SC Housing Palmetto Heroes Program honors educators, first responders and community service personnel in the fields of law enforcement, corrections, firefighting, emergency medical services and health care, as well as active-duty military, members of the SC Army National Guard, SC Air National Guard and Veterans of the U.S. Armed Forces. The program typically offers a variety financing options with a reduced fixed interest rate AND Down Payment Assistance.

The program is first come first serve and lasts until funds are depleted. Last year (2023) the program featured $10,000 down payment assistance for qualified applicants. 2024 details have not been released yet, but should be announced very soon, within the coming weeks.

I am watching for the details of the new issue. If you are interested in this program, please contact me and I would be glad to help!

Are you feeling a bit unsure about what’s really happening with mortgage rates? That might be because you’ve heard they’re coming down. But then you read somewhere else that they’re up again. And that may leave you scratching your head and wondering what’s true.

The simplest answer is: that what you read or hear will vary based on the time frame they’re looking at. Here’s some information that can help clear up the confusion.

Mortgage Rates Are Volatile by Nature

Mortgage rates don’t move in a straight line. There are too many factors at play for that to happen. Instead, rates bounce around because they’re impacted by things like economic conditions, decisions from the Federal Reserve, and so much more. That means they might be up one day and down the next depending on what’s going on in the economy and the world as a whole.

Take a look at the graph below. It uses data from Mortgage News Daily to show the ebbs and flows in the 30-year fixed mortgage rate since last October:

If you look at the graph, you’ll see a lot of peaks and valleys – some bigger than others. And when you use data like this to explain what’s happening, the story can be different based on which two points in the graph you’re comparing.

For example, if you’re only looking at the beginning of this month through now, you may think mortgage rates are on the way back up. But, if you look at the latest data point and compare it to the peak in October, rates have trended down. So, what’s the right way to look at it?

The Big Picture

Mortgage rates are always going to bounce around. It’s just how they work. So, you shouldn’t focus too much on the small, daily changes. Instead, to really understand the overall trend, zoom out and look at the big picture.

When you look at the highest point (October) compared to where rates are now, you can see they’ve come down compared to last year. And if you’re looking to buy a home, this is big news. Don’t let the little blips distract you. The experts agree, overall, that the larger downward trend could continue this year.

Despite the ups and downs, many analysists predict mortgage rates will, over-all, move in a slow declining path as the year progresses, but many factors can influence the trajectory and so only time will tell.

if you’re looking to buy a home, you’ve probably been paying close attention to mortgage rates. Over the last couple of years, they hit record lows, rose dramatically, and are now dropping back down a bit. Ever wonder why?

The answer is complicated because there’s a lot that can influence mortgage rates. Here are just a few of the most impactful factors at play.

Inflation and the Federal Reserve

The Federal Reserve (Fed) doesn’t directly determine mortgage rates. But the Fed does move the Federal Funds Rate up or down in response to what’s happening with inflation, the economy, employment rates, and more. As that happens, mortgage rates tend to respond. Business Insider explains:

“The Federal Reserve slows inflation by raising the federal funds rate, which can indirectly impact mortgages. High inflation and investor expectations of more Fed rate hikes can push mortgage rates up. If investors believe the Fed may cut rates and inflation is decelerating, mortgage rates will typically trend down.”

Over the last couple of years, the Fed raised the Federal Fund Rate to try to fight inflation and, as that happened, mortgage rates jumped up, too. Fortunately, the expert outlook for inflation and mortgage rates is that both should become more favorable over the course of the year. As Danielle Hale, Chief Economist at Realtor.com, says:

“[Mortgage rates will continue to ease in 2024 as inflation improves . . .”

There’s even talk the Fed may actually cut the Fed Funds Rate this year because inflation is cooling, even though it’s not yet back to their ideal target.

The 10-Year Treasury Yield

Additionally, mortgage companies look at the 10-Year Treasury Yield to decide how much interest to charge on home loans. If the yield goes up, mortgage rates usually go up, too. The opposite is also true. According to Investopedia:

“One frequently used government bond benchmark to which mortgage lenders often peg their interest rates is the 10-year Treasury bond yield.”

Historically, the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate has been fairly consistent, but that’s not the case recently. That means, there’s room for mortgage rates to come down. So, keeping an eye on which way the treasury yield is trending can give experts an idea of where mortgage rates may head next.

Bottom Line

With the Fed meets, experts in the industry will be keeping a close watch to see what they decide and what impact it’ll have on the economy.

The Federal Reserve held interest rates steady on Wednesday but signaled that rates could fall in the coming months if inflation continues to cool.

He cautioned, however, that the economy remains unpredictable and said the central bank would proceed cautiously. ”The economic outlook is uncertain and we remain highly attentive to inflation risks,” Powell said.

The Fed has been pleasantly surprised by the rapid drop in inflation in recent months. Core prices in December — which exclude food and energy prices — were up just 2.9% from a year ago, according to the Fed’s preferred inflation yardstick. That’s a smaller increase than the 3.2% core inflation rate that Fed officials had projected in December.

If that positive trend continues, the Fed may be able to start cutting interest rates as early as this spring. However, he sounded doubtful about a rate cut at the Fed’s next meeting in March as many investors in Wall Street had hoped for. The comments disappointed investors, with the Dow Jones Industrial Average tumbling 317 points.

Investors are still hopeful about a rate cut in May, with markets putting the likelihood of that at better than 90%.

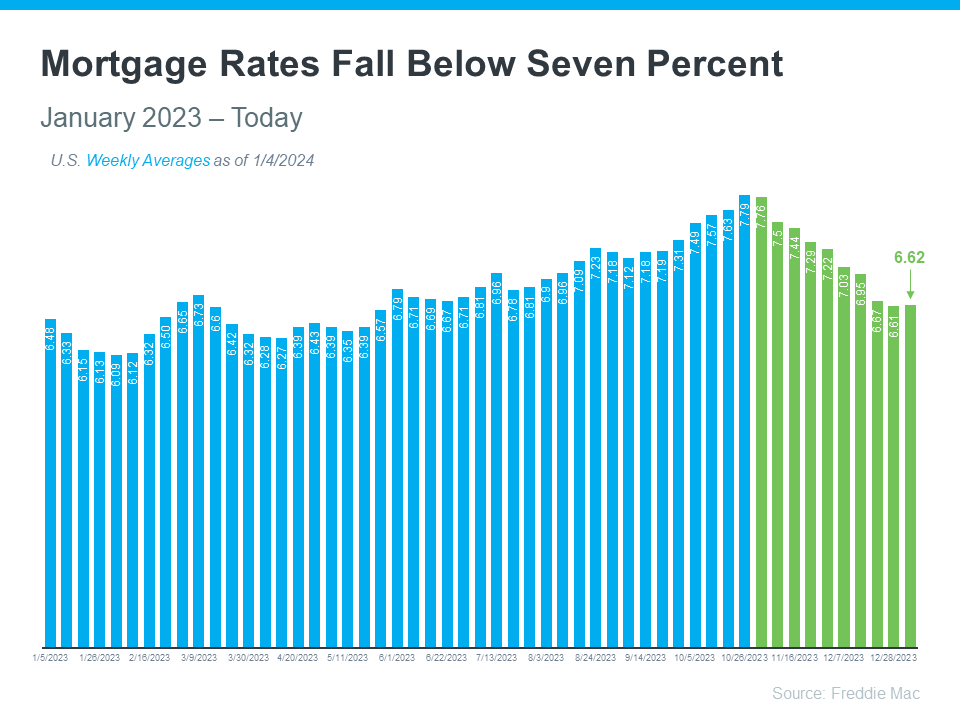

If you want to buy a home, it’s important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph below) and many analysts predict a continued easing of mortgages rates throughout 2024.

This recent trend is great news for buyers. As a recent article from Bankratesays:

“The rate cool-off somewhat eases the housing affordability squeeze.”

And according to Edward Seiler, AVP of Housing Economics and Executive Director of the Research Institute for Housing America at the Mortgage Bankers Association (MBA):

“MBA expects that affordability conditions will continue to improve as mortgage rates decline . . .”

Here’s a bit more context on how this could help with your plans to buy a home.

How Mortgage Rates Affect Your Search for a Home

Understanding the connection between mortgage rates and your monthly home payment is crucial for understanding the sales price you can afford. The chart below illustrates how your ability to afford a home changes when mortgage rates shift. (see chart below):

More information about interest rates at Freddie Mac

Sellers, including home builders, will sometimes use 2-1 buydowns as an incentive for potential purchasers

A 2-1 buydown is a concession or incentive negotiated with a seller or builder that temporarily reduces a buyer’s mortgage interest rate by 2 percentage points the first year and 1 percentage point the second year of your mortgage. The third year the interest rate goes back to the fixed rate obtained from the lender.

A 2-1 buydown is a type of financing that lowers the interest rate on a mortgage for the first two years before it rises to the regular, permanent rate.

The rate is typically two percentage points lower during the first year and one percentage point lower in the second year.

Sellers, including home builders, may offer a 2-1 buydown to make a property more attractive to buyers.

2-1 buydowns can be a good deal for homebuyers, provided that they will be able to afford the higher monthly payments once those begin.

Lenders charge an additional fee to make up for the interest that they won’t be receiving in those early years. A homebuyer or seller can pay for a buydown. That payment may be in the form of mortgage points, or a lump sum deposited in an escrow account with the lender and used to subsidize the borrower’s reduced monthly payments.

The 2-1 buydown is sometimes offered as an incentive and sometimes it is part of the buyer’s negotiations.

Example

Suppose a new home builder is offering a 2-1 buydown on its new homes. If the prevailing interest rate on 30-year mortgages is 6% for a particular buyer, this homebuyer could get a mortgage that charged just 4% in the first year, then 5% in the second year, and 6% starting in year three and continuing through the remaining years. The reduced payments in those first two years can result in substantial savings.

The good news is, many experts are optimistic we’ve turned a corner and are headed in a positive direction.

Mortgage Rates Expected To Ease

Recently, mortgage rates have started to come back down. This has offered hope to buyers dealing with affordability challenges. Mark Fleming, Chief Economist at First American, explains how they may continue to drop:

“Mortgage rates have already retreated from recent peaks near 8 percent and may fall further . . .”

Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), says:

“For home buyers who are taking on a mortgage to purchase a home and have been wary of the autumn rise in mortgage rates, the market is turning more favorable, and there should be optimism entering 2024 for a better market.”

The Supply of Homes for Sale May Grow

As rates ease, activity in the housing market should pick up because more buyers and sellers who had been holding off will jump back into action. If more sellers list, the supply of homes for sale will grow – a trend we’ve already started to see this year. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Supply will loosen up in 2024. Even homeowners who have been characterized as being ‘locked in’ to low rates will increasingly find that changing family and financial circumstances will lead to more moves and more new listings over the course of the year, particularly as rates move closer to 6.5%.”

Home Price Growth Should Moderate

And mortgage rates pulling back isn’t the only positive sign for affordability. Home price growth is expected to moderate too, as inventory improves but is still low overall.As the Home Price Expectation Survey (HPES) from Fannie Mae, a survey of over 100 economists, investment strategists, and housing market analysts,says:

“On average, the panel anticipates home price growth to clock in at 5.9% in 2023, to be followed by slower growth in 2024 and 2025 of 2.4 percent and 2.7 percent, respectively.”

To wrap it up, experts project 2024 will be a better year for the housing market. So, if you’re thinking about making a move next year, know that early signs show we’re turning a corner. As Mike Simonsen, President and Founder of Altos Research, puts it:

“We’re going into 2024 with slight home-price gains, somewhat easing inventory constraints, slightly increasing transaction volume . . . All in all, things are looking up for the U.S. housing market in 2024.”

Bottom Line

Experts are optimistic about what 2024 holds for the housing market. If you’re looking to buy or sell a home in the new year, I would love to help!

The Federal Open Markets Committee (FOMC) held its short-term policy interest rate steady at its last meeting of the year on Wednesday (12-13-23). It was the fourth pause recorded in 2023.

Federal Reserve Chairman Jerome Powell said that while inflation remains ‘elevated,’ the Fed anticipates making three 25 basis point rate cuts in 2024, a signal to Investors that hikes are over and this news is already causing some reduction in rates.

The bond market responded in kind, with the 10-year Treasury yield falling to 4.0% late afternoon on Wednesday, its lowest level since late July.

Mike Fratantoni, the chief economist of the Mortgage Bankers Association, stated. “This is good news for the housing and mortgage markets. We expect that this path for monetary policy should support further declines in mortgage rates, just in time for the spring housing market. We are forecasting modest growth in new and existing home sales in 2024, supporting growth in purchase originations, following an extraordinarily slow 2023.”

In 2023, the Fed hiked the benchmark federal funds rate by a quarter-point at four meetings, most recently in July.

Rate relief in 2024

“The Fed’s projections for 2024 will continue to anticipate a normalization in monetary policy in the year ahead,” said Realtor.com Chief Economist Danielle Hale.

Hale has forecast mortgage rates to ease further in 2024 as inflation improves and Fed rate cuts draw closer.

“Mortgage rates could near 6.5% by the end of the year, a key factor in starting to provide affordability relief to homebuyers,” Hale said.

Among the first customers to benefit from reduced interest rates would be those who are currently making payments on mortgages with high rates.

According to TransUnion data, since January 2021, there have been 3 million new mortgages originated with interest rates of 6% of higher, the total balance of which being over $1 Trillion. The monthly payments of each of these high interest mortgages averages $2,201.

If interest rates dropped to even 5.5%, it could result in significant savings for homeowners, as refinancing at that rate could result in an average monthly payment of $1,917 for them, a reduction of $284 every month, said Michele Raneri, VP of U.S. research and consulting at TransUnion. “This would represent nearly $300 a month that these homeowners would be able to use elsewhere in this continued high cost-of-living environment in which every dollar counts.”

The 30-year fixed-rate mortgage (FRM) decreased for the sixth straight week, from last week to an average of 7.03% this week, according to the latest Primary Mortgage Market Survey® (PMMS®) from Freddie Mac released Thursday.

This week’s numbers:

30-year fixed-rate mortgage averaged 7.03%, down from last week when it averaged 7.22%. A year ago at this time, the 30-year FRM averaged 6.33%.

15-year fixed-rate mortgage averaged 6.29%, down from last week when it averaged 6.56%. A year ago at this time, the 15-year FRM averaged 5.67%.

Realtor.com Economist Jiayi Xu commented: “The Freddie Mac fixed rate for a 30-year mortgage continued its downward trend to 7.03 percent this week, down from 7.22 percent last week. While Fed Chair Powell stated last Friday that it was too early to conclude that the current monetary policy is restrictive enough to tame inflation down to the 2% target, the cooling October job openings data, a measure of labor demand, released on Tuesday, boosted investors’ confidence that the Federal Reserve was probably done with rate hikes. As a result, the 10-year treasury yield dropped to its lowest level in three months. Looking ahead, we predict that sustained improvement in inflation will bring the mortgage rate down to 6.5% by the end of 2024.