Seasonal Flow of Business Returns. We seem to have exited the “pandemic years” when real estate was busy at all points in the year and we have returned to a more normal seasonal flow of business as shown in the chart below. All three lines (2022, 2023, and the 15 year average) track each other closely throughout the year. The orange line represents ratified contracts by week 2022, the green line is 2023 and the blue line is the 15-year average for each week.

As inventory was still constrained and interest rates begin retreating, written sales market wide finished -7% in December of ’23 versus December of ‘22

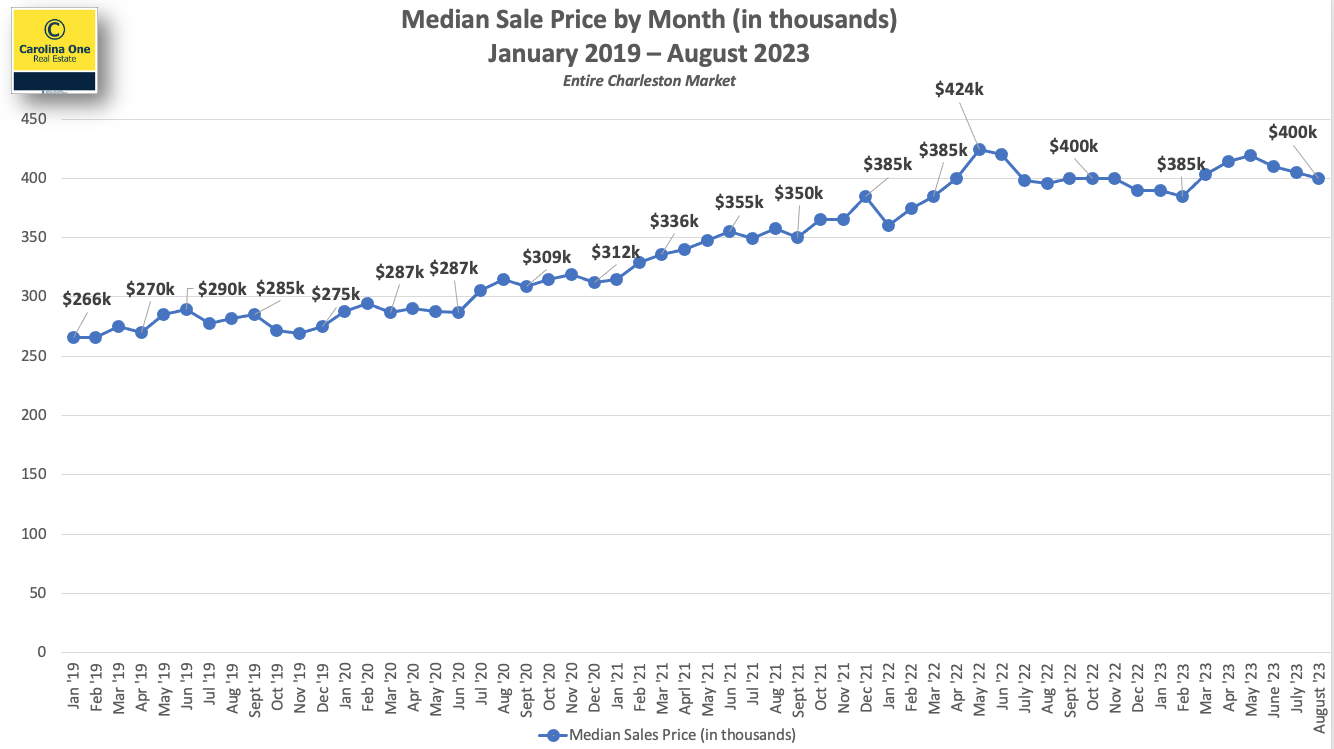

The Median sale price in the Charleston MLS continues to stay in a tight band between $400k and $420k where it has been for most of the last 20 months.

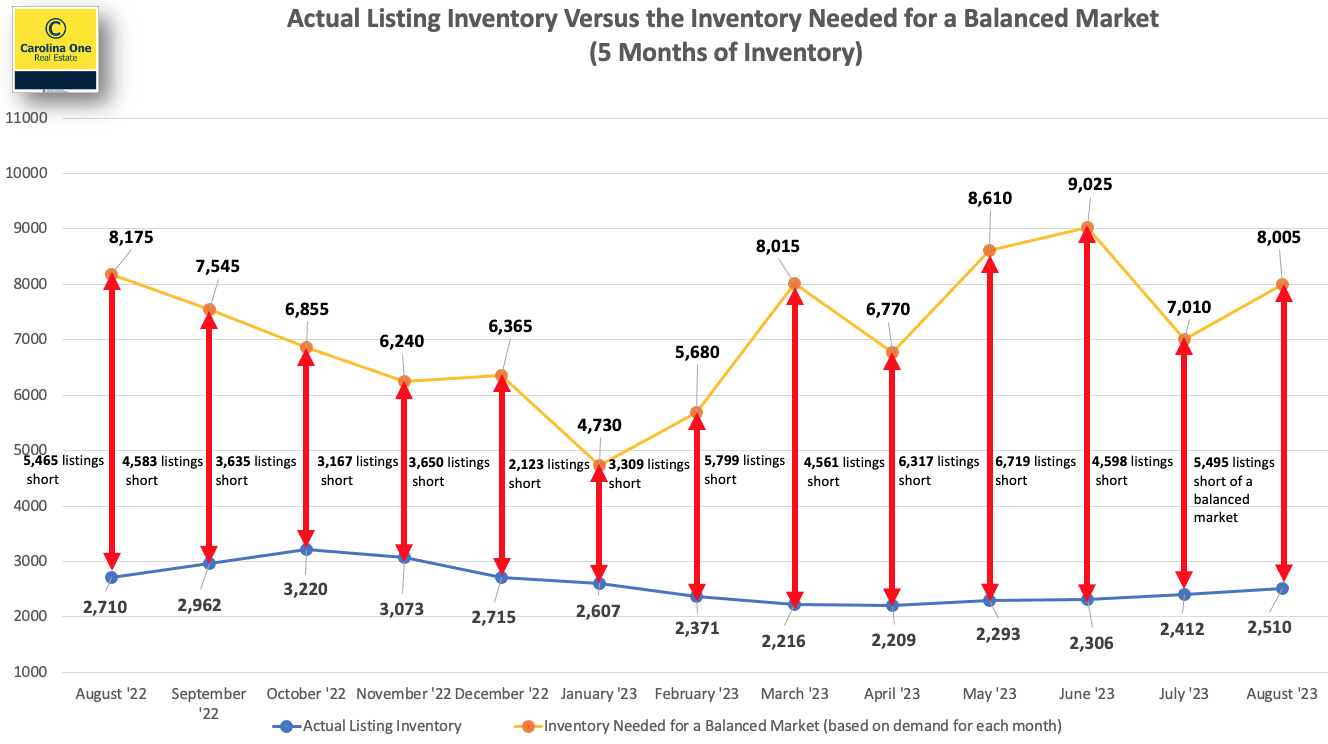

Inventory remained below what is needed for a balanced market throughout 2023. At end of December active Inventory stood at approximately 2,800 listings. This level of inventory is a significant increase over the 1,035 listing “floor” that we set in February of 2022, but still below what is needed for a balanced market. 3,000 additional listings are needed market wide to achieve a balanced market (5 months of inventory)

The gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is expressed visually in the chart below.

The Good News` – Although inventory is still constrained, we are starting to see a trend of new listings hitting the market increasing over the same month a year prior for the first time in two years. This has happened for three consecutive months.

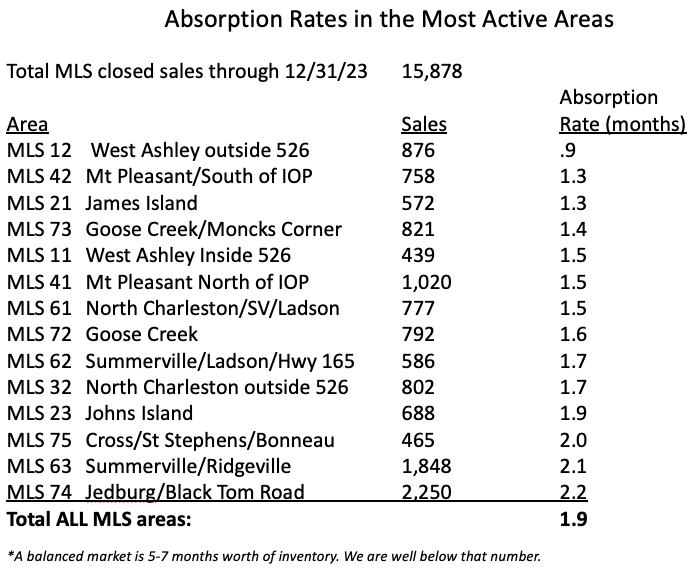

Absorption Rate By the end of the 2023, The Charleston market had about eight weeks of inventory as a whole, still trending more toward a seller’s market (this can vary by pricerange and specific location). The most active areas have inventory levels in the 5–9-week range.

NewConstruction At December’s end, new construction represented approximately 49% of pending contracts in the MLS and new construction comprised about 33% of the closings and new homes represented approximately 32% of the available inventory.

Sellers, including home builders, will sometimes use 2-1 buydowns as an incentive for potential purchasers

A 2-1 buydown is a concession or incentive negotiated with a seller or builder that temporarily reduces a buyer’s mortgage interest rate by 2 percentage points the first year and 1 percentage point the second year of your mortgage. The third year the interest rate goes back to the fixed rate obtained from the lender.

A 2-1 buydown is a type of financing that lowers the interest rate on a mortgage for the first two years before it rises to the regular, permanent rate.

The rate is typically two percentage points lower during the first year and one percentage point lower in the second year.

Sellers, including home builders, may offer a 2-1 buydown to make a property more attractive to buyers.

2-1 buydowns can be a good deal for homebuyers, provided that they will be able to afford the higher monthly payments once those begin.

Lenders charge an additional fee to make up for the interest that they won’t be receiving in those early years. A homebuyer or seller can pay for a buydown. That payment may be in the form of mortgage points, or a lump sum deposited in an escrow account with the lender and used to subsidize the borrower’s reduced monthly payments.

The 2-1 buydown is sometimes offered as an incentive and sometimes it is part of the buyer’s negotiations.

Example

Suppose a new home builder is offering a 2-1 buydown on its new homes. If the prevailing interest rate on 30-year mortgages is 6% for a particular buyer, this homebuyer could get a mortgage that charged just 4% in the first year, then 5% in the second year, and 6% starting in year three and continuing through the remaining years. The reduced payments in those first two years can result in substantial savings.

The good news is, many experts are optimistic we’ve turned a corner and are headed in a positive direction.

Mortgage Rates Expected To Ease

Recently, mortgage rates have started to come back down. This has offered hope to buyers dealing with affordability challenges. Mark Fleming, Chief Economist at First American, explains how they may continue to drop:

“Mortgage rates have already retreated from recent peaks near 8 percent and may fall further . . .”

Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), says:

“For home buyers who are taking on a mortgage to purchase a home and have been wary of the autumn rise in mortgage rates, the market is turning more favorable, and there should be optimism entering 2024 for a better market.”

The Supply of Homes for Sale May Grow

As rates ease, activity in the housing market should pick up because more buyers and sellers who had been holding off will jump back into action. If more sellers list, the supply of homes for sale will grow – a trend we’ve already started to see this year. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Supply will loosen up in 2024. Even homeowners who have been characterized as being ‘locked in’ to low rates will increasingly find that changing family and financial circumstances will lead to more moves and more new listings over the course of the year, particularly as rates move closer to 6.5%.”

Home Price Growth Should Moderate

And mortgage rates pulling back isn’t the only positive sign for affordability. Home price growth is expected to moderate too, as inventory improves but is still low overall.As the Home Price Expectation Survey (HPES) from Fannie Mae, a survey of over 100 economists, investment strategists, and housing market analysts,says:

“On average, the panel anticipates home price growth to clock in at 5.9% in 2023, to be followed by slower growth in 2024 and 2025 of 2.4 percent and 2.7 percent, respectively.”

To wrap it up, experts project 2024 will be a better year for the housing market. So, if you’re thinking about making a move next year, know that early signs show we’re turning a corner. As Mike Simonsen, President and Founder of Altos Research, puts it:

“We’re going into 2024 with slight home-price gains, somewhat easing inventory constraints, slightly increasing transaction volume . . . All in all, things are looking up for the U.S. housing market in 2024.”

Bottom Line

Experts are optimistic about what 2024 holds for the housing market. If you’re looking to buy or sell a home in the new year, I would love to help!

Mortgage rates dropped significantly in the last few weeks.

The 30-year, fixed mortgage rate averaged 7.29% for the week ending Nov. 22, according to Freddie Mac‘s Primary Mortgage Market Survey. That’s down significantly from last week’s 7.44% and up from 6.58% the same week a year ago.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s average 30-year fixed rate on conventional loans at 7.283% on Wednesday.

Mortgage applications rose to their highest level in six weeks after the 30-year fixed mortgage rate fell last week.

Mortgage rates for the 30-year fixed loan averaged 7.44%, falling 6 basis points in one week, according to Freddie Mac‘s Primary Mortgage Market Survey.

On a seasonally adjusted basis, purchase applications rose by nearly 4% over the week, with increases in both conventional and government purchase loan demand.

The average loan size on a purchase application was $403,600, the lowest since January 2023. Joel Kan, MBA’s vice president and deputy chief economist, said this corroborates with other sources of home-sales data pointing to a rising share of first-time homebuyers entering the market.

Meanwhile, refinance applications rose slightly by 1.6% last week but remained subdued. The adjustable-rate mortgage (ARM) share of activity fell to 8.3% of total applications, down from 8.8% the previous week.

The share of Federal Housing Administration (FHA) loan activity increased to 14.8% of all applications, down from 14.4% the week prior. The share of Department of Veterans Affairs(VA) loan activity was 11.3%, up from 11.2% over the previous week, while the share of U.S. Department of Agriculture (USDA) loan activity fell to 0.4% from 0.5% week over week.

After already falling for two days, 30-year mortgage rates plummeted Thursday, shedding another two-tenths of a point. That drops the 30-year average to 7.92%, its cheapest level since September. Rates were down by double-digit basis points for almost every other loan type as well.

Since rates vary widely across lenders, it’s always smart to shop around for and compare rates regularly, no matter what type of loan you’re seeking.

(1) Written sales market wide finished 13% less in August of ’23 versus August of ’22.

It was anticipated that sales would be -15% for the year (versus 2022) with the first half of the year being much worse than -15% and the back half of the year being better than -15%

Based on interest rates remaining stubbornly and persistently high, we are now anticipating that the second half of the year will be similar to the first half of the year with sales in the -15% year-over-year range

(2) Last week saw 239 properties go under contract, a very “normal” number for this time of year but far below the “juiced up” pandemic years of 2020 and 2021. Sales (green line) have remained remarkably close to the 15 year average (blue line) for about three and a half months.

The orange line represents ratified contracts by week last year…the green line is this year…and the blue line is the 15 year average for each week.

(3) Mortgage rates remaining elevated is holding back sales.

4) The Median sale price in the Charleston market continues to stay in a tight band between $400k and $420k where it has been for most of the last 16 months.

(5) Active Inventory stands at 2,510 listings. We haven’t seen much inventory growth this summer and inventory typically starts a slow seasonal decline in September or October. It is believed this may likely put upward pressure on prices, or at the very least hold prices steady.

While this level of inventory is a significant increase over the 1,035 listing “floor” that we set in February of 2022:

Roughly an additional 5,500 listings is needed market wide to achieve a balanced market (5 months of inventory)

The gap between the number of listings available for sale and the number of listings needed to maintain a balanced market is substantial. The chart below is an attempt to express this visually.

(6) The number of new listings taken in August was even with the same month a year prior for the first time in two years, but inventory still remains low.

7) The Charleston market has about six or seven weeks of inventory as a whole, still solidly a seller’s market (this can vary by price range and specific location). The most active areas have inventory levels in the 3-6 week range.

(8) New construction represents 46% of all pending contracts in the MLS and new construction comprises about 32% of the closings.

New Homes “pendings” will always be higher than new homes closings as new construction typically sits in pending status for far longer than a resale, and the new homes tend to “pile up” in pending status, so new homes actually represent about 32% of the sales market currently

New homes represent 33% of the available inventory, currently.

(9) Foreclosures and Short Sales continue to hold at a combined .6% of all available listings currently. This is down from 1.8% of all available listings on 1/1/2020. This market has very few “newly distressed” properties in the pipeline.

“Serious delinquencies fell to the lowest level since August 2006; the July delinquency rate was negligibly higher than the lowest level ever recorded.” – Black Knight Mortgage Monitor statement from two weeks ago.

Record home equity is driving the low delinquency rate along with high levels of employment.

(10)We are at roughly double the monthly pre-pandemic sales levels of $1MM+ properties. This market segment remains surprisingly robust.

Home Swap is a loan program designed to help current homeowners buy a new home without having to sell their existing home first. It functions similar to a traditional bridge loan, which is a short-term loan that people can use in the lead up to securing long-term financing. Instead of having to sell first and then find temporary housing while searching for a new home to buy (or worse, take on two mortgages), homeowners get the flexibility to close on their new home and then go through the process of selling. That means no double mortgages and no juggling timelines to try and minimize the period in between closings.

How does Knock Home Swap work?

The Home Swap program works like this:

Homeowners get pre-approved and fully underwritten for a homebuying loan with Knock, the company behind Home Swap. Secured at a convenience fee of 1.25% of the new home’s purchase price, the loan also includes a down payment advance. (Home Swap users can pay that 1.25% can at closing or roll it into what they borrow.)

When they find the home they want to buy, the purchasers put in their offer without a sales contingency—meaning they do not have to sell their previous home to close. Upon move-in, they’ll start making payments on their new mortgage while a Knock Equity Advance covers payments on their old mortgage for up to six months.

While settling into their new home, the homeowners will list their old home for sale. If they need to make any improvements before the sale, they can take out up to $25,000 in Home Swap loans for the job.

Homeowners sell their old homes using a real estate agent of their choice. Suppose the home doesn’t sell on the open market within the six months that mortgage payments are being fronted through Home Swap. In that case, homeowners have the option to sell their home directly to Knock for a pre-determined offer—usually about 80% to 85% of fair market value for the property.

Just like with a standard home loan, Knock sells your loan after you close, and you’ll make your mortgage payments to the company that buys it. Payment for the Home Swap loan is a 1.25% convenience fee.

What are the benefits of using Home Swap?

The biggest benefit is that homeowners do not have to sell their current home before buying their new one. This is a huge advantage since most people don’t have the financial flexibility to take on the risk of paying two mortgages at the same time. Of course, you’re still paying for your first mortgage with Home Swap, but it’s rolled into the amount that you borrow so that you won’t be cutting two checks every month.

Another major benefit is that buyers can avoid a sale contingency.

Home Swap vs. traditional lending

Keep in mind that with convenience comes fees, so you’ll pay extra for it through that set 1.25% convenience fee, which may be more than the origination fee you would have secured on a traditional loan.

What’s the same?

Closing costs

You’ll still owe all normal closing costs if you go with Home Swap, including title-related fees, attorney fees, and lending fees. The one difference here is that if you go with Home Swap, you’ll also owe a 1.25% convenience fee; however that can roll into your mortgage if you don’t want to pay it at closing.

Varying rates

As with any home loan, your rates will still depend on your qualifications. The better your credit and the less risky of a borrower you are, the better terms you’ll get on your loan, whether that’s with Home Swap or with another lender.

Flexible housing options

Like with any home loan, you can use Home Swap to buy and sell various housing types. Condos, townhomes, and new construction are all eligible and will not preclude you from getting financing.

What’s different?

Non-contingent financing

So long as your qualifying information doesn’t change between when you’re approved and when you close, you’re guaranteed cash-backed, non-contingent financing with a Home Swap loan. This gives the seller 100% assurance that financing will come through on closing day, regardless of whether your other home is sold.

No-sale contingencies are possible with traditional lending, but because they’re risky for lenders, you’ll need to have the cash to support them. Home equity loans, bridge loans, or savings are ways to do it, but they’ll exist separately from your new mortgage.

Market availability – (AVAILBLE IN SC)

Other options for buying and selling a house at the same time

Home Swap is a nice option for buyers who also need to sell, but it’s not the only one. If you’re in the market to buy and sell at the same time, here are some of the other ways that you can finance the move.

Home Equity Line of Credit (HELOC)

A HELOC is a loan that allows homeowners to borrow up to the amount of equity in their current home. The longer you’ve lived in your current home, the more equity you’ll have in it—and the more you’ll be able to borrow with a HELOC.

HELOCs are sort of like credit cards in that you have a set limit to the loan (your equity balance), and you can take out what you need when you need it. To buy a new home, however, you can go ahead and take out as much of the limit as you need and then put that toward your purchase.

Note that while a standard HELOC repayment period is about 20 years, you have to pay back the loan in full before you close on a sale of the property. That shouldn’t be an issue as long as you can sell your home for at least as much as your mortgage is currently worth.

Bridge loan

Home Swap is an example of a bridge loan, a short-term loan that you can take out to “bridge” the period between buying a new home and selling your old one. A standard bridge loan (also known as a swing loan or gap financing) won’t come with the additional perks of Home Swap, but it could still be a good choice depending on your circumstances.

Like a HELOC, you’ll borrow against your home’s equity with a bridge loan. Unlike a HELOC, you don’t have an extended repayment period that can hold you over if your home doesn’t sell right away. Bridge loan repayment periods usually start after 12 months, at which point you’d be responsible for paying back the loan and paying the mortgage on your new home, provided you weren’t able to sell.

The benefits to a bridge loan are the flexibility it affords and that it gives you the ability to put down a non-contingent offer and, potentially, a higher down payment as well. Drawbacks include the aforementioned short repayment period, high interest rates, and additional closing costs.

Information from Knock.com

If you would like to explore buying a new home and selling your current home, I would love to help!

Tucked away in The Hamlets of Crowfield Plantation, is a rare property that offers privacy and tranquility in a desirable community with easy access to all that the Low Country has to offer!

This Luxury property has a private security gate, 7795 sqft, 7 Bedrooms, 8 Bathrooms, A State-Of-The Art Movie Theatre, A 6 Car Garage, A Separate Apartment, One Acre Lot, Golf Course and Pond Views, and so much more!

Nestled in the heart of Goose Creek, South Carolina, lies a community that exudes elegance, charm and character. Known as Crowfield Plantation, this stunning residential community has earned the reputation as a hidden gem within the Charleston metro area.

The development of Crowfield began in the early 1990’s and was built on a historic site.

The neighborhood’s peaceful environment offers an escape from the hustle and bustle of everyday life, as well as a welcome retreat from the busier parts of the Lowcountry. The community consists of residential and commercial parcels and offers a variety of housing types and price-ranges.

Today, Crowfield Plantation offers its residents a myriad of recreational and entertainment options. Its scenic lake, ponds and walking trails are a popular spot for runners and walkers alike, and the community pools, parks, clubhouse and tennis courts provide endless opportunities for leisure activities. The Crowfield golf course is located in The Hamlets of Crowfield Plantation which is a great feature for avid golfers and visitors alike. VIEW ALL HOMES AVAILABLE FOR SALE IN CROWFIELD

With easy access to Interstate 26 and a location that’s close to local attractions, Charleston and Summerville, Crowfield Plantation residents have plenty of shopping and dining options. There are also several public schools located nearby.

But perhaps what sets Crowfield Plantation apart from other residential communities is the true sense of community and it’s serene environment. Crowfield’s immense greenspace, tree-filled buffers, lakes, ponds and playgrounds along with community events. create a true sense of camaraderie, tranquility and belonging.

So if you’re looking for a peaceful escape that offers a strong sense of community and a wealth of recreational opportunities, consider Crowfield Plantation as your next home.