower interest rates should help make homes more affordable. Whether the rising supply can keep up with demand remains to be seen.

Tax credit: These are dollar-for-dollar reductions on your tax bill. When you claim a tax credit, the amount you owe goes down the exact same dollar amount.

Tax incentive: These encourage taxpayers to do something, like install efficient appliances, in exchange for a tax reduction.

Tax refund: You’re probably familiar with this one already. You’ll get a refund if you pay more in taxes — say, through your paycheck withholdings — than you actually owe.

Tax rebate: These are retroactive tax decreases. Unlike refunds, they can come at any time of year. Rebates are often offered to stimulate the economy, because people tend to spend them immediately.

Tax break: A general term referring to various tax benefits. These could be credits, deductions, exemptions and others.

Tax benefit: Similar to a tax break, these lower your tax liability.

Home improvement tax deduction: Qualifying improvements to your home that qualify for tax deductions.

Most home improvements, like putting on a new roof or performing routine maintenance, don’t qualify for any immediate tax breaks. However, some (known as capital improvements) may raise the value of your home. In that case, you may see a benefit when you sell.

For immediate benefits, check out these incentives that will reduce your 2023 taxes:

Energy efficiency tax credits

Reducing energy consumption saves money and natural resources. The IRA includes multiple clean energy tax credits to help you do both.

Heat pumps: Your air conditioning and furnace are two of the biggest energy users in your home. Switching to an energy efficient heat pump can net you a 30% credit, up to $2,000.

Windows and doors: Replacing leaky doors and windows brings a 30% credit on the cost, up from 10% last year. Credits are capped at $600 for windows and $500 for two doors.

Electrical upgrades: If you need to update your electrical panel to handle new appliances, the government will pay 30%, up to $600.

Home energy audit: To get the most out of these tax incentives, start with a home energy audit. A credit of up to $150 offsets the cost.

Don’t stop there. “[I]incentives on items like solar, energy storage, EVs [electric vehicles] and more are incredibly generous,” says Greg Fasullo, CEO of Elevation, a residential clean technology company.

Installing solar panels gets you a 30% credit. Depending on the size of the project, Fasullo predicts you could save $6,000, based on the average rooftop solar installation cost of $20,000.

Home office tax deduction

Working from home since the pandemic? Fifty-eight percent of American workers are, too, at least part of the time.

If you use a portion of your home exclusively for business purposes, “you may be able to deduct a portion of your mortgage interest, property taxes, and other expenses related to that space,” says Seth Diener, a private wealth manager at Diener Money Management.

The Internal Revenue Service (IRS) has specific rules about what qualifies as a home office, though. If you’re doing Zoom calls from the kitchen table where you eat dinner every night, that doesn’t count. You must have a separate room or area that’s only used for your home office. If that’s you, you can calculate this deduction two ways:

Regular method: Figure out the percentage of your home you use for work. The deduction you can claim is based on this number, and whether your expenses are direct or indirect.

Simplified method: Calculate the square footage of your home office and multiply it by $5 per sq. ft., up to 300 sq. ft., with a maximum deduction of $1,500.

Medical improvements

“If you have medical upgrades that are prescribed by a doctor, such as wheelchair ramps or other accessibility features, these may be deductible as medical expenses,” says Andrew Latham, a certified financial planner and director of content at SuperMoney.com.

The IRS website offers a non-exhaustive list of qualifying capital expenses, including widening doorways, moving electrical devices, adding handrails and grading the exterior.

Note: If the medical home improvement raises the value of your home, the deduction will be based on the difference between the cost of the improvement and the increase in property value.

Rental property investments

Improvements to rental properties fall under a deduction called depreciation.

“Improvements to a rental property are usually considered deductible business expenses,” Latham says. “However, these incentives are subject to specific rules and limits, so it’s advisable to check current tax laws or consult with a tax professional.”

Federal vs. State Home Improvement Tax Incentives

What if you put in that heat pump and got back $2,000 from the federal government? Could you also claim the credit on your state return?

“Yes, in some instances, you can qualify for multiple tax breaks for the same project,” Latham says. “[I]f you install a new energy-efficient heat pump, you might be eligible for a federal tax credit, a state-level incentive, and potentially a rebate from your local utility company.”

Always check with a tax professional for advice as rules and laws change.

Home Swap is a loan program designed to help current homeowners buy a new home without having to sell their existing home first. It functions similar to a traditional bridge loan, which is a short-term loan that people can use in the lead up to securing long-term financing. Instead of having to sell first and then find temporary housing while searching for a new home to buy (or worse, take on two mortgages), homeowners get the flexibility to close on their new home and then go through the process of selling. That means no double mortgages and no juggling timelines to try and minimize the period in between closings.

How does Knock Home Swap work?

The Home Swap program works like this:

Homeowners get pre-approved and fully underwritten for a homebuying loan with Knock, the company behind Home Swap. Secured at a convenience fee of 1.25% of the new home’s purchase price, the loan also includes a down payment advance. (Home Swap users can pay that 1.25% can at closing or roll it into what they borrow.)

When they find the home they want to buy, the purchasers put in their offer without a sales contingency—meaning they do not have to sell their previous home to close. Upon move-in, they’ll start making payments on their new mortgage while a Knock Equity Advance covers payments on their old mortgage for up to six months.

While settling into their new home, the homeowners will list their old home for sale. If they need to make any improvements before the sale, they can take out up to $25,000 in Home Swap loans for the job.

Homeowners sell their old homes using a real estate agent of their choice. Suppose the home doesn’t sell on the open market within the six months that mortgage payments are being fronted through Home Swap. In that case, homeowners have the option to sell their home directly to Knock for a pre-determined offer—usually about 80% to 85% of fair market value for the property.

Just like with a standard home loan, Knock sells your loan after you close, and you’ll make your mortgage payments to the company that buys it. Payment for the Home Swap loan is a 1.25% convenience fee.

What are the benefits of using Home Swap?

The biggest benefit is that homeowners do not have to sell their current home before buying their new one. This is a huge advantage since most people don’t have the financial flexibility to take on the risk of paying two mortgages at the same time. Of course, you’re still paying for your first mortgage with Home Swap, but it’s rolled into the amount that you borrow so that you won’t be cutting two checks every month.

Another major benefit is that buyers can avoid a sale contingency.

Home Swap vs. traditional lending

Keep in mind that with convenience comes fees, so you’ll pay extra for it through that set 1.25% convenience fee, which may be more than the origination fee you would have secured on a traditional loan.

What’s the same?

Closing costs

You’ll still owe all normal closing costs if you go with Home Swap, including title-related fees, attorney fees, and lending fees. The one difference here is that if you go with Home Swap, you’ll also owe a 1.25% convenience fee; however that can roll into your mortgage if you don’t want to pay it at closing.

Varying rates

As with any home loan, your rates will still depend on your qualifications. The better your credit and the less risky of a borrower you are, the better terms you’ll get on your loan, whether that’s with Home Swap or with another lender.

Flexible housing options

Like with any home loan, you can use Home Swap to buy and sell various housing types. Condos, townhomes, and new construction are all eligible and will not preclude you from getting financing.

What’s different?

Non-contingent financing

So long as your qualifying information doesn’t change between when you’re approved and when you close, you’re guaranteed cash-backed, non-contingent financing with a Home Swap loan. This gives the seller 100% assurance that financing will come through on closing day, regardless of whether your other home is sold.

No-sale contingencies are possible with traditional lending, but because they’re risky for lenders, you’ll need to have the cash to support them. Home equity loans, bridge loans, or savings are ways to do it, but they’ll exist separately from your new mortgage.

Market availability – (AVAILBLE IN SC)

Other options for buying and selling a house at the same time

Home Swap is a nice option for buyers who also need to sell, but it’s not the only one. If you’re in the market to buy and sell at the same time, here are some of the other ways that you can finance the move.

Home Equity Line of Credit (HELOC)

A HELOC is a loan that allows homeowners to borrow up to the amount of equity in their current home. The longer you’ve lived in your current home, the more equity you’ll have in it—and the more you’ll be able to borrow with a HELOC.

HELOCs are sort of like credit cards in that you have a set limit to the loan (your equity balance), and you can take out what you need when you need it. To buy a new home, however, you can go ahead and take out as much of the limit as you need and then put that toward your purchase.

Note that while a standard HELOC repayment period is about 20 years, you have to pay back the loan in full before you close on a sale of the property. That shouldn’t be an issue as long as you can sell your home for at least as much as your mortgage is currently worth.

Bridge loan

Home Swap is an example of a bridge loan, a short-term loan that you can take out to “bridge” the period between buying a new home and selling your old one. A standard bridge loan (also known as a swing loan or gap financing) won’t come with the additional perks of Home Swap, but it could still be a good choice depending on your circumstances.

Like a HELOC, you’ll borrow against your home’s equity with a bridge loan. Unlike a HELOC, you don’t have an extended repayment period that can hold you over if your home doesn’t sell right away. Bridge loan repayment periods usually start after 12 months, at which point you’d be responsible for paying back the loan and paying the mortgage on your new home, provided you weren’t able to sell.

The benefits to a bridge loan are the flexibility it affords and that it gives you the ability to put down a non-contingent offer and, potentially, a higher down payment as well. Drawbacks include the aforementioned short repayment period, high interest rates, and additional closing costs.

Information from Knock.com

If you would like to explore buying a new home and selling your current home, I would love to help!

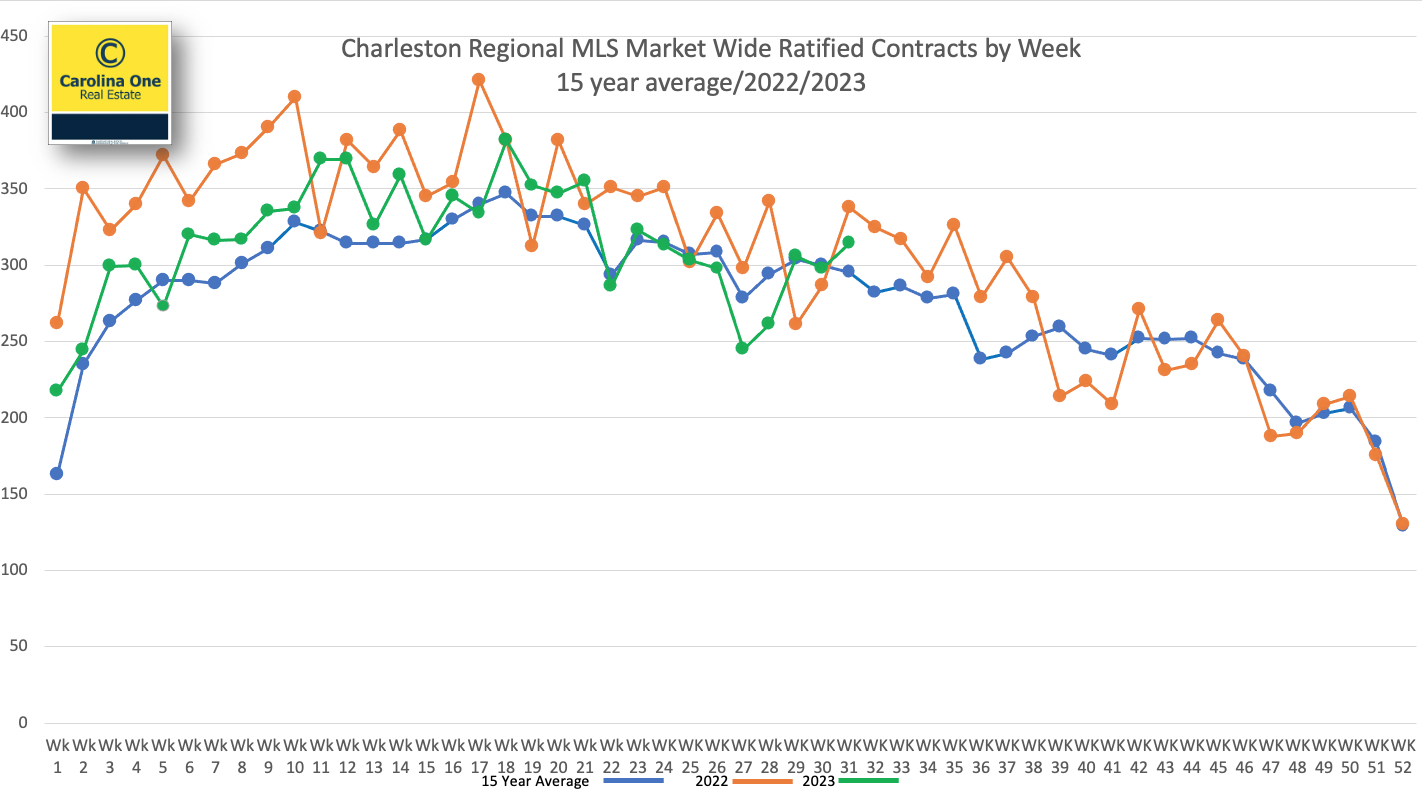

1) Written sales market wide finished -7% in July of ’23 versus July of ’22.

July finishing at -7% to last July is an excellent outcome

(2) Early August showed a relatively strong 314 properties go under contract. Sales (green line) have remained remarkably close to the 15 year average (blue line) for about two and a half months.

The orange line represents ratified contracts by week last year…the green line is this year…and the blue line is the 15 year average for each week.

Green line=2023 Orange Line=2022 Blue Line=15-year average

(3) Mortgage rates remain elevated, and this is obviously holding back sales levels.

6.5% may be the “magic number”

When 30 year mortgage rates trend below that number and stay there for a reasonable period of time, buyers will come off of the sidelines and resale listing inventory will start to come back online at a higher rate than what we are seeing currently

(4) The Median sale price in the Charleston market continues to stay in a tight band between $400k and $420k where it has been for most of the last 15 months, sitting at $405k in June.

(5) Active Inventory stands at 2,412 listings. We haven’t seen much inventory growth this summer and inventory typically starts a slow seasonal decline in September or October. This will also likely put upward pressure on prices, or at the very least hold prices steady.

While this level of inventory is a significant increase over the 1,035 listing “floor” that we set in February of 2022:

We need roughly 4,600 additional listings market wide to achieve a balanced market (5 months of inventory)

The gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is substantial. The chart below is an attempt to express this visually.

(6) There continues to be a reluctance of owners to list their property; new listings taken were down 17% in July of ’23 versus July of ’22.

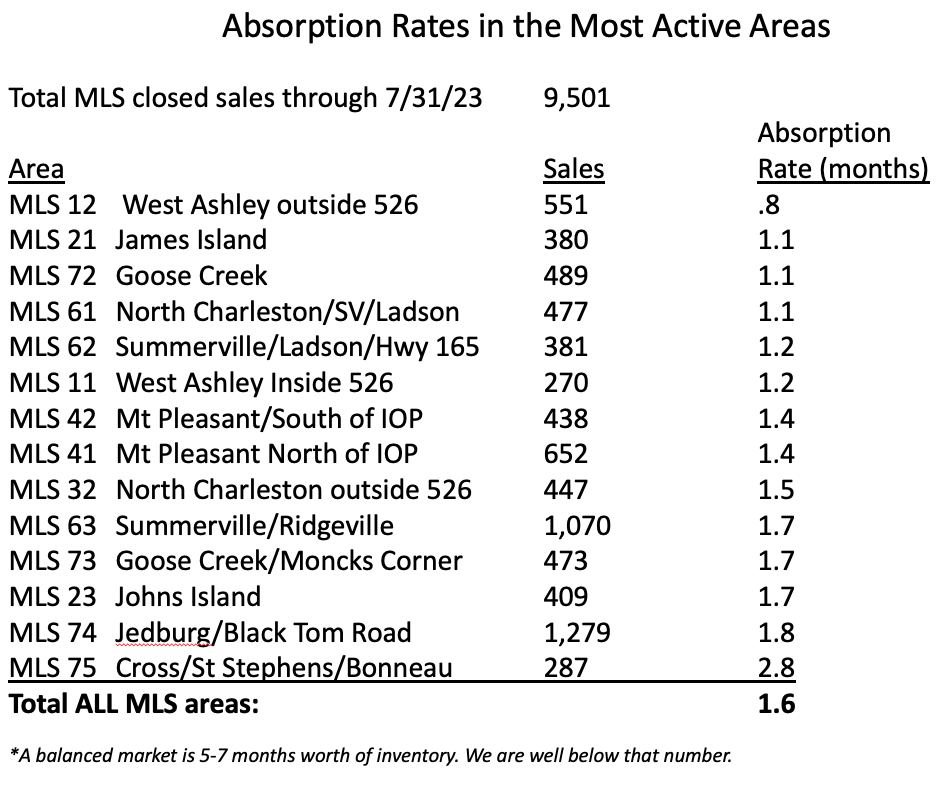

7) The Charleston market has about six or seven weeks of inventory as a whole, still solidly a seller’s market (this can vary by price range and specific location, of course). The most active areas have inventory levels in the 3-5 week range.

(8) New construction represents 46% of all pending contracts in the MLS and new construction comprises about 32% of the closings.

New Homes “pendings” will always be higher than new homes closings as new construction typically sits in pending status for far longer than a resale, and the new homes tend to “pile up” in pending status, so new homes actually represent about 32% of the sales market currently

New homes represent 33% of the available inventory currently

New construction does not appear to be poised to ride to the rescue of our inventory problem; the last 12 months of permits issued in the tri-county sits at almost exactly the midpoint (5,354 single family permits) between the historical high point (8,084 permits) and the historical low point (2,732 permits)

To meet demand in a low resale inventory environment, it is projected that we need approximately 7,000-8,000 new single-family builds in Charleston annually.

(9) Foreclosures and Short Sales continue to hold at a combined .6% of all available listings currently. This is down from 1.8% of all available listings on 1/1/2020. This market has been and continues to be basically nonexistent and there are very few “newly distressed” properties in the pipeline.

“Serious delinquencies fell to the lowest level since August 2006; June delinquency rate was the third lowest on record.” – Black Knight Mortgage Monitor Headline from last week

Record home equity is driving the low delinquency rate along with high levels of employment. Many homeowners do not want to walk away from their equity.

(10)We are at roughly double the monthly pre-pandemic sales levels of $1MM+ properties. This market segment remains surprisingly robust.

f you have considered buying or selling a home in The Tri-County area, I would love to help!

There’s no doubt that today’s housing market is changing, and everything we see right now indicates it is time to sell. Here’s a look at why selling now is likely to drive the greatest return on your largest investment.

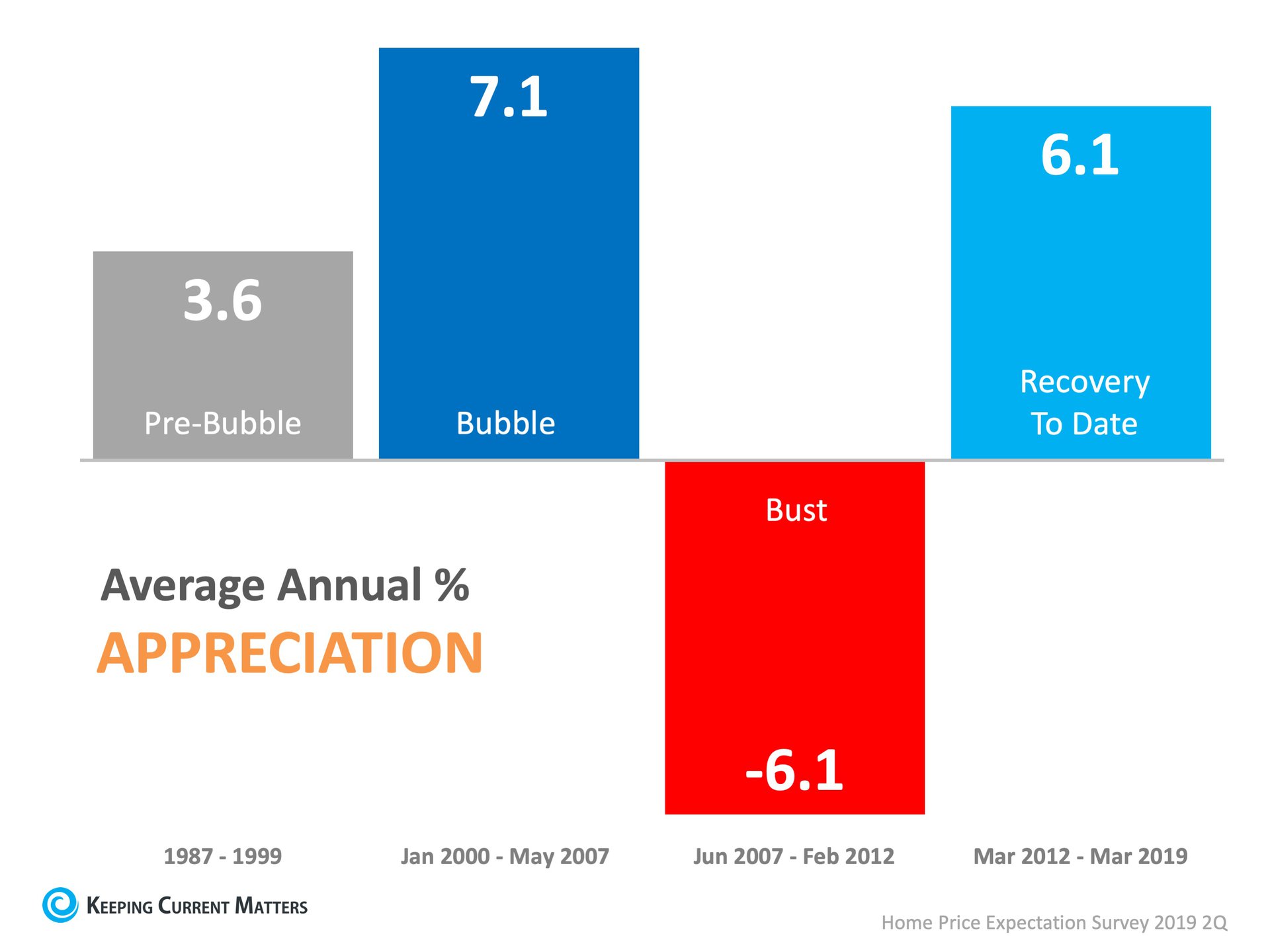

Home values have been appreciating for several years now, growing at a strong, steady, and impressive pace. In fact, the average annual appreciation rate since 2012 has nearly doubled the average rate from the more normal market of the 1990s (think: pre-bubble).Appreciation, however, is projected to shift back toward normal, meaning home prices will likely keep climbing over the next few years, but they are not projected to continue to increase at such a high rate.

Here’s What That Means for Homeowners:

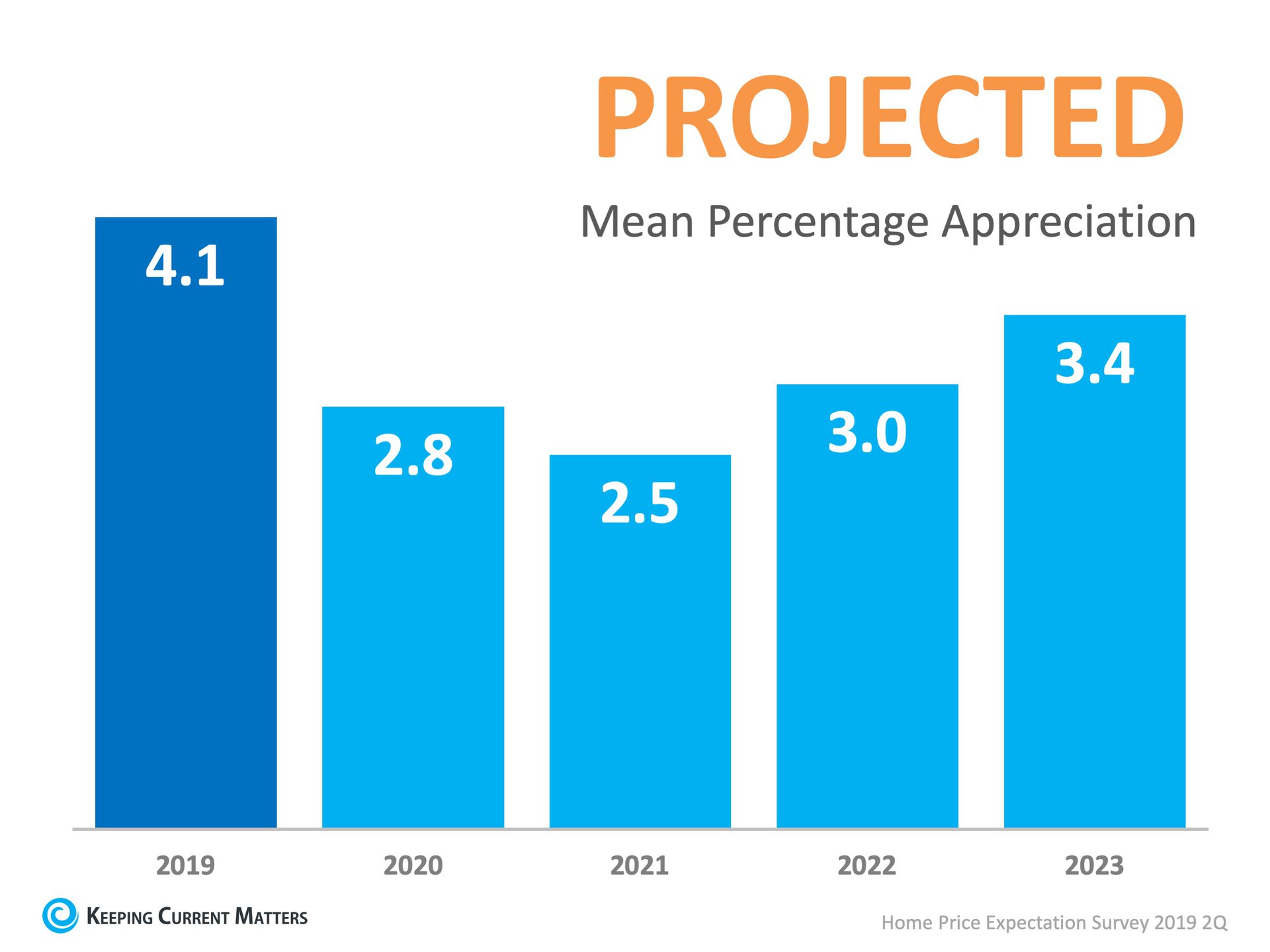

As noted in the latest Home Price Expectation Survey (HPES) powered by Pulsenomics, experts forecast an average annual appreciation rate closer to 3.2% over the next five years, which is more in line with a historically normal market (3.6%). The good news is, there’s still time to take advantage of the current strength of home prices by selling your house now.Looking at the projections as they stand today, 2019 is slated to drive the strongest appreciation as compared to the upcoming few years. With average home prices still on the rise, the pace at which they are predicted to continue increasing will likely soften by 2020.

Bottom Line

If you’re thinking about selling your house, now is a great time to make your move. Don’t get stuck waiting until projected home price appreciation rates potentially re-accelerate again in 2023. You’ll likely earn the greatest return on your investment by selling now before the prices start to normalize next year.

There are many financial benefits to homeownership, but probably none more important than its ability to create family wealth.

How Housing Matters is a joint project of the Urban Land Institute and the MacArthur Foundation. It is an online resource for research and information on how homeownership contributes to individual and community success.

“The ladder to economic success can stretch only so high without the asset-building power of homeownership.”

To this point, National Association of Realtors’ (NAR) Economists’ Outlook Blog revealed in a recent post:

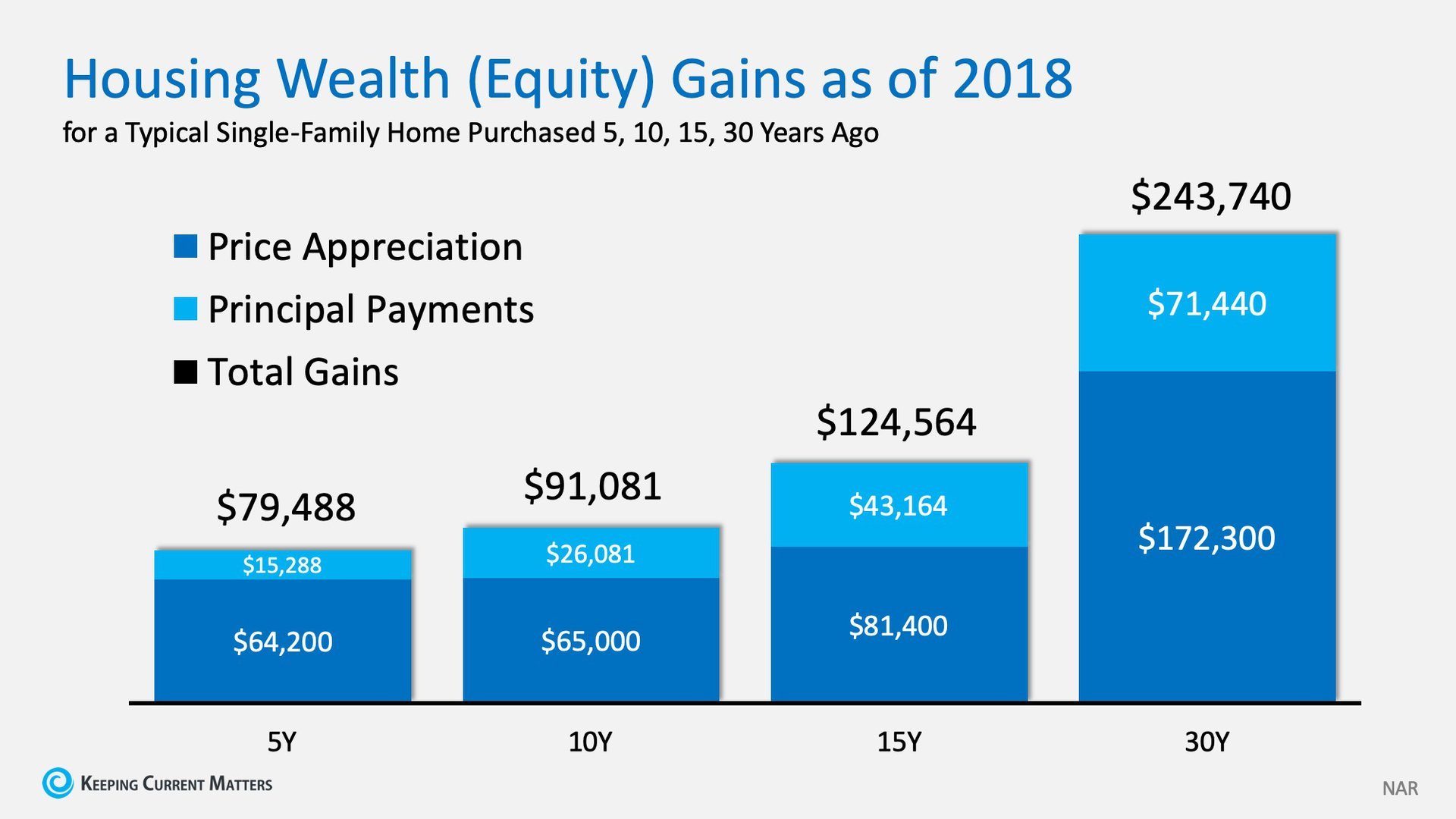

“Housing wealth contributes positively to the homeowner’s and children’s economic condition, because home equity can be tapped for expenditures such as investing in another property (which can generate rental income), home renovation (which further increases the home value), a child’s college education, emergency or major life events, or expenses in retirement…

Housing wealth (or net worth or equity) is built up over time via the home price appreciation and the principal payments that the homeowner makes on the loan.”

Just last month, NAR’s Chief Economist, Lawrence Yun, explained that even though home appreciation has slowed, homeowners are still building wealth:

“Homeowners in the majority of markets are continuing to enjoy price gains, albeit at a slower rate of growth. A typical homeowner accumulated $9,500 in wealth over the past year.”

Later in life, this wealth is crucial…

This wealth is important to a family’s retirement plans. In a recent report from the Joint Center for Housing Studies at Harvard University titled, Housing America’s Older Adults 2018, they revealed that a renter 65 years old or older has a net worth of $6,710. Meanwhile, a homeowner 65+ years old has a net worth of $319,200. That huge difference will allow for a dramatic upgrade in one’s lifestyle during your retirement years.

Bottom Line

Homeownership builds wealth. This, in turn, allows families to have more and better options when it comes to their children and their life in retirement.

![Americans Choose Real Estate as the Best Investment [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2022/01/20143424/20220121-NM.png)