The National Association of REALTORS® unveiled the top 10 homebuying hot spots for 2026 in a new report, Housing Hot Spots for 2026: The Markets Poised for New Buyer Opportunities. Charleston was among the selected. These top 10 housing hot spots consist of markets that outperform the average market in the U.S. on at least five of 10 economic, demographic, and housing indicators, have populations above 250,000, and demonstrate meaningful 2026 opportunities for homebuyers.

NAR senior economist Nadia Evangelou stated that, “Charleston is a metro that stands out from the crowd”. The city’s inventory is growing at the right price points, offering would-be buyers’ greater affordability than many other locations.

Population growth in the metro remains among the fastest in the area, fueled by both millennial households and high-income transplants from the Northeast. Additionally, income growth in Charleston is 6% year over year, while job growth is up 3.2% compared to 2024.

Covenants, Conditions, and Restrictions (CCRs) are legal documents in real estate, common in planned communities and subdivisions. These recorded rules govern land use and development, establishing a framework for how properties within a specific area can be utilized. CCRs maintain community standards and can help preserve property value to ensure individual property use aligns with the neighborhood’s collective vision.

“Covenants” are promises by property owners to perform or refrain from specific actions, such as maintaining a home’s exterior or adhering to landscaping guidelines. “Conditions” are requirements for property ownership, often relating to improvements or obtaining approval for changes. “Restrictions” impose limitations on property use, which might include prohibitions on commercial activities or specific vehicle parking.

Common CCR’s

CCRs include rules and regulations for community standards. Architectural guidelines cover things like exterior paint colors, fencing materials, and home additions. Landscaping rules focus on lawn care, tree removal, and approved plant types. Pet restrictions might limit the number, size, or breed of animals and often include waste disposal requirements.

Parking rules may govern where vehicles can be parked, prohibit oversized vehicles or limit street parking. Limitations on property use, such as commercial businesses from operating from a residence or restricting short-term rentals could also be included in CCR’s.

Establishment and Enforcement

CCRs come into existence through a formal process, typically initiated by the developer of a planned community or subdivision. These documents are legally recorded with the county recorder’s office, making them part of the public record and binding on all current and future property owners within that community. This recording ensures that the rules “run with the land,” meaning they apply to the property itself, regardless of who owns it.

The Homeowners Association (HOA) may play a central role in enforcing CCRs once the community is established. Enforcement mechanisms vary but commonly include issuing warnings for minor infractions. For continued non-compliance, HOAs can levy fines, which may be assessed periodically until the violation is resolved. In more serious cases, an HOA might place a lien on the property for unpaid fines or assessments. Legal action, such as a lawsuit to compel compliance or recover damages, is another enforcement tool available to some HOAs.

Some governing documents may have a provision to amend the CCR’s, such as a vote of the majority of the members, but rules can vary.

Prospective buyers should review a property’s CCRs to understand their rights and obligations.

For communities without an HOA, CCRs might still be recorded, enforcement may be handled by a local municipality.

Homebuyers will soon have an added layer of protection when shopping around for a mortgage due to the new Homebuyers Privacy Protection Act. The new law is designed to prohibit the abuse of what’s known as trigger leads, which are when credit bureaus sell a borrower’s information immediately after a mortgage credit inquiry. The law makes it illegal for credit bureaus to do so without consumers’ consent.

“This new law is a major victory for mortgage borrowers that will protect them from the barrage of unwanted calls, texts, and emails they too often received immediately after applying for a mortgage,” said Mortgage Bankers Association President and CEO Bob Broeksmit. “It will create a more efficient, responsible, and respectful homebuying process when it goes into effect on March 5, 2026.”

The average sale price is determined by totaling all the sale prices of homes sold in a specific area over a set time period and dividing by the number of properties sold. However, if a property or two sells at an unusually high or low price, it can distort the average, making it an unreliable metric in certain situations. The median sale price is the price right in the middle of a dataset. It shows the point where half the properties in an area sell for more and the other half sell for less. This figure is a reliable way to track market trends over time.

Average and median sales prices are both useful methods for analyzing data, but they serve different purposes.

SC State Housing offers a variety of mortgage financing options through a variety of Lending Partners to make owning a home more affordable and recent changes will allow more buyers to qualify.

One of the most substantial changes allows the applicant / buyer to use only his/her income for qualification purposes. This change will allow more buyers to fall under the income limits to help them qualify for the program. Previously, the total household income had to be under the income limit to qualify.

The current bond issue offers a lower than market rate and $10.000 down payment assistance. The rules for “targeted” areas allow buyers to purchase their primary residence but they cannot own another property at the time of closing. However, buyers can sell their current home prior to purchasing the new home and still use the program as long as they meet all other guidelines.

For “non-targeted areas, purchasers may not have owned a home within 3 years of closing the new home

There are a variety of affordable SC Housing programs with different criteria and the much-anticipated Palmetto Heroes Program will be available this spring (date and details have not been announced yet). Palmetto Heroes serves military, police, fire and medical personal and typically has a generous down payment assistance amount and a lower-than-market rate.

If you or someone you know could benefit from a State Housing program, please contact me, I would be happy to help connect you with the needed resources.

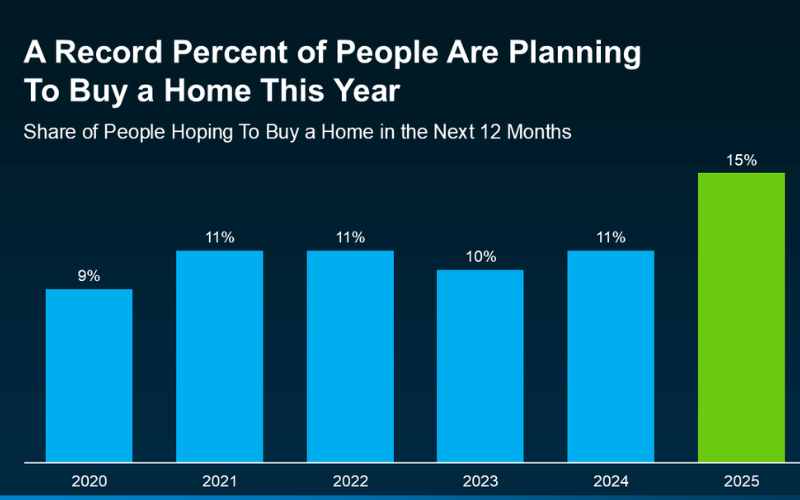

According to a recent NerdWallet survey, 15% of Americans are planning to purchase a home this year. That’s actually a record high for this survey (see graph below):

The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening but does indicate that buyers are optimistic. Whether they’re feeling more confident about moving, or saved money, or simply can’t wait any longer – this seems to be the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring.

In today’s market, more and more home buyers are getting assistance with their down payment in the form of gift funds from friends and family. According to a recent study, in 2023, 39% of home buyers who financed their home with a mortgage loan used gifted funds as at least one source for their down payment, up nine percentage points from 2018. While it’s great to have help, there are rules around financial gifts that you need to know in order to smoothly navigate the process.

What is a down payment gift?

Down payment money is considered a “gift” when people, usually friends or family, financially contribute money that will help the home buyer pay for a down payment on a home. there is generally no limit on how much a borrower is allowed to receive as a gift

Who is eligible to Gift you down payment money?

Depending on the loan type, gifts can come from the buyer’s relative, employer, or close friend with a “clearly defined and documented” interest in the borrower, or a charitable organization, governmental agency, or a public entity that has a program providing home ownership assistance for low and moderate-income families or first-time home buyers. However, donations for down payments cannot come from people who are directly affiliated with the home buying transaction which includes builders, developers, or real estate agents.

What are the rules for mortgage down payments?

For Fannie Mae backed loans, a minimum borrower contribution from the borrower’s own funds is not required. This means that 100% of the money that is needed to make up the down payment can come from a gift. On the other hand, with FHA loans, the borrower is required to provide a minimum personal cash investment of at least 3.5% for the down payment. regardless of the loan type, gift funds must be a “bona fide gift,” and not a loan that requires repayment.

While there is no limit to how much money you can accept as a gift for a home down payment, when you’re going through the mortgage loan application process, you’ll need to make sure that you have proper documentation of the gift money in the form of a letter, with specific requirements outlined by your lender, from the donor of the funds. this is required to show your letter that you don’t owe someone a large sum of money that you won’t be able to pay back on top of your monthly mortgage payment.

An accessory dwelling unit (ADU), sometimes called a carriage house or in-law suite, is a separate, detached living space with a kitchen, bathroom and sleeping area on the same property as a single-family home.

As the cost of housing continues to rise, local leaders are looking to allow these accessory dwelling units in residential areas to provide more housing options.

Leaders in the local government of North Charleston recently proposed a new ordinance that would allow homeowners to rent the separate unit to a long-term tenant, which would provide additional income to the homeowner and increase housing stock.

North Charleston currently allows ADUs in a few overlay districts, such as the Olde North Charleston Historic District and Neighborhood Conservation District, which covers a strip of Park Circle between Spruill and Virginia avenues. The new ordinance is aimed at areas like Park Circle where larger lot sizes can accommodate additional density, as opposed to already dense areas like Liberty Hill, Chicora-Cherokee and Accabee.

According to the proposed ordinance, an ADU cannot be more than two-thirds the size of the principal dwelling unit or exceed 800 square feet. The lot size must be at least 4,500 square feet. An additional off-street parking spot for the ADU must be provided. All ADUs must be permitted by the city.

It’s intentional that these additional units are small, said Tim Macholl, the city’s director of planning and zoning, during a November committee meeting. He said the space is ideal for a college student who is spending the summer at home or in-laws staying in town. It also provides an opportunity for additional income for homeowners if they choose to rent it out, he added. However, these units are not eligible for short-term rental permits, so they can not be used for vacation rental services, like Airbnb.

The demand for ADU’s is on the rise. They offer some affordable housing solutions, an option for multi-generational living and versatility of home space as they can be used as home offices, living spaces or possibly rentals.

Goose Creek also has previsions in their ordinance for ADU’s and many other municipalities are incorporating guidelines as well to accommodate the ADU trend.

If you are considering an ADU, check with your local municipality and Homeowner Association to make sure they are allowed and to obtain the guidelines, rules and permitting requirements.

The National Association of Realtor’s economists recently weighed in on home sales, mortgage rates, the economy and changing buyer demographics and its effect on real estate for the year ahead.

Lawrence Yun, chief economist of the National Association of REALTORS®, along with NAR’s Deputy Chief Economist, Jessica Lautz, shared data and forecasts..

Their updated estimates show that the housing market is still dramatically undersupplied, and they estimate that U.S. housing stock is 3.7 million units below what is needed.

High mortgage rates and rising home prices have put a damper on affordability and are directly related to the supply shortage. Building more houses is essential but builders are also contending with high interest rates.

There is no silver bullet to alleviating this ongoing shortage but there are options being considered such as, accessory dwelling units (ADUs), Community Land Trusts, condominium conversions, and manufactured homes. They will continue to study this topic and work to uncover potential solutions.

Yun released a rosier forecast for the housing market for 2025 and 2026, with an outlook for higher home sales and moderating mortgage rates.

Here’s an overview of NAR’s predictions on key housing indicators for the year ahead.

Home Sales to Rise

With improving job numbers and recent gains in the stock market, more Americans may be motivated to act, Yun said.

Here’s Yun’s forecast over the next two years:

2025 sales projection: Existing home sales to rise 9% year-over-year; New home sales to jump by 11%.

2026 sales projection: Existing-home sales to rise 13% year-over-year; new home sales to increase by 8%.

Mortgage Rates to Moderate

The trajectory of mortgage rates will have a major bearing on how the housing market will fare, Yun said.

Mortgage rates may moderate but buyers may not see that anytime soon, Yun said. “Mortgage rates will not decline in tandem”… “With a large budget deficit, there’s less mortgage money available…. A large budget deficit will prevent mortgage rates from going down to 4%”

Nevertheless, the “locked-in” effect of homeowners feeling stuck-in-place with low 2% or 3% mortgage rates from recent years will lessen over time, as personal milestones (births, deaths, marriages, graduations, new jobs,etc.) trigger real estate moves.

Home Prices Increases Slowly After Rapid Rises

While homeowners have enjoyed record-breaking equity gains, home buyers’ have been struggling with affordability. A typical homeowner has accumulated $147,000 in housing wealth just over the last five years, according to NAR’s research. As a result, the spread in median net worth between homeowners and renters continues to grow. It stands at $415,000 for homeowners versus $10,000 for renters, Yun said.

“The strong price increases cannot be sustainable for another five years, or America will be divided … with only a few getting to experience the tremendous housing wealth,” Yun said. “If we bring more supply to the housing market, home price increases will not be as outrageous … and will be more in line with wages.”

Yun’s forecast:

2025 median home price: $410,700; up 2% over 2024.

2026 median home price: $420,000, up 2% over 2025.

A Different Type of Buyer Emerges

The profile of home buyers are changing, Lautz said, presenting data from NAR’s newly released 2024 Profile of Home Buyers and Sellers. Here’s a few of the changes observed in the report:

More buyers are skipping the mortgage. all-cash buyers have surged to record highs, accounting for 26% of home sales over the past year. Thirty-one percent of repeat buyers paid all-cash for their next home purchase.

First-time buyers are getting older. The median age of a first-time home buyer was 38, an all-time high. Twenty-five percent of first-time buyers used a gift or loan from a relative or friend for their home purchase; 20% took money out of financial assets like stocks, 401ks or cryptocurrency to afford homeownership; and 7% used inheritance money for their purchase—a record high, Lautz noted. First-time buyers are coming up with the highest down payments in nearly 30 years—at 9%—in order to afford the higher home prices.

The allure of cities grows. The pandemic may have unleashed a trend of suburban movers, but people are now heading back to city centers—the largest uptick in a decade, Lautz said.

More buyers are pooling their money. The number of multigenerational households surged to an all-time high of 17% over the past year. “The number one reason is for cost savings,” Lautz said. “They’re combining incomes” in order to afford homeownership. They’re also buying a multigenerational home to take care of aging parents or because of young adults are moving back home, Lautz noted.

Single women buyers continue to outpace single men buyers. A drop in marriage rates has triggered more consumers to enter the housing market on their own. Single women held a 24% share of the home-purchase market over the past year. For single men, it was 11%.

According to a new Zillow Home Loans analysis, a monthly mortgage payment is actually less expensive than rent in 22 of the 50 largest U.S. metros. Recent dips in mortgage rates, which have fallen to the lowest level since early 2023, have significantly reduced monthly payments.

Locally, the median rent in the Charleston market is $2800 / month (this varies by submarkets) and is 33% higher than the national median.

The Lower rates have been much anticipated and is making home ownership more affordable for many buyers.

If you have considered buying a home, I would love to help you through the process, feel free to contact me anytime!